Emissions from Scottish hydrogen – international standards and export competitiveness

Research completed: October 2024

DOI: http://dx.doi.org/10.7488/era/5354

Executive summary

Scotland has set ambitions in its Hydrogen Action Plan to install at least 5 gigawatts of renewable and low-carbon hydrogen production capacity by 2030, and 25 gigawatts by 2045. Given Scotland’s hydrogen export ambitions, it is critical to understand any barriers to compliance with standards in potential markets, as well as Scotland’s international competitiveness as a hydrogen exporter.

Aims of the project

The main objectives of this study are to compare existing and developing hydrogen sustainability standards globally; and to compare the greenhouse gas (GHG) emissions of hydrogen and derivatives exported from Scotland to the EU market with those from other regions in meeting EU requirements.

Findings and recommendations

Key hydrogen standards globally already set out different GHG calculation methodologies and compliance requirements for producers. Hydrogen imported to the EU market currently must comply with rules set by the EU Renewable Energy Directive (RED) and the EU Gas Directive, if they are to contribute towards targets set under these policies. While an international standard is being developed (ISO 19870), it is unclear if the UK or EU will align with it in the future.

With regard to GHG emissions, electrolytic hydrogen produced in Scotland and exported to the EU market could be one of the most competitive from the countries we studied. Today, electrolytic hydrogen produced from renewable electricity in Scotland can already meet the EU RED GHG emission threshold (Figure 1). We refer to the GHG intensity of electricity used for Scotland pathways as the “Scottish grid” and use the National Grid country GHG intensity for Scotland rather than the GB grid electricity average GHG intensity. Of the other countries we considered, only Norway, with a grid that uses mainly hydro-electric power, can deliver electrolytic hydrogen to the EU with lower GHG emissions than Scotland. Further grid decarbonisation would increase the likelihood of compliance for hydrogen made from grid power, known as grid-connected electrolysis, by 2030. This would be the case even if, under EU rules, the Great Britain (GB) grid average factor has to be used instead of the (much lower) Scottish grid average.

When transported over short distances as compressed hydrogen via pipelines or ships, electrolytic hydrogen produced using low-carbon electricity is expected to meet the EU GHG threshold. This is applicable in both 2023 and 2030 to renewable hydrogen produced in Scotland, Norway and Morocco, and to hydrogen produced from nuclear power in France (Figure 1).

Transporting hydrogen as ammonia leads to significantly higher GHG emissions. Producers who rely on ammonia for long-distance transport from countries such as Chile and the USA may need to reduce emissions further to comply with EU policies, particularly if ammonia is reconverted to hydrogen for final use. Over shorter distances, hydrogen produced in Scotland or Norway using renewable electricity and transported as ammonia is likely to comply with the EU GHG emission threshold by 2030 (Figure 1). France will only meet the EU threshold if ammonia is used as the end-product in 2030 due to additional emissions from nuclear electricity inputs. Meeting the threshold requires further emission reduction measures such as using renewable electricity for hydrogen distribution.

Only countries with a high share of low-carbon electricity on their grid can meet the EU GHG emission threshold for hydrogen produced from grid electricity. In 2023, hydrogen produced from grid electricity in Norway could already meet the EU threshold when transported as compressed hydrogen. This could also be achieved in Scotland if compressed hydrogen is transported via pipelines. In 2030, all production pathways in Scotland can meet the EU threshold if the GHG emission intensity of grid electricity (emissions per kilowatt-hour of electricity generated) specific to Scotland decreases in line with policy aspirations. If using the GB grid emission intensity, only the pipeline transport pathway could meet the threshold by 2030, with grid decarbonisation in line with policy ambitions. Hydrogen produced from grids heavily reliant on fossil fuels such as those in Morocco, Chile and the USA will not be compliant (Figure 2).

Many natural gas pathways modelled will not comply with the EU Gas Directive threshold. These pathways are highly sensitive to the GHG intensity of upstream natural gas production, which is uncertain and can be highly variable depending on the source (e.g. imported LNG with high intensities). Based on the default upstream natural gas intensity published in the EU RED Delegated Act 2023/1185 (as the EU Gas Directive Delegated Act is not yet finalised), hydrogen produced from natural gas in the UK could be compliant when piped or shipped as compressed hydrogen (Figure 3). This would give it an emissions advantage over US natural gas-derived hydrogen, which is transported via ammonia.

GB’s electricity grid as a whole has a significantly higher GHG intensity than Scotland, so further clarity on the definition of bidding zones in the EU RED Delegated Act is critical. Using the GB grid GHG intensity average for grid-electrolysis projects in Scotland results in high risk of non-compliance with the EU GHG threshold whereas using data specific to Scotland would confer significant advantages on grid electrolysis projects, including exemptions from some EU requirements.

This GHG emission analysis could be combined with the previous ClimateXChange cost analysis to evaluate the overall competitiveness of these hydrogen pathways. Further work could provide a view on the costs of adopting renewable electricity across all the post-production supply chain steps, alternative renewable heat for the ammonia cracking step of relevant pathways and/or switching in 2030 to using only zero emission marine fuels for shipping pathways. Implementing the hydrogen and ammonia pathways modelled in this study may require significant investment in new infrastructure for some countries, and these infrastructure needs and any first-mover advantages could be investigated further.

Abbreviations table

|

ATR |

Autothermal Reforming |

|

CCR |

Carbon Capture and Replacement |

|

CCS |

Carbon Capture and Storage |

|

CCU |

Carbon Capture and Utilisation |

|

CfD |

Contract for Difference |

|

CO2 |

Carbon Dioxide |

|

DA |

Delegated Act |

|

DESNZ |

Department for Energy Security and Net Zero |

|

EU RED |

European Union Renewable Energy Directive |

|

H2 |

Hydrogen |

|

GB |

Great Britain |

|

GH2 |

Green Hydrogen Standard |

|

GHG |

Greenhouse Gas |

|

GO |

Guarantee of Origin |

|

GREET |

Greenhouse gases, Regulated Emissions and Energy use in Transportation model |

|

GTP |

Global Temperature Potential |

|

GWP |

Global Warming Potential |

|

IPHE |

International Partnership for Hydrogen and Fuel Cells in the Economy |

|

IRA |

Inflation Reduction Act |

|

ISO |

International Organization for Standardization |

|

LCHS |

Low Carbon Hydrogen Standard |

|

LHV |

Lower Heating Value |

|

MJ |

Megajoule |

|

MPa |

Megapascal |

|

PPA |

Power Purchase Agreement |

|

PTC |

Production Tax Credit |

|

RCF |

Recycled Carbon Fuel |

|

REC |

Renewable Energy Certificate |

|

RES |

Renewable Energy Source |

|

RFNBO |

Renewable Fuel of Non-Biological Origin |

Introduction

In the 2022 Hydrogen Action Plan, Scotland set ambitions to install at least 5 gigawatts of renewable and low-carbon hydrogen production capacity by 2030, and 25 gigawatts by 2045 (Scottish Government, 2022). Given Scotland’s significant potential for hydrogen production using renewable electricity, the government has also published its Hydrogen Sector Export Plan (HSEP).

Low-carbon hydrogen is a nascent market, as most hydrogen used today is derived from fossil sources. As such, regulations, standards and schemes are being put in place globally to promote the use of low-carbon hydrogen, as well as to ensure that its production and use are sustainable. For example, in the UK, the Low Carbon Hydrogen Standard (DESNZ, 2023) has been established and continues to evolve. EU rules exist for renewable hydrogen pathways and are being developed for non-renewable pathways. Additionally, a global standard for hydrogen lifecycle GHG emissions is under development.

The main objective of this study is to compare existing and developing hydrogen lifecycle GHG standards globally and quantify how the GHG emissions (including not only carbon dioxide but other GHGs such as methane and nitrous oxide) of Scottish exports to the EU, in various forms, would compare against those from other regions in meeting EU requirements. Results from this report supported the development of the Hydrogen Sector Export Plan (HSEP) by identifying potential barriers to compliance with standards in potential markets, as well as Scotland’s international competitiveness as a hydrogen exporting country.

This report is a follow-up to a previous CXC project: “Cost reduction pathways of green hydrogen production in Scotland – total costs and international comparisons” (Arup, 2024).

International hydrogen standards

Several hydrogen standards, sustainability schemes and policies have recently been developed to support the implementation of national hydrogen strategies around the world. These standards typically set out a GHG emission calculation methodology and (where applicable) a maximum GHG emission intensity, as well as broader sustainability criteria and evidence requirements for eligible hydrogen pathways to comply with.

This section provides summary tables of those standards/schemes/relevant policies (referred to as standards thereafter when referenced collectively) listed in Table 1 and provides a snapshot of the key criteria. A detailed review of each standard can be found in Appendix B which focuses the discussion on key differences, along with key uncertainties and potential changes. The UK Low Carbon Hydrogen Standard (LCHS) is used as a benchmark for this comparison, as it sets the requirements for producers in Scotland receiving UK Government support. This review includes:

The scope of each standard, including:

- The type of standard (mandatory, voluntary), and who it was developed by.

- Geographies covered.

- Implementation status.

Eligibility criteria:

- Conversion technology or feedstock restrictions, including any biomass feedstock sustainability rules.

- Any GHG emission intensity thresholds.

- Any categories of hydrogen labelled by the standard.

GHG calculation methodology, including:

- System boundary – which parts of the supply chain are in or out of scope of the GHG emissions calculations. This can vary between standards, thereby potentially omitting or including significant emissions, and making comparison of results challenging between different standards.

- Splitting of emissions across co-products. When systems produce multiple outputs (product, co-products, wastes, residues, etc.), GHG emissions must be assigned between them. This can be done through various approaches, including through an allocation of emissions based on the relative masses, energy contents or economic value of the (co-)products. This can also be done by looking at the products these co-products would replace in the market (via system expansion) to assign substitution credits. Typically, wastes and residues are not assigned emissions. A full discussion of the various methods is provided in Appendix A.

- Reference flow – a set pressure and/or purity for the hydrogen product. Hydrogen produced at a lower pressure or purity may be required to account for the emissions for theoretical compression and/or purification to reach the reference flow, and in some standards, hydrogen produced at a higher pressure and/or purity than the reference may be given an emissions credit.

Other relevant requirements, such as:

- Chain of custody. This is the process of following and evidencing materials through steps of the supply chain, which provides insights into the product’s origin, components, processes, and handlers. As illustrated in Appendix A, there are different chain of custody models, and while some standards are explicit and prescriptive in their requirements on how to trace feedstocks and hydrogen products, others are not; and

- Renewable electricity sourcing. Some standards may impose requirements to ensure the use of renewable electricity for hydrogen production does not negatively impact the wider grid. These can include temporal correlation (matching generation with consumption over defined time periods), geographical correlation (rules about locations and grid connections) and “additionality” (hydrogen production contracting with new, rather than existing, renewable electricity generation).

In addition to national or regional standards and policies, and several voluntary schemes[1], a global hydrogen lifecycle GHG standard is also currently being developed by the International Organization for Standardization (ISO). This could enable greater harmonisation of GHG emission calculation methodologies across the globe. The implications of this scenario will be explored further in Chapter 3.

|

Region |

Relevant hydrogen standards[2] |

|---|---|

|

UK |

|

|

EU |

|

|

US |

|

|

International |

|

Summary of hydrogen standards

|

Standard |

Geographic scope |

Type of standard |

Status |

System boundary |

|---|---|---|---|---|

|

UK LCHS |

UK producers |

Mandatory government standard for accessing subsidy schemes |

Implemented. V3 is live (Dec 2023) |

Cradle to production gate |

|

EU RED |

Hydrogen consumed in the EU |

Directive (with Delegated Acts) |

REDII (Dec 2018) is fully transposed into Member State legislation and Delegated Acts (Feb 2023) are live. REDIII implemented (Oct 2023) but still being transposed |

Cradle to use |

|

EU Gas Directive |

Hydrogen consumed in the EU |

Directive (with draft Delegated Act) |

Implemented (July 2024), but still being transposed into Member State legislation. Delegated Act is pending, due by July 2025 |

Cradle to use |

|

CertifHy |

Hydrogen producers in EU, EEA and CH |

Voluntary standard, industry developed |

Implemented. V2 is live (April 2022) |

Cradle to production gate |

|

France Energy Code L. 811-1 |

Hydrogen consumed in France |

Mandatory standard for accessing subsidies, Government developed |

Implemented. V1 is live (July 2024) |

Cradle to use |

|

US IRA 45V |

US producers |

Tax credit |

Implemented. March 2024 revision is live |

Cradle to production gate |

|

IPHE |

Global producers and consumers |

Voluntary transnational effort on GHG methodology harmonisation |

Implemented. V3 is live (July 2023) |

Cradle to use |

|

ISO 19870 |

Global producers |

Voluntary standard, ISO developed |

Technical Specification published in Dec 2023, full standard 19870-1 under revision during 2024, due to be finalised in 2025 |

Cradle to production gate. ISO 19870 series will next look at downstream hydrogen vectors |

|

TÜV SÜD |

Global producers |

Voluntary standard, industry developed |

Implemented. V 11/2021 is live (Nov 2021) |

Cradle to production gate (GreenHydrogen), or to point of use (GreenHydrogen+) |

|

TÜV Rheinland |

Global producers |

Voluntary standard, industry developed |

Implemented. V2.1 is live (March 2023) |

Cradle to production gate or to point of use |

|

GH2 |

Global producers |

Voluntary standard, industry developed |

Implemented. V2 is live (Dec 2023) |

Cradle to production gate |

|

Scheme |

GHG threshold |

Category |

Eligible pathways |

Eligible main inputs |

Biomass sustainability |

|---|---|---|---|---|---|

|

UK LCHS |

20 gCO₂e/MJLHV |

“Low carbon” |

Electrolysis, Fossil/Biogenic gas reforming with CCS, Biomass/Waste gasification, Gas splitting producing Solid Carbon. Pathways can be added |

Electricity (all types), Fossil fuels, Biomass, Bio/fossil wastes & residues |

Biomass inputs must meet relevant Forestry, Land and/or Soil Carbon criteria, and report indirect land use change GHGs |

|

EU RED |

28.2 gCO₂e/MJLHV |

“Biofuel”, “RFNBO”, “RCF” |

All production pathways eligible but feedstock dependent |

Renewable electricity, Biomass & Fossil wastes |

Biomass feedstocks must meet relevant Forestry, Land and/or Soil Carbon criteria |

|

EU Gas Directive |

28.2 gCO₂e/MJLHV |

“Low carbon fuel” |

All pathways eligible |

Non-renewable energy sources |

Follows RED, where applicable |

|

CertifHy |

36.4 gCO₂e/MJLHV |

“Green” |

All pathways eligible |

Renewable energy sources |

Not specified |

|

“Low-carbon” |

Non-renewable sources | ||||

|

France Energy Code L. 811-1 |

28.2 gCO₂e/MJLHV |

“Renewable”, |

RFNBOs, RCF, nuclear-based |

Follows EU RED and adds nuclear electricity |

Follows EU RED |

|

US IRA 45V |

Increasing tax credits at 33.3, 20.6, 12.5 or 3.75 gCO₂e/MJLHV |

“Clean” |

All pathways eligible. Those not in 45V-GREET can apply for a “provisional emissions rate” |

Electricity (all types), Fossil fuels, Biomass |

None |

|

IPHE |

None, only a method |

No categories |

Electrolysis, steam cracking, fossil gas reforming + CCS, coal or biomass gasification + CCS, biomass digestion + CCS. More will be added |

Fossil fuel, Biomass, Bio/fossil wastes & residues |

Not specified |

|

ISO 19870 |

None, only a method |

No categories |

All pathways eligible |

Feedstock neutral |

None |

|

TÜV SÜD |

28.2 gCO₂e/MJLHV |

“Green” |

Electrolysis, Biomethane steam reforming, Glycerine pyro-reforming |

Renewable electricity, Bio waste/residue, Biomass |

Biomass feedstocks must meet EU RED criteria |

|

TÜV Rheinland |

28.2 gCO₂e/MJLHV |

“Renewable” |

Renewable electrolysis |

Renewable electricity |

Not specified |

|

“Low-carbon” |

All production pathways |

Feedstock neutral | |||

|

GH2 |

8.33 gCO₂e/MJLHV |

“Green” |

Electrolysis |

Renewable electricity |

Low iLUC risk, non-biodiverse land |

|

Scheme |

Chain of Custody |

Co-product allocation |

Reference flow |

Renewable power evidence |

|---|---|---|---|---|

|

UK LCHS |

Mass balance used, but cannot blend biomethane with nat gas (upstream) |

LHV energy allocation (Carnot efficiency for heat), plus system expansion for waste fossil feedstock counterfactual |

3 MPa, 99.9 vol% purity. If below, adjustment required |

Additionality not required. PPA with 30-minute temporal correlation from UK generator needed, or avoided curtailment proof |

|

EU RED |

Mass balance (H2 + upstream) |

LHV energy allocation (Carnot efficiency for heat). If co-product ratio can change, physical causality used. If co-product has zero LHV, economic allocation used |

None |

Renewable PPAs complying with additionality, temporal and geographic correlation rules |

|

EU Gas Directive |

Mass balance (H2 + upstream) |

Assumed to follow EU RED |

None |

In line with EU RED Delegated Act for RFNBOs |

|

CertifHy |

Book & Claim as GOs allowed (upstream) |

Defined approach for each pathway broadly follows EU RED. O2 method TBC |

Same as UK LCHS |

GOs are allowed. No additional requirements. |

|

France |

Follows EU RED |

Follows EU RED |

None |

Follows EU RED |

|

US IRA 45V |

None specified, but proposed mass balance for biomethane (upstream) |

System expansion. Restrictions placed on the size of steam co-product credit |

2 MPa, 100% purity. Adjustment required for higher/lower |

PPAs complying with additionality, temporal and geographic correlation |

|

IPHE |

None specified but GOs allowed (upstream) |

Follows hierarchy but recommended approach for each pathway differs |

Not specified |

GOs are allowed. Additionality not required. |

|

ISO 19870 |

None specified but GOs allowed (upstream) |

Can be system expansion or attributional. Approach defined for pathways differ |

None. GHG increase to reflect impurities and their release |

Grid GOs are allowed if ISO 14064-1 “proper quality criteria” are met |

|

TÜV SÜD |

Mass balance (H2 + upstream) |

Follows EU RED, but chlor-alkali has choice of energy allocation, economic allocation or system expansion |

Same as UK LCHS |

GreenHydrogen must follow EU RED. GreenHydrogen + must meet more stringent additionality rules. |

|

TÜV Rheinland |

None specified but assumed to follow EU RED & Gas Directive |

Assumed to follow EU RED & Gas Directive |

None |

PPAs to have temporal correlation (up to yearly) and geographic correlation within the same country. Additionality not required. |

|

GH2 |

Follows IPHE |

System expansion recommended, as oxygen nil LHV |

Same as UK LCHS |

Additionality, temporal and geographical correlations are allowed but not required |

Lifecycle GHG emission intensity of hydrogen pathways for import to the EU market

The GHG emission intensity of various hydrogen pathways from Scotland and other exporting countries were calculated using ERM’s in-house GHG assessment model. The hydrogen pathways modelled used a combination of the production, distribution, and use steps, set out in Table 5 below. For a comprehensive list of the GHG pathways modelled, refer to Appendix D, and see Table 8 for the assumptions and references used in the modelling process.

|

Production location |

Hydrogen production types |

Hydrogen transport |

Final use |

|---|---|---|---|

|

Scotland Norway France Morocco USA Chile UK |

Electrolysis using grid electricity Electrolysis using renewable electricity (excluding France) Electrolysis using nuclear electricity (only in France) Natural gas autothermal reforming with carbon capture & sequestration (ATR + CCS) |

Ammonia shipping Ammonia shipping with reconversion to hydrogen Compressed hydrogen shipping Compressed hydrogen pipeline |

Hydrogen in refinery boiler Ammonia in marine vessel |

Methodologies used to model lifecycle GHG emission intensity of imported hydrogen pathways

Section 2 detailed the various GHG calculation methodologies and compliance requirements set by key hydrogen standards that are currently active globally. In the EU market, EU RED and the EU Gas Directive currently set the eligibility criteria and the methodology for calculating the GHG emission intensity for imported hydrogen. As the hydrogen market becomes more established and globalised, there could be growing interest globally in harmonising approaches for GHG accounting (e.g. through alignment with ISO 19870). However, the EU has not yet expressed any intentions to do so. As such, two scenarios can be envisioned regarding possible evolutions of the EU’s approach for calculating life-cycle GHG emissions of hydrogen:

- Business-as-usual: The EU RED and EU Gas Directive will continue to apply for hydrogen imported in the EU, regardless of global methodologies such as ISO 19870.

- International alignment: The EU aligns with ISO 19870 at some future point in time, after publication.

The components of calculating the GHG emissions under these scenarios can be found in Appendix C. The key methodological differences considered during modelling include:

- System boundary: The system boundary for EU policies is ‘cradle-to-use’, whereas ISO/TS 19870 uses ‘cradle-to-production gate’. Results under scenario 2 therefore exclude potentially significant emissions from distribution of hydrogen to the EU.

- GHG threshold: EU sets a GHG threshold of 28.2 gCO2eq/MJLHV hydrogen, whereas ISO does not set a GHG threshold. As such, compliance with GHG thresholds were only carried out for results using the EU methodology.

- Reference flow: EU RED and the EU Gas Directive do not set a reference flow. The reference flow under ISO 19870 is set by the end-user but the GHG intensity is adjusted upwards for (project specific) impurities and their release.

- Co-product emission assignment: For electrolysis with co-product oxygen sales, economic allocation is required by EU RED, whereas ISO/TS 19870 currently recommends economic allocation or system expansion. For fossil gas reforming, the EU Gas Directive DA currently uses LHV energy allocation (with steam Carnot efficiencies), whereas ISO/TS 19870 has sub-division then LHV energy allocation (using steam enthalpy changes) or else system expansion. However, as no co-products are modelled for either electrolysis or reforming pathways in this study (it is assumed for simplicity there are no oxygen or steam customers), 100% of emissions in both scenarios are assigned to the hydrogen product.

At the time of writing this report, a draft version of the EU Gas Directive DA had been released for consultation and is still therefore subject to revision. This report follows the draft DA methodology to assess the GHG emissions of fossil natural gas hydrogen pathways under the BAU scenario (as outlined in Appendix C). However, due to uncertainty about the timings of reporting under the EU Methane Regulations, this report does not apply conservative default values for upstream natural gas emissions from the draft DA, and instead relies on the upstream natural gas GHG intensity given in the final published RED DA.

GHG emission intensity results

This section presents GHG emission results for various hydrogen production pathways under EU and ISO methodologies, including hydrogen used in refinery boilers and ammonia for marine vessels. Modelling have been carried out for production in 2023 and 2030 to reflect potential impacts from decarbonisation projections (e.g. grid decarbonisation, increased use of renewable fuels in transport), and technology improvements.

Specifically for the modelling of hydrogen production in Scotland, the National Grid country GHG intensity for Scotland is used, rather than the GB grid electricity average GHG intensity. From this point forward, the GHG intensity of electricity used for Scotland pathways is referred to as the “Scottish grid”.

In addition, a sensitivity analysis was conducted on the following parameters:

- Using renewable electricity across the entire pathway

- Using renewable heat for the ammonia cracking step of relevant pathways

- Using low-carbon marine fuel for shipping pathways

- Using the UK vs Scottish grid average intensity

Further details and results of this sensitivity analysis are given in Appendix F. These results are used in the GHG emission compliance scoring matrix to assess whether a previously non-compliant production pathway can adopt mitigation measures to meet the EU GHG threshold. This matrix can be found in Appendix G.

GHG emission results for pathways producing hydrogen for use in a refinery boiler under EU methodologies

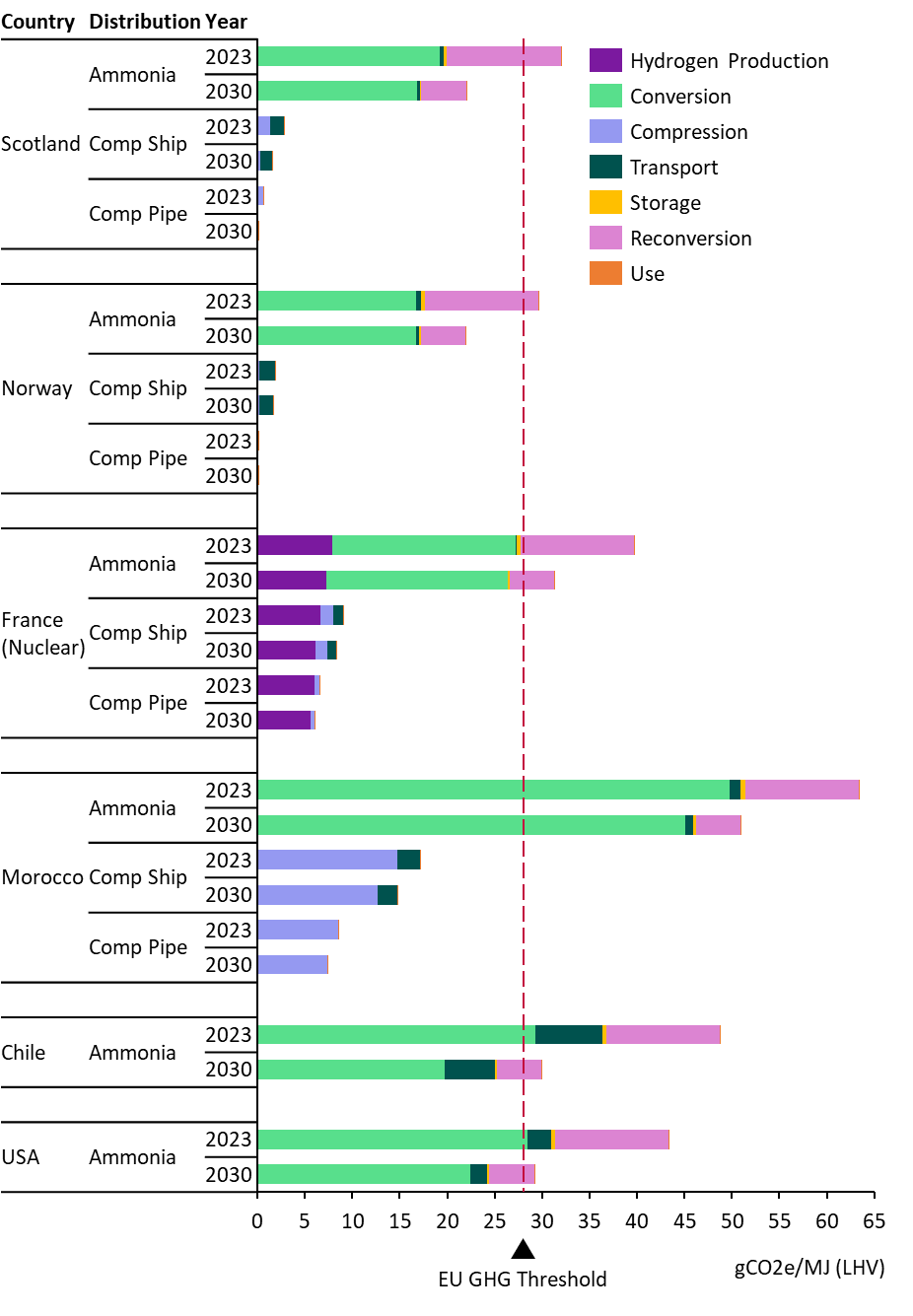

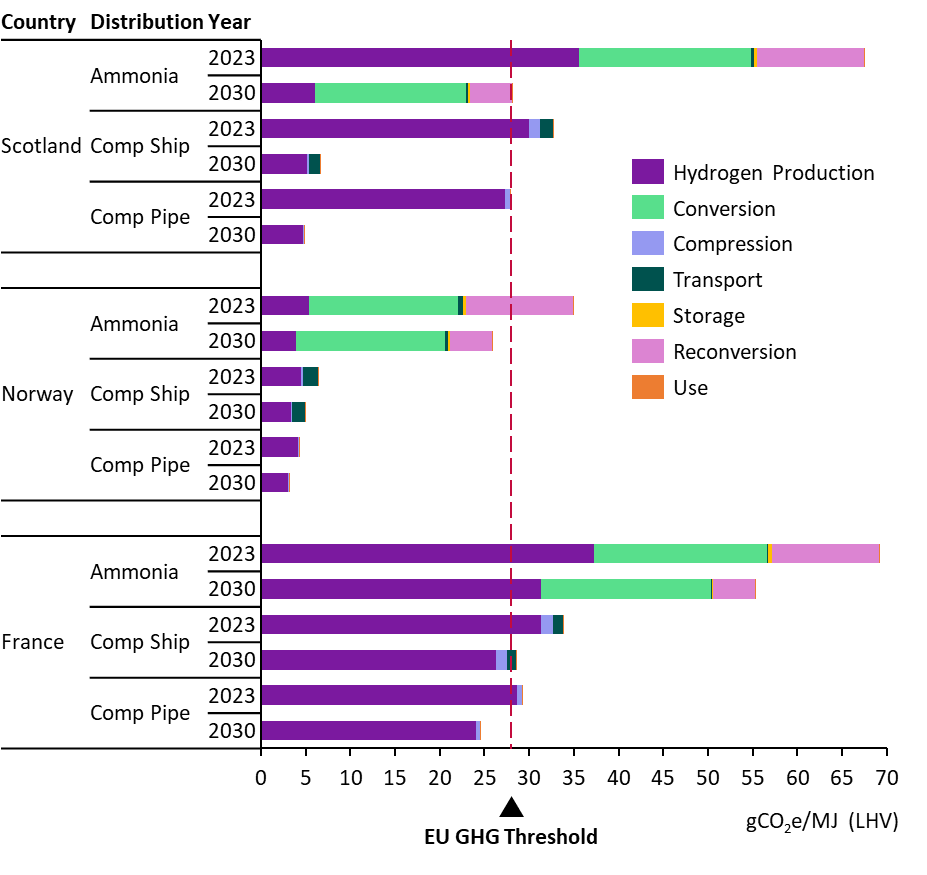

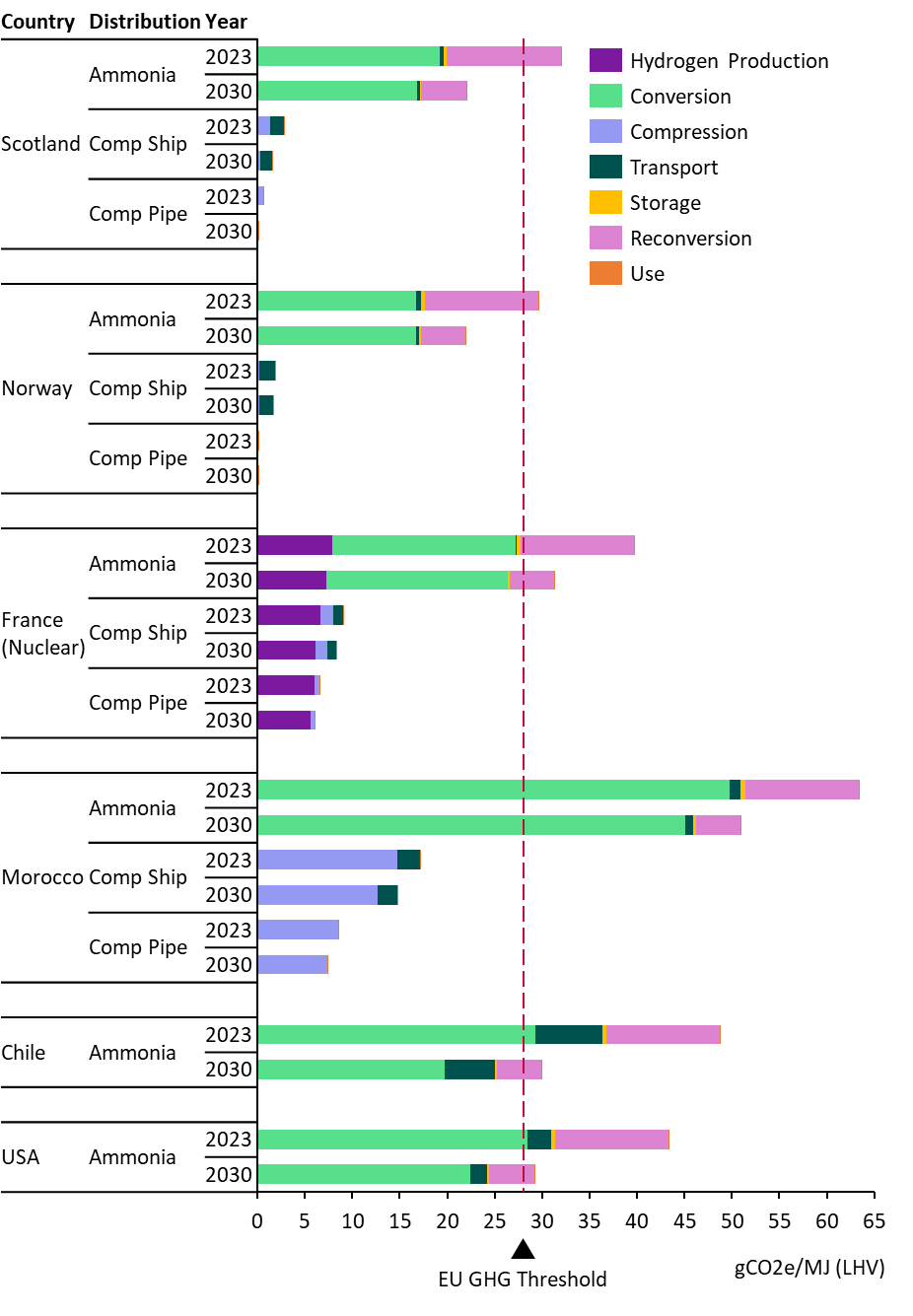

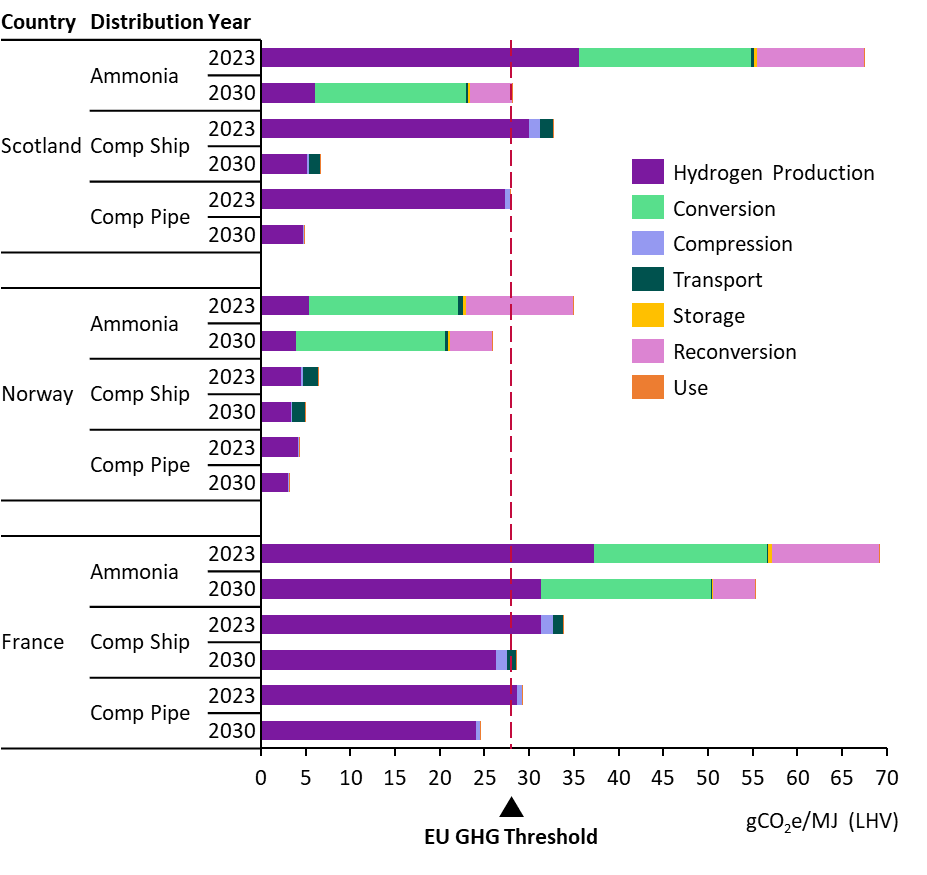

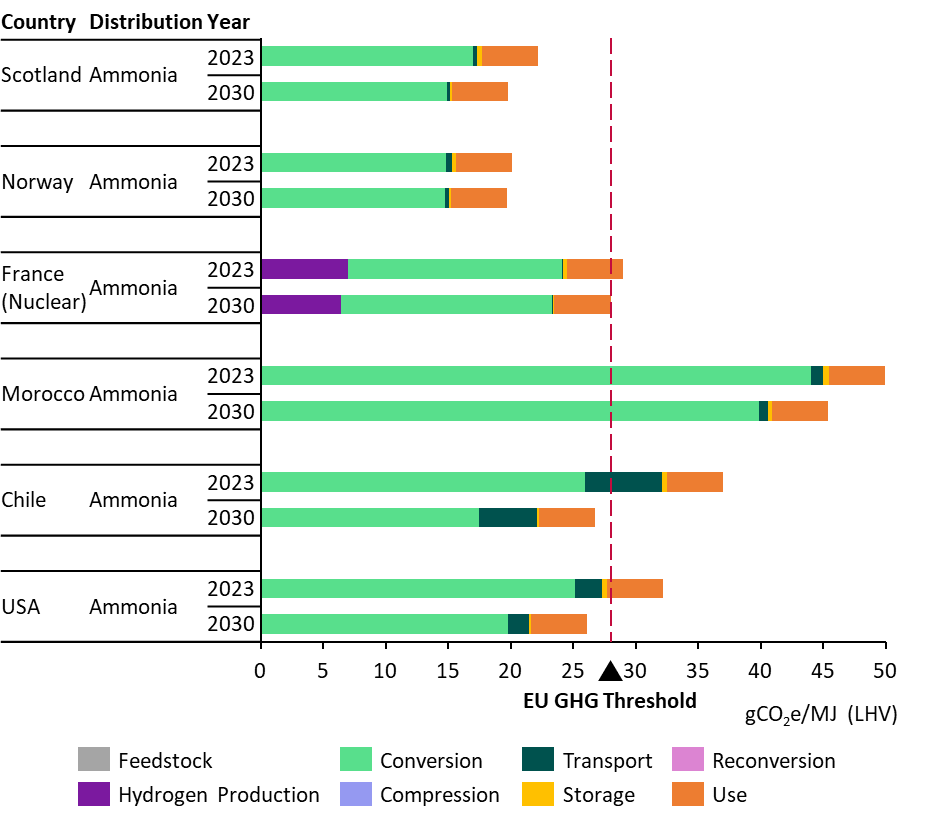

A breakdown of the GHG emissions at each stage of the hydrogen production life-cycle is provided in Figure 1, Figure 2 and Figure 4. The value chain steps included in each stage include:

Feedstock emissions: this is only relevant to natural gas pathways (Figure 3), and accounts for the upstream emissions of natural gas inputs (e.g. extraction, transport, pre-processing, including methane leakage).

Hydrogen production emissions: these arise from the electrolysis or natural gas autothermal reforming with carbon capture (ATR+CCS) processes. Sources of emissions include electricity consumption, uncaptured fossil CO2 and chemical inputs.

Distribution emissions: these include compression, transport, storage, reconversion and downstream emissions. The emissions depend significantly on the hydrogen transport pathways.

- Ammonia pathways include conversion of hydrogen to ammonia, transport via truck to a port, port storage, shipping to Rotterdam, port storage, reconversion/cracking ammonia to hydrogen (requiring heating and catalysts), transport via pipeline to a refinery, and end use of hydrogen in a refinery combustion boiler.

- A separate end use case is modelled where instead of cracking and hydrogen transport, ammonia stored in Rotterdam is loaded onto a maritime vessel for combustion in the propulsion engines.

- The compressed hydrogen shipping pathways include compression of hydrogen for trucking, transport of hydrogen via truck to a port, port storage, shipping to Rotterdam, port storage, transport via pipeline to a refinery, and use of hydrogen in refinery combustion boiler.

- The compressed hydrogen pipeline pathways include compression of hydrogen, piping to Rotterdam, transport via pipeline to a refinery, and end use of hydrogen in a refinery combustion boiler.

- Transport to the EU via pipeline or via compressed hydrogen shipping were not modelled for the USA and Chile due to the long transport distance making these options unviable, following the previous ClimateXChange report.

The input values and assumptions used in the GHG modelling are detailed in Appendix E.

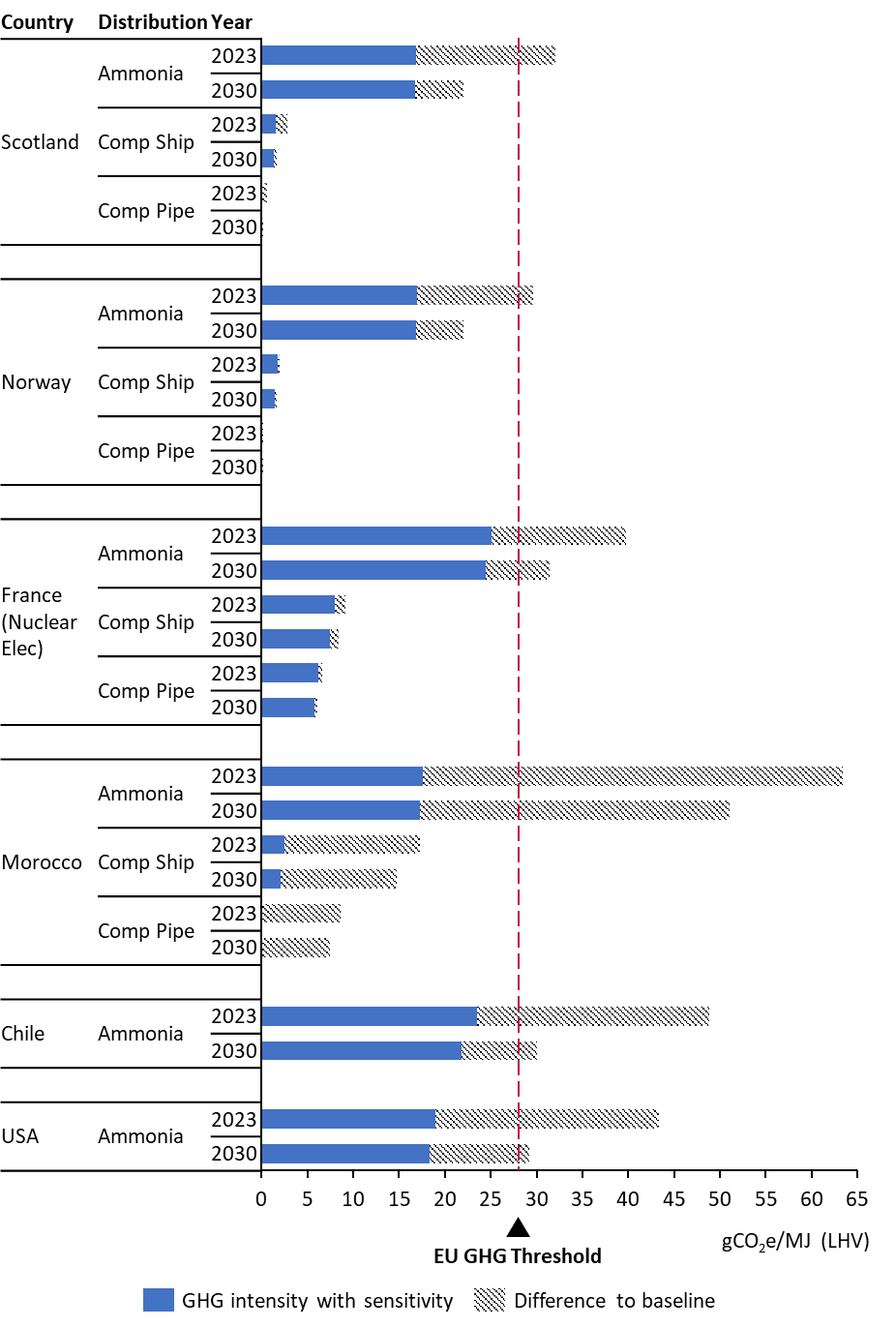

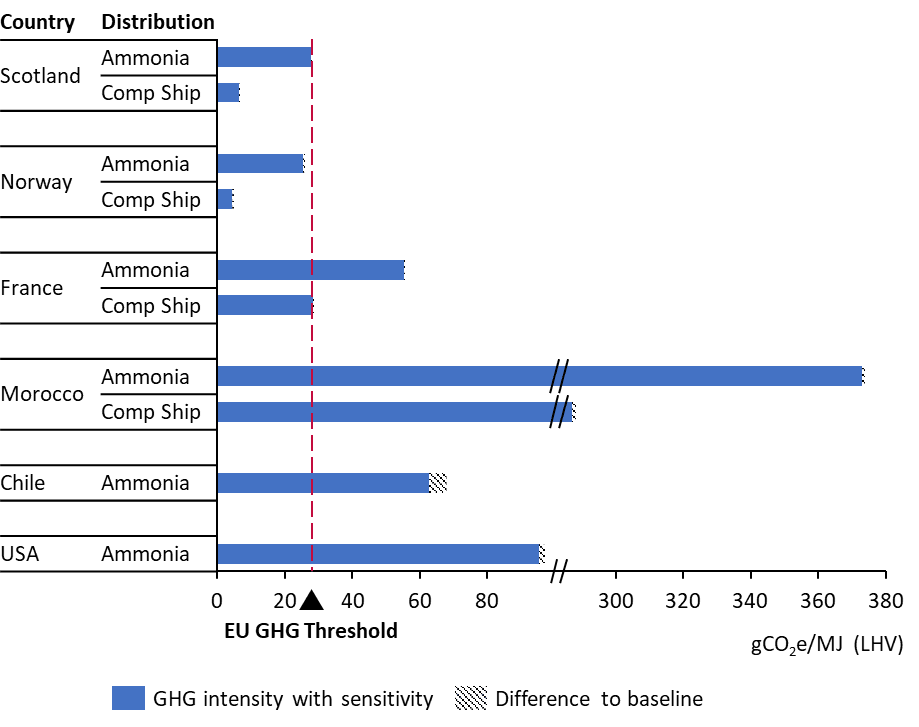

Figure 1 represents the GHG intensity of pathways that use renewable electricity for electrolytic hydrogen production, followed by distribution to the EU (using grid electricity and gas), before use of gaseous hydrogen in a refinery boiler. The exception is nuclear electricity with an emission factor of 3.64 gCO2e/MJ elec[3] being assumed to be used for electrolysis in France, which leads to higher production emissions compared to other regions using renewable electrolysis (0 gCO2e/MJ elec).

These results show that hydrogen produced from renewable electricity-based electrolysis is likely to meet the EU GHG threshold when transported as compressed hydrogen. However, transporting compressed hydrogen via ships generates higher emissions compared to transport via pipeline due to the fuel used for trucking and shipping, plus additional electricity requirements for storage at the shipping ports.

Emission intensities of hydrogen using ammonia as an intermediary vector are significantly higher than those of gaseous hydrogen pathways and may not meet the EU threshold in 2030. This is primarily due to the use of grid electricity in distribution steps, the efficiency losses in the (re)-conversion steps, and the release of nitrous oxide during ammonia production. Only Norway and Scotland might comply by 2030, due to low enough emission grid electricity in these countries. Emissions from the conversion step (ammonia production) remain significant in 2030 due to the release of nitrous oxide emissions, and the ammonia cracking step uses Netherlands grid electricity which has a high GHG intensity (although this improves significantly by 2030).

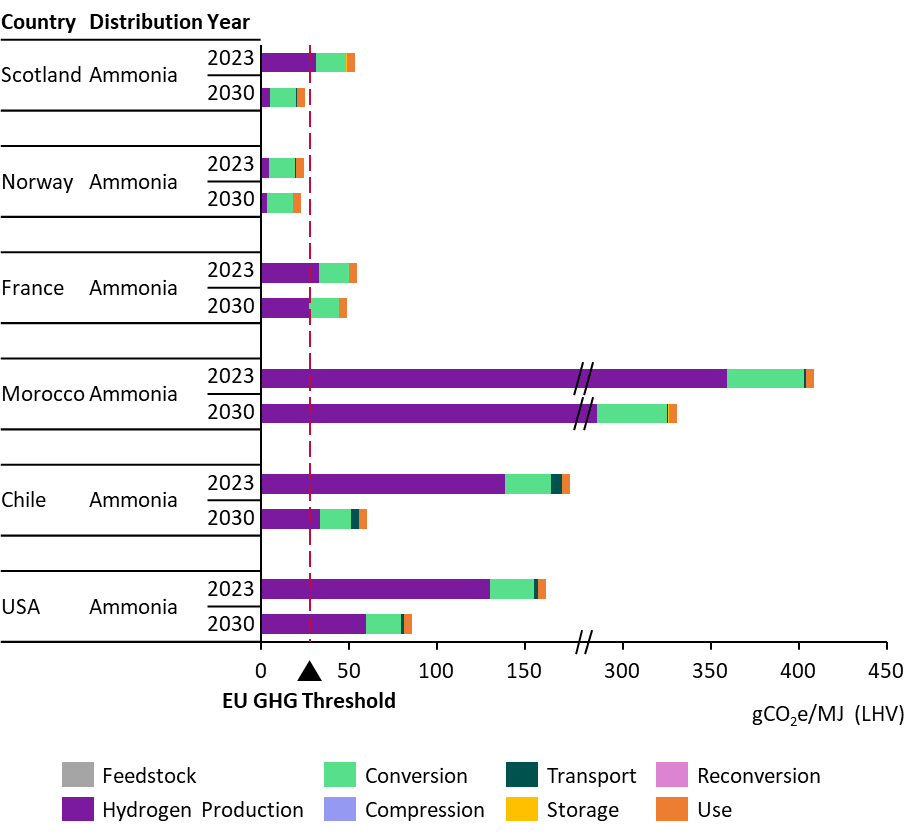

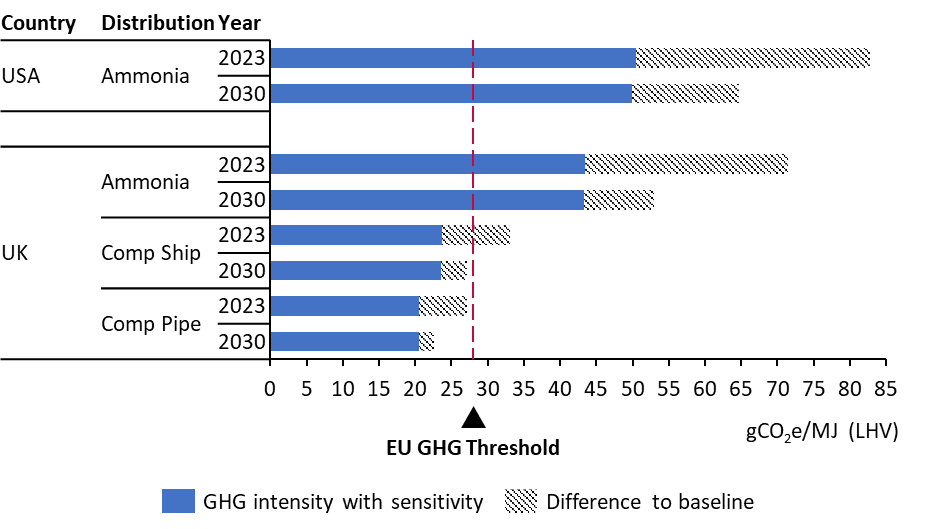

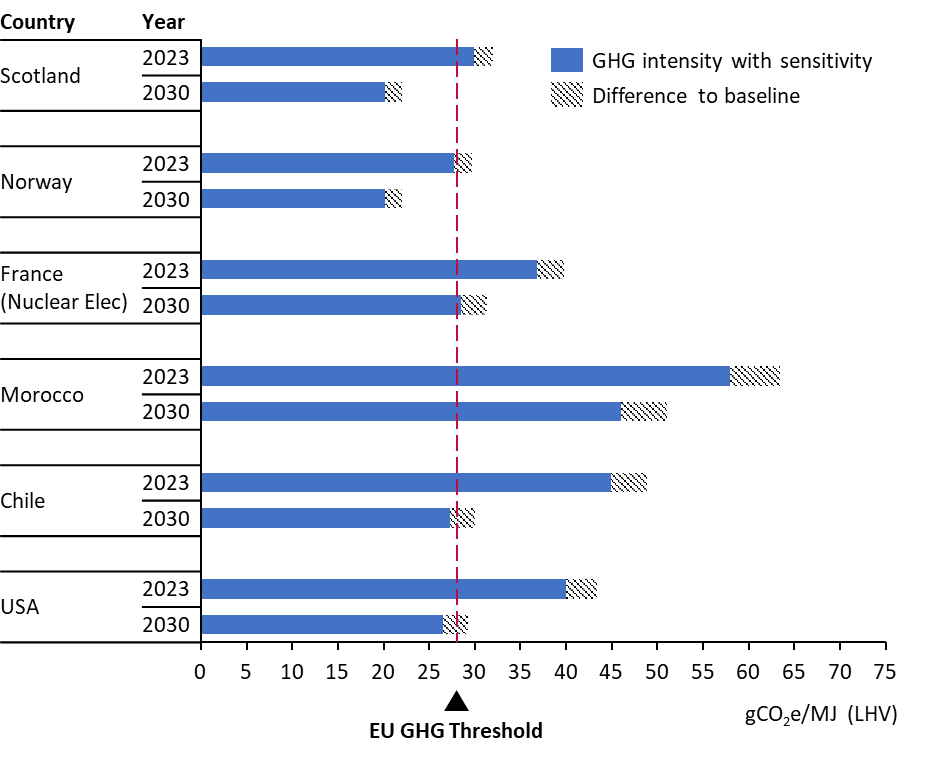

Figure 2 below shows the GHG intensity results if grid electricity is used for electrolysis instead of renewable electricity. Note the change in x-axis scale between the two graphs.

In these pathways, the emissions factor of the grid is the most important contributor to overall GHG emissions intensity of delivered hydrogen. Decarbonisation of electricity grids in some countries (i.e. Scotland and France) may enable some of the pathways to achieve the EU GHG threshold in 2030. However, gaseous pathways from Norway are expected to already comply.

For Scottish pathways, the average grid factor for Scotland was used in the GHG modelling (see Appendix E for details). This assumes that the Scottish grid intensity could be used under EU rules instead of the GB grid average, however, it remains unclear how EU rules on bidding zones apply to Scotland. A sensitivity analysis in Appendix F explores the GHG impact of using the GB grid average compared to the Scottish grid average. The results in Figure 2 show that using the Scottish grid factor in electrolysis results in the GHG emission intensity of piped and shipped compressed hydrogen pathways close to the EU GHG threshold in 2023 but easily achieving it by 2030 as the Scottish grid decarbonises. Ammonia pathways from Scotland may just meet the threshold in 2030 as electricity grids in Scotland and the Netherlands decarbonise.

Pipeline hydrogen pathways are all expected to fall below the EU GHG threshold in 2030 as electricity grids decarbonise, except for Morocco, which has a significantly higher grid GHG intensity compared with other countries. Hydrogen production in countries with high shares of fossil fuel power generation in their grid mix will have to rely on renewable electricity (Figure 1 results) to export to EU markets. For example, neither of the grid electrolysis pathways from Chile or the USA are expected to be able to meet the EU threshold, due to both high grid GHG intensities and additional emission arising from ammonia supply chains.

It is important to note that hydrogen produced from grid electricity is likely to have both renewable and non-renewable consignments. Both consignments will have the same GHG intensity under EU rules, and if this is low enough to meet the EU GHG threshold, the renewable fraction may be eligible as a RFNBO under EU RED, and the non-renewable fraction may be eligible under the EU Gas Directive.

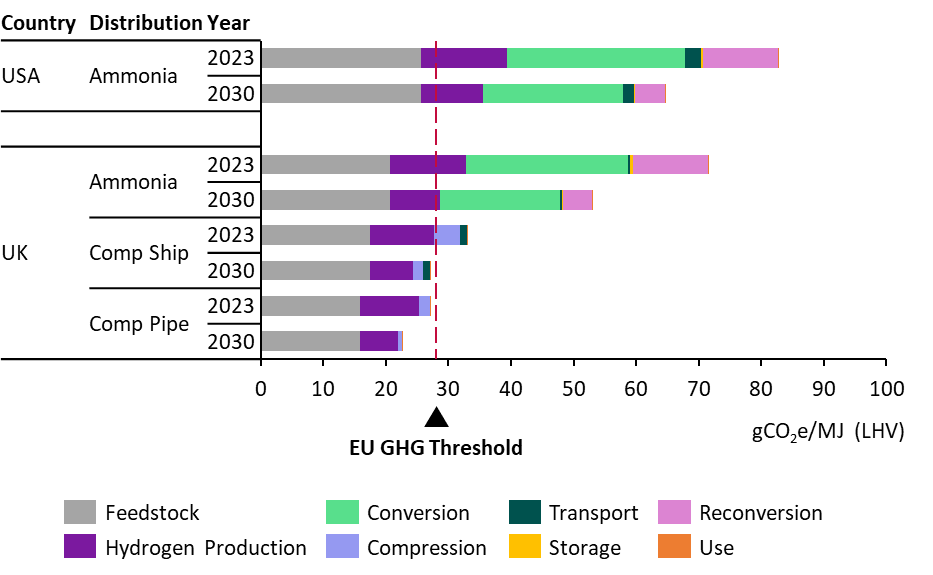

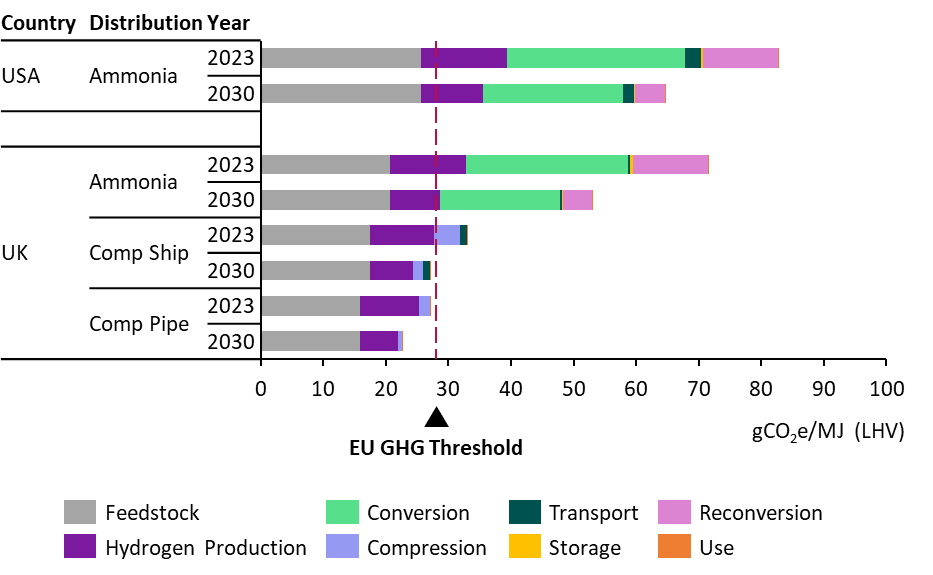

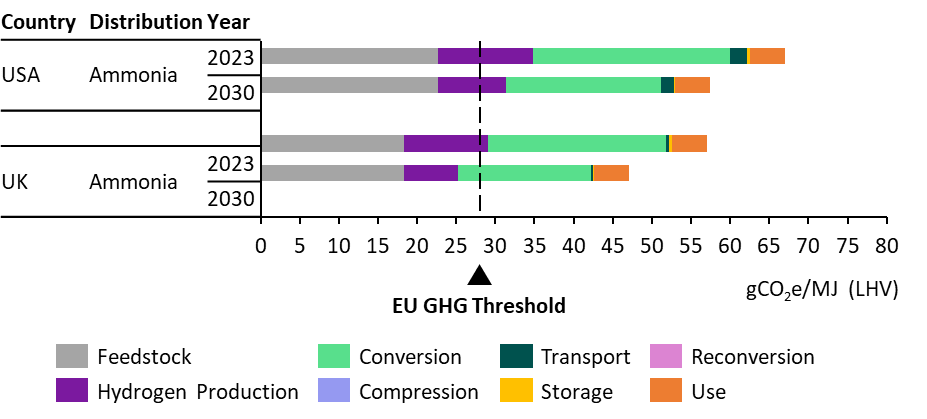

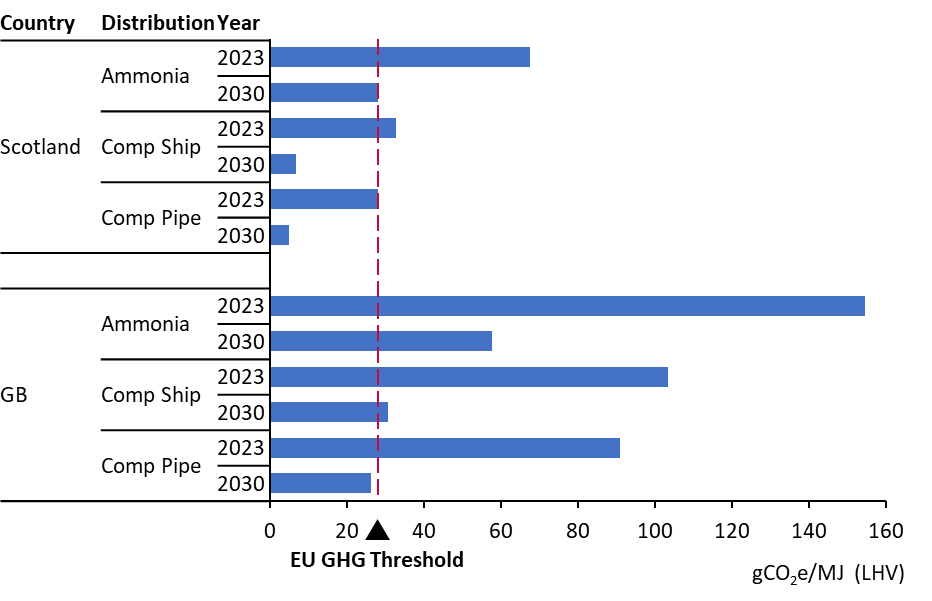

As shown in Figure 3, natural gas reforming with CCS pathways may struggle to meet the EU Gas Directive’s GHG emission threshold (same as the EU RED threshold). The emissions of hydrogen produced from these pathways are very sensitive to upstream natural gas intensities, which are highly uncertain and can be highly variable depending on the source of natural gas (e.g. imported LNG can have much higher intensities than domestic gas supplies used for hydrogen production).

The European Commission is expected to establish a methodology for calculating the methane emissions of fossil feedstocks (including natural gas) at a producer level by 2027. In the absence of this more accurate data, an upstream natural gas intensity of 12.7 gCO2e/MJLHV natural gas was used to model both USA and UK reforming pathways, based on the published generic value in the EU RED DA. However, individual producers or countries could have intensities significantly above this value. This value will likely need to be updated as more accurate, audited data is reported by the fossil gas industry.

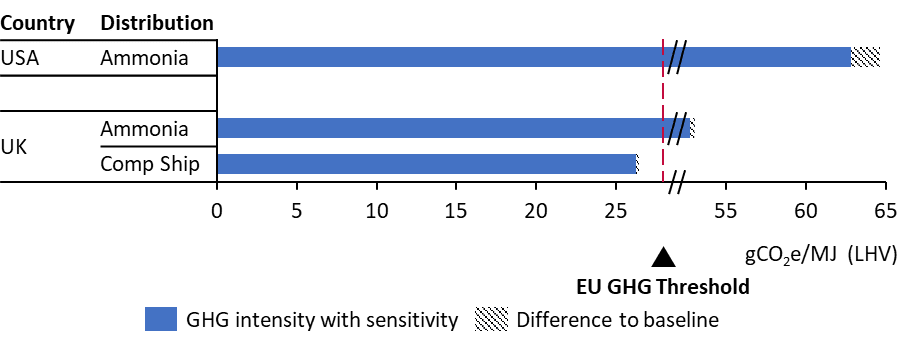

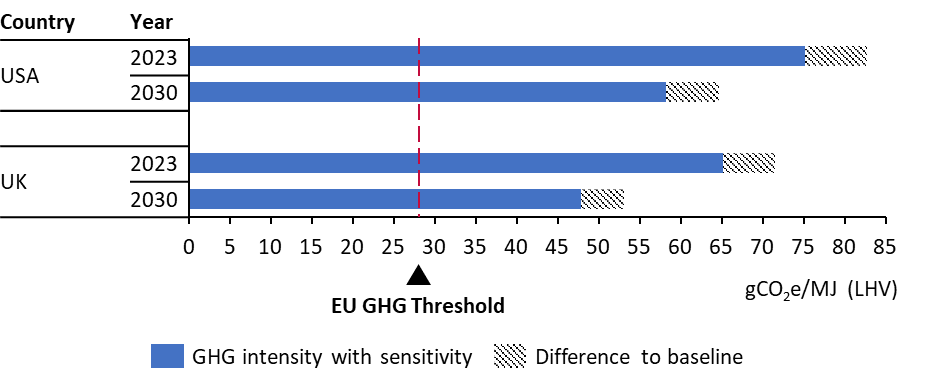

In the UK, pathways with compressed shipping or pipeline could meet the EU GHG emission threshold. In contrast, long transport distances from the USA to the EU means that it is not feasible to transport hydrogen via compressed shipping or pipeline (requiring large additional emissions from ammonia distribution), leading to the UK natural gas pathways via compressed hydrogen distribution having a significant GHG advantage compared with ammonia pathways from the USA.

GHG emission results for pathways producing ammonia for use in a marine vessel under EU methodologies

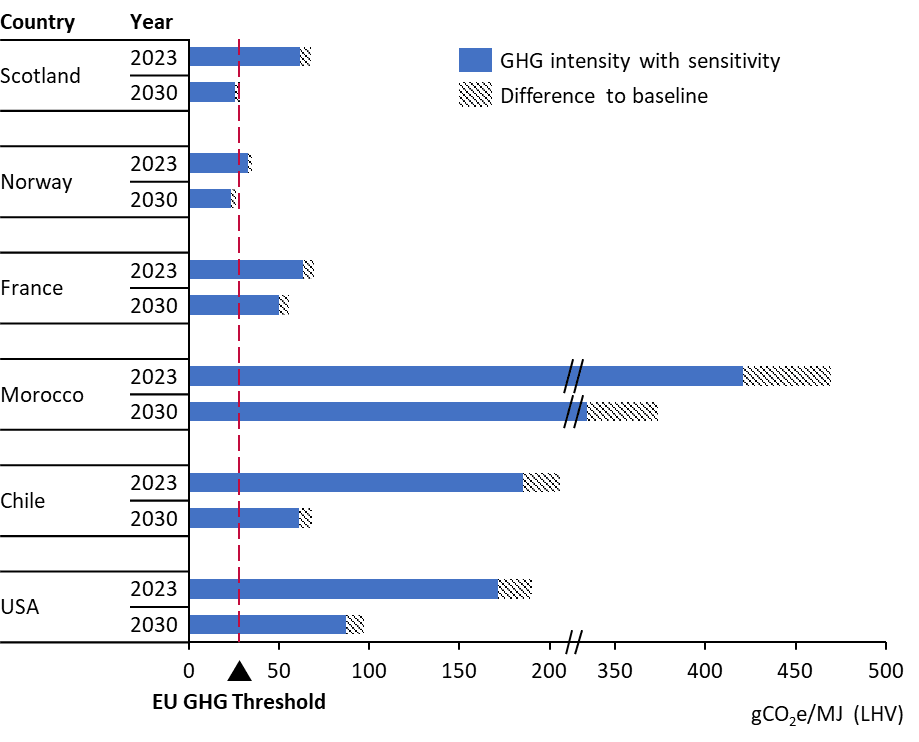

Ammonia was also modelled as the end-product for use in a marine vessel in Rotterdam. As shown below in Figure 4, Figure 5 and Figure 6, GHG emissions of these ammonia use pathways are lower than pathways with hydrogen as the end-product because ammonia reconversion back to hydrogen is not required. As in the previous analysis, grid electricity is assumed to be used for ammonia distribution (conversion, storage, reconversion) in both grid and renewable electricity-based electrolysis pathways.

Ammonia produced using renewable electricity (Figure 4) is likely to comply with the EU GHG threshold in 2023 and 2030 in both Scotland and Norway, and may just comply in France by 2030. Similar to the earlier analysis, production in the US and Chile may still struggle to comply, as the conversion step (ammonia production) accounts for a significant portion of the total pathway emissions. This is due to the release of nitrous oxide emissions, the use of grid electricity in distribution and losses in conversion efficiency.

Grid electricity-based ammonia produced in all countries modelled in this study (Figure 5) is unlikely to meet the threshold, except for Norway in both years and for Scotland in 2030. As discussed in the previous section, only the renewable portion of the ammonia would likely qualify under EU RED, the remaining portion would need to qualify under the EU Gas Directive. As shown in Figure 6, even avoiding emissions from reconversion of ammonia to gaseous hydrogen does not sufficiently reduce the emissions of natural gas reforming pathways via ammonia to comply with the EU GHG threshold.

gCO2e/MJ (LHV)

Processing

Conversion

Compression

Transport

Storage

Reconversion

Downstream

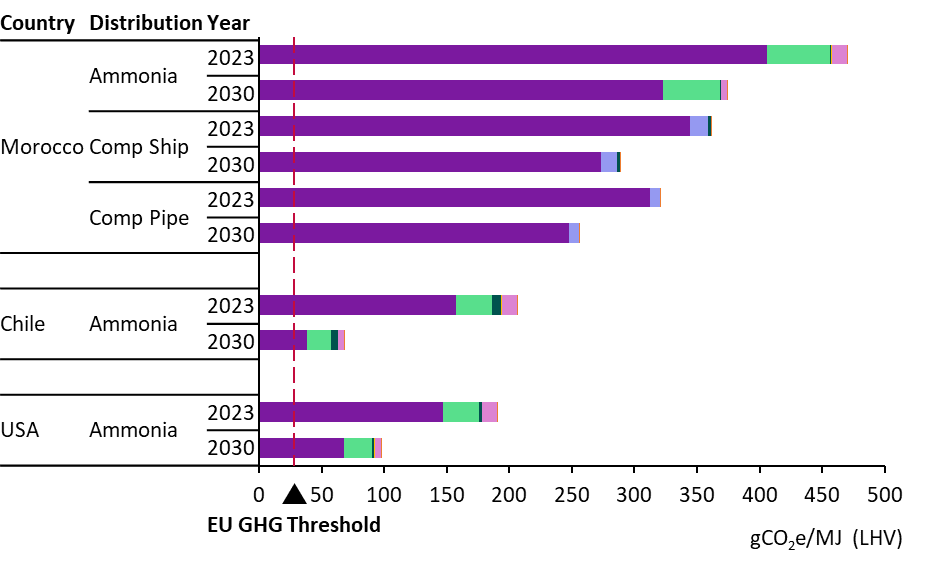

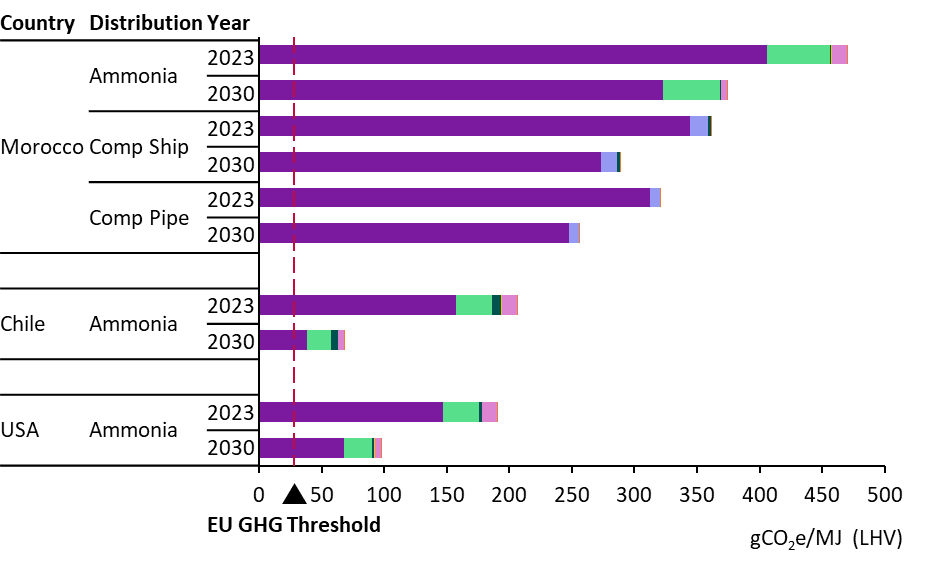

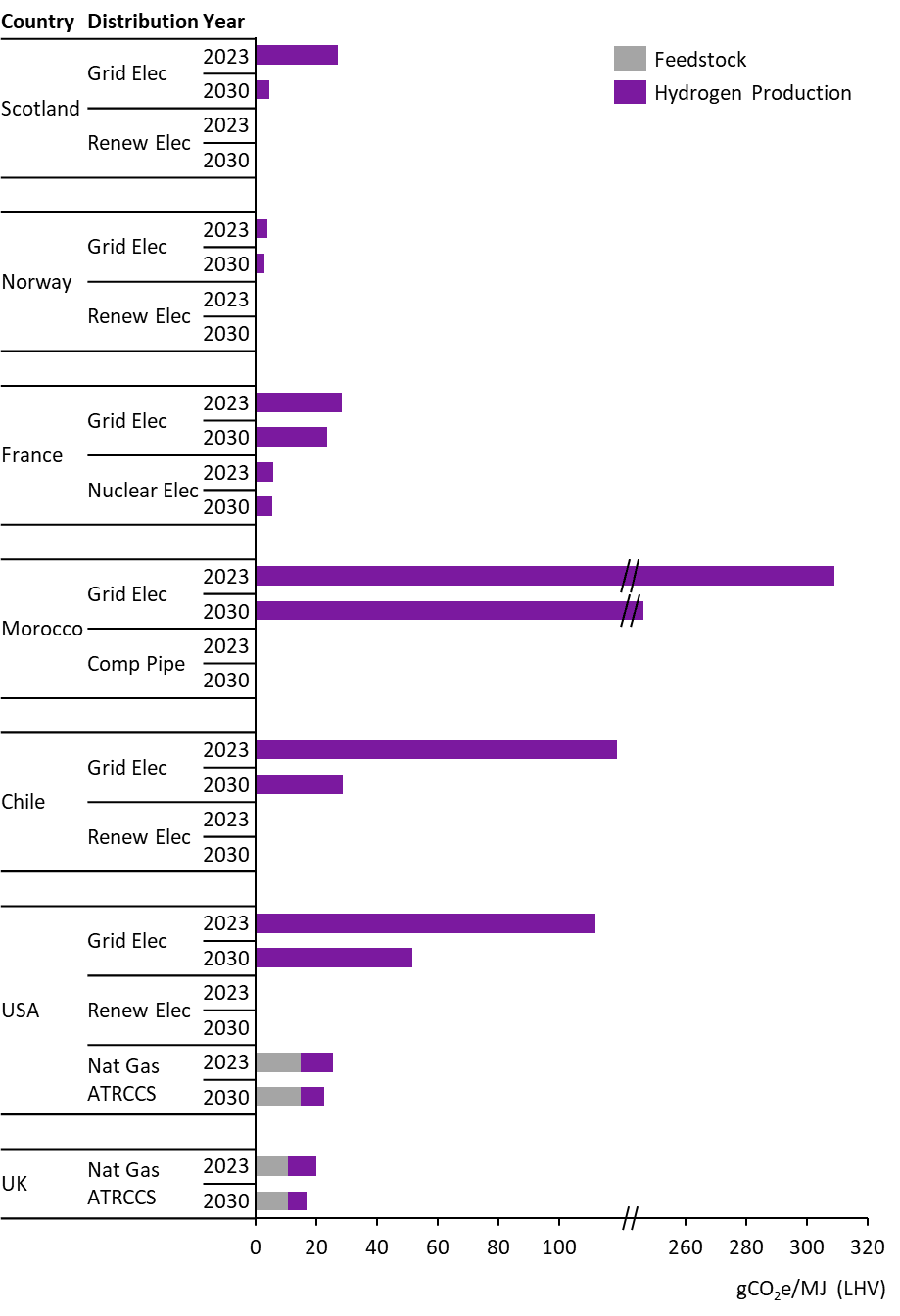

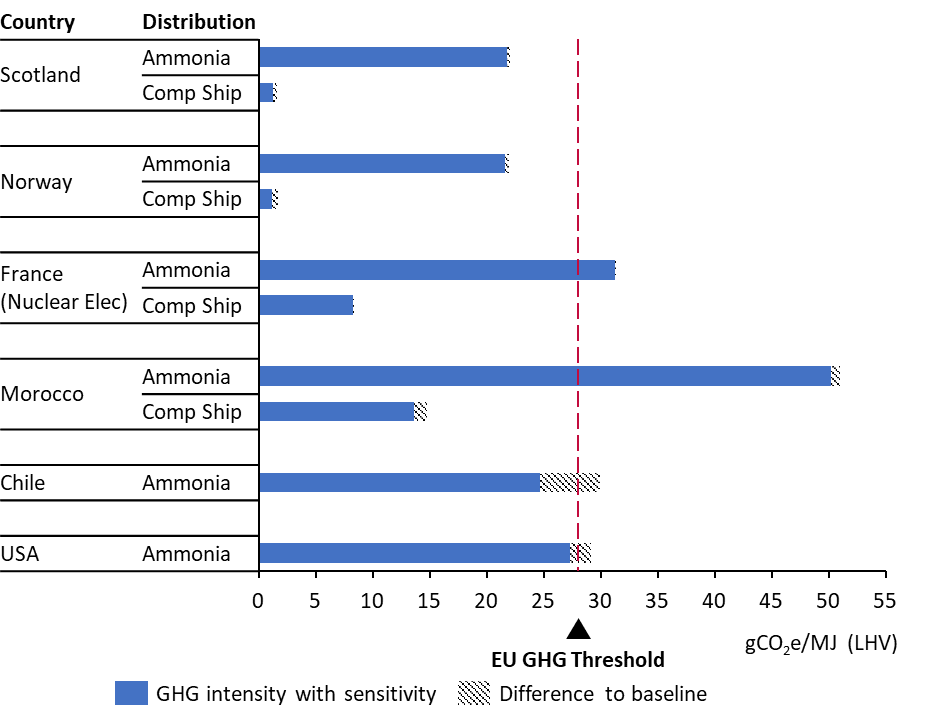

GHG emission results for hydrogen production pathways under ISO 19870 methodology

The GHG emission intensities of pathways modelled under the ISO methodology are shown below in Figure 7. Only emissions from feedstock and hydrogen production are modelled given the current ISO 19870 system boundary is “cradle to production gate” and does not include any downstream steps. There is also no GHG emissions threshold under ISO 19870, so compliance is not assessed.

Emissions for renewable electrolysis pathways are close to zero because there are only very small emissions for consumed water and minor chemicals. Emissions for delivered wind, hydro and solar electricity are considered to be zero, as in EU RED. Once again, grid electricity intensities dominate the grid electrolysis results.

For the natural gas reforming pathways, the difference in emissions between the UK and USA is mainly due to differences in upstream natural gas emissions intensities and grid electricity intensities. Under the ISO methodology, which allows producer, region or country-specific data to be used, the upstream natural gas intensities in the ISO analysis are assumed to be 8.7 and 9.2 gCO2e/MJLHV natural gas for the UK and USA respectively, based on current published UK and US government data.

These values could be significantly underestimating true upstream emissions, including the impact of LNG imports and methane leakage rates, and are lower than the generic single value the EU RED DA applies to all natural gas supplies (12.7 gCO2e/MJLHV natural gas). However, UK and US government data is likely to be updated more frequently (e.g. annually) in light of new evidence or updated gas source mixes compared to the single value published in the EU RED DA (which is based on the JEC WTT v5 study from 2020).

Those applying the ISO methodology are not required to use government estimates and could use other credible sources, including producer-specific data. This means that natural gas intensities under the ISO method are likely to vary significantly between projects, although where several credible options exist, there may be pressure from projects to choose lower values. In contrast, the EU Gas Directive requires the phasing in of producer-specific methane intensity data and does not give a choice as to which dataset to use.

The ISO 19870 method requires adjustments upwards for impurities by mass, and applies GWPs assuming the impurities are released. This may slightly affect the results, depending on the project-specific impurities. The engineering design data used assumes high purities (>99.9% by volume), so hydrogen product compositions were not modelled. However, for hydrogen production facilities that generate hydrogen at lower purities (e.g. 95-99% by volume), these impurity adjustments have a more significant impact, as hydrogen purity by mass is significantly lower than purity by volume.

Conclusions and recommendations

Key hydrogen standards globally already set out different GHG calculation methodologies and compliance requirements for producers. Hydrogen imported to the EU market must comply with rules set by the EU Renewable Energy Directive (RED) and the EU Gas Directive, if they are to contribute towards targets set under these policies. While an international standard is being developed (ISO 19870), it is unclear if the UK or EU will align with it in the future.

With regard to GHG emissions, electrolytic hydrogen produced in Scotland and exported to the EU market could be one of the most competitive among the countries we studied. Today, electrolytic hydrogen produced from renewable electricity in Scotland can already meet the EU RED GHG emission threshold. Further grid decarbonisation would increase the likelihood of compliance for grid connected electrolysis by 2030, even if the GB grid average factor has to be used under EU rules instead of the (much lower) Scottish grid average. Of the other countries considered in this study, only Norway with its hydro-electric dominated grid can deliver electrolytic hydrogen to the EU with lower GHG emissions than Scotland.

When transported over short distances as compressed hydrogen via pipelines or ships, electrolytic hydrogen produced using low-carbon electricity is expected to meet the EU GHG threshold. This applies in both 2023 and 2030 to renewable hydrogen produced in Scotland (930 km), Norway (1,312 km) and Morocco (2,747 km by ship, 1,930 km by pipeline), as well as nuclear electricity-derived hydrogen from France (261 km by ship, 435 km by pipeline).

Transporting hydrogen as ammonia leads to significantly higher GHG emissions. Producers relying on ammonia for long-distance transport from countries such Chile and the USA may need to adopt additional emission reduction measures to comply with EU policies, particularly if ammonia is reconverted to hydrogen for final use. Over shorter distances, hydrogen produced in Scotland or Norway using renewable electricity and transported as ammonia is likely to comply with the EU GHG emission threshold by 2030. However, in France, ammonia pathways will only meet the EU threshold if ammonia is used as the end-product in 2030 due to additional emissions from nuclear electricity inputs. Meeting the threshold requires further emission reduction measures such as using renewable electricity for hydrogen distribution.

Only countries with a high share of low-carbon electricity on their grid can produce grid-based electrolytic hydrogen meeting the EU GHG threshold. In 2023, grid electricity-based hydrogen from Norway can already meet the EU threshold when transported as compressed hydrogen. Scotland could also achieve compliance if compressed hydrogen is transported via pipelines. By 2030, all production pathways in Scotland can meet the EU threshold if the GHG intensity of grid electricity specific to Scotland decarbonises in line with policy aspirations. However, if GB’s grid emission intensity is used, only the hydrogen pipeline transport pathway could meet the threshold by 2030, assuming the grid decarbonises as planned. Hydrogen produced from fossil heavy electricity grid mixes such as those in Morocco, Chile and the USA will not be compliant.

Many natural gas pathways modelled will not comply with the EU Gas Directive threshold. These pathways are highly sensitive to the upstream GHG intensity of natural gas, which is uncertain and can be highly variable depending on the natural gas source (e.g. imported LNG with high intensities). Based on the default upstream natural gas intensity published in the EU RED Delegated Act 2023/1185 (as the EU Gas Directive Delegated Act is not yet finalised), natural-gas derived hydrogen produced in the UK could be compliant when piped or shipped as compressed hydrogen, giving it an emissions advantage over US natural gas-derived hydrogen (transported via ammonia).

GB’s electricity grid has a significantly higher GHG intensity than Scotland, so further clarity on the definition of bidding zones in the EU RED Delegated Act is critical. Using the GB grid average for grid-electrolysis projects in Scotland results in high risk of non-compliance with the EU GHG threshold (see Appendix F for results of this analysis), whereas use of grid GHG intensity data specific to Scotland would confer significant advantages on grid electrolysis projects, including exemptions from some EU requirements.

This GHG emission analysis could be combined with the previous CXC cost analysis to evaluate the overall competitiveness of these hydrogen pathways. Further work could also provide a view on the costs of adopting the different emission reduction measures discussed in the sensitivity analysis section of this report. Appendix H provides an abatement cost methodology, to calculate the minimum cost of compliance for those pathways above the EU GHG threshold but where emissions reduction measures could lead to compliance. We also note that implementation of the hydrogen and ammonia pathways modelled in this study may require significant investment in new infrastructure for some countries, and these infrastructure needs and any first-mover advantages could be investigated further.

Recommended next steps

The following recommendations could be considered for follow-on work:

- Expand the sensitivity analysis to cover additional sensitivities:

- Low-emission trucking

- Nitrous oxide mitigation

- Sensitivities in 2023, given several grid-electrolysis pathways do not consider any sensitivities in 2023

- Expand the analysis to include:

- Other distribution options e.g. methanol, liquid organic hydrogen carriers (LOHC)

- Additional time periods e.g. 2040 and 2050

- Additional emerging export regions e.g. Oman, Egypt, Australia, Namibia

- Combine the previous CXC cost analysis with the GHG emission analysis in this study to evaluate the overall competitiveness of the hydrogen and ammonia pathways

- Integrate upstream fossil fuel emissions intensity data once more reliable data is available e.g. EU methane regulations, any UK studies

We also suggest engagement with policymakers on the following aspects:

- Confirm with the European Commission whether Scotland counts as a country with its own GHG intensity or whether the GB grid bidding zone takes priority

- The EU Gas Directive Delegated Act as it is finalised and published, as interpretation of these rules could significantly impact fossil pathways

- The potential impacts of ISO 19870 once published, including the level of EU engagement or willingness to align with the standard, and when downstream hydrogen vectors e.g. ammonia will be included in future iterations of ISO 19870.

References

Arup. (2024). Cost reduction pathways of green hydrogen production in Scotland – total costs and international comparisons. Available at: https://www.climatexchange.org.uk/projects/green-hydrogen-production-and-international-competitiveness/

BEIS. (2023). Decarbonisation of the power sector. Available at: https://committees.parliament.uk/publications/39325/documents/193081/default/

CertifHy. (2023). SD Carbon footprint calculation. Available at: https://www.certifhy.eu/wp-content/uploads/2023/03/CertifHy_Carbon-footprint-calculation_220214.pdf

CertifHy. (2022). CertifHy-SD Hydrogen Criteria. Available at: https://www.certifhy.eu/wp-content/uploads/2022/06/CertifHy_H2-criteria-definition_V2.0_2022-04-28_endorsed_CLEAN-1.pdf

CERTIFHY. (n.d.). CERTIFHY DOCUMENTS – CERTIFHY. Available at: https://www.certifhy.eu/certifhy-documents/

Circularise. (2022). Four chain of custody models explained. Available at: https://www.circularise.com/blogs/four-chain-of-custody-models-explained

Department for Energy Security & Net Zero (DESNZ). (2023). UK Low Carbon Hydrogen Standard. Available at: https://assets.publishing.service.gov.uk/media/6584407fed3c3400133bfd47/uk-low-carbon-hydrogen-standard-v3-december-2023.pdf

Ding, Y., Baldino, C. and Zhou, Y. (2024). Understanding the proposed guidance for the Inflation Reduction Act’s Section 45V Clean Hydrogen Production Tax Credit. Available at: https://theicct.org/wp-content/uploads/2024/03/ID-132-%E2%80%93-45V-hydrogen_final2.pdf

E4tech. (2021). Options for a UK low carbon hydrogen standard Final report. Available at: https://assets.publishing.service.gov.uk/media/616012fce90e071979dfebba/Options_for_a_UK_low_carbon_hydrogen_standard_report.pdf

Ember. (n.d.). Electricity Data Explorer | Open Source Global Electricity Data. Available at: https://ember-climate.org/data/data-tools/data-explorer/

European Union. (2023a). DIRECTIVE (EU) 2023/2413 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 18 October 2023 amending Directive (EU) 2018/2001, Regulation (EU) 2018/1999 and Directive 98/70/EC as regards the promotion of energy from renewable sources, and repealing Council Directive (EU) 2015/652 (EU RED III). Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:02018L2001-20220607

European Union. (2023b). Commission Delegated Regulation (EU) 2023/1184 of 10 February 2023 supplementing Directive (EU) 2018/2001 of the European Parliament and of the Council by establishing a Union methodology setting out detailed rules for the production of renewable liquid and gaseous transport fuels of non-biological origin. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv%3AOJ.L_.2023.157.01.0011.01.ENG&toc=OJ%3AL%3A2023%3A157%3ATOC

European Union. (2024a). Directive – EU – 2024/1788 of the European Parliament and of the Council of 13 June 2024 on common rules for the internal markets for renewable gas, natural gas and hydrogen. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:L_202302413

European Union. (2024b). Texts adopted – Common rules for the internal markets for renewable gas, natural gas and hydrogen (recast) – Thursday, 11 April 2024. Available at: https://www.europarl.europa.eu/doceo/document/TA-9-2024-0283_EN.html

European Union. (2024c). Methodology to determine the greenhouse gas (GHG) emission savings of low-carbon fuels. Available at: https://ec.europa.eu/info/law/better-regulation/have-your-say/initiatives/14303-Methodology-to-determine-the-greenhouse-gas-GHG-emission-savings-of-low-carbon-fuels_en

European Union. (2024d). Regulation (EU) 2024/1787 of the European Parliament and of the Council of 13 June 2024 on the reduction of methane emissions in the energy sector and amending Regulation (EU) 2019/942. Available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:L_202401787

GHG Protocol. (n.d.). GHG Protocol Scope 2 Guidance. Available at: https://ghgprotocol.org/sites/default/files/2023-03/Scope%202%20Guidance.pdf

GH2 Standard. (2023). The Global Standard for Green Hydrogen and Green Hydrogen Derivatives. Available from: https://gh2.org/sites/default/files/2023-12/GH2_Standard_2.0_Dec%202023.pdf

International Partnership for Hydrogen and Fuel Cells in the Economy (IPHE). (2023). Methodology for Determining the Greenhouse Gas Emissions Associated with the Production of Hydrogen. Available at: https://www.iphe.net/_files/ugd/45185a_8f9608847cbe46c88c319a75bb85f436.pdf

International PtX Hub. (2023). Introduction to the IPHE methodology. Available at: https://ptx-hub.org/wp-content/uploads/2023/08/International-PtX-Hub_202308_IPHE-methodology-electrolysis.pdf

International Organization for Standardization (ISO). (2023). ISO/TS 19870:2023. Hydrogen technologies — Methodology for determining the greenhouse gas emissions associated with the production, conditioning and transport of hydrogen to consumption gate. Available at: https://www.iso.org/standard/65628.html

Martin, P. (2023). France to launch €4bn contracts-for-difference programme to support clean hydrogen production | Hydrogen Insight. Available at: https://www.hydrogeninsight.com/policy/france-to-launch-4bn-contracts-for-difference-programme-to-support-clean-hydrogen-production-reports/2-1-1508431

République Francaise. (2024). Decree of 1 July 2024 specifying the greenhouse gas emissions threshold and the methodology for qualifying hydrogen as renewable or low-carbon. Available at: https://www.legifrance.gouv.fr/jorf/id/JORFTEXT000049870616

Scottish Government. (2022). Hydrogen action plan. Available at: https://www.gov.scot/publications/hydrogen-action-plan/pages/3/

Scottish Renewables. (2021). Renewable Energy Facts & Statistics | Scottish Renewables. www.scottishrenewables.com. Available at: https://www.scottishrenewables.com/our-industry/statistics

TÜV Rheinland. (2023). Standard H2.21 Renewable and Low-Carbon Hydrogen Fuels. Available at: https://www.tuv.com/content-media-files/master-content/global-landingpages/images/hydrogen/tuv-rheinland-hydrogen-standard-h2.21-v2.1-2023-en.pdf

TÜV SÜD. (2021). Standard CMS 70 Production of green hydrogen (GreenHydrogen). Available at: https://www.tuvsud.com/en-gb/-/media/global/pdf-files/brochures-and-infosheets/tuvsud-cms70-standard-greenhydrogen-certification.pdf

US Department of Energy (DOE). (2024). Guidelines to Determine Well-to-Gate Greenhouse Gas (GHG) Emissions of Hydrogen Production Pathways using 45VH2-GREET Rev. March 2024. Available at: https://www.energy.gov/sites/default/files/2024-05/45vh2-greet-user-manual_may-2024.pdf

Appendices

Appendix A Definitions

Chain of custody

There are 4 types of chain of custody models to trace sustainability throughout supply chains. They are listed below in order of high to low level of physical connection required (Circularise, 2022).

|

Identify preservation – this model does not allow the certified product from a certified site to mix with other certified sources. It requires tracking the actual molecule of the material as they move through the supply chain. |

|

|

Segregation – this model requires the certified product from a certified site to be kept separately from non-certified sources. However, it allows different certified sources to be mixed if they share the same defined standard. |

|

|

Mass balance – this model tracks the total amount of sustainable content through virtual balancing of physical allocation. It allows the mixing of sustainable and non-sustainable materials producers and end-users must operate within the same ecosystem (e.g. gas grid). |

|

|

Book-and-claim – the sustainable attributes are tracked virtually where sustainable and non-sustainable materials flow freely through the supply chain without the requirement of them being supplied and used in the same ecosystem. |

|

In addition to the 4 types of chain of custody models, some hydrogen standards also use Environmental Attribute Certificates (EAC). This is a mechanism to demonstrate to end-users that a product (e.g. hydrogen, electricity, biogas) is produced from renewable sources. EACs enable the decoupling of physical goods from their environmental attributes, and can take the form of guarantees of original (GOs), renewable electricity certificates (RECs), etc. EACs could adopt either a mass balance or book-and-claim chain of custody model, or a combination of both. As such and where possible, the report uses terms referenced directly in the hydrogen standards.

Emission allocation methods

Hydrogen production pathways can generate co-products. Consequently, the total emissions resulting from the hydrogen production (and its upstream emissions) should be divided between the hydrogen and its co-products where these co-products are valorised. Outputs that would normally be discarded or that do not carry any economic value are considered as wastes or residues and do not receive any emissions burden. There are multiple methods of assigning emissions to the co-products, as described below.

System expansion – In this method, co-products are considered alternatives to other products on the market. The emissions avoided as a result of this replacement is subtracted from the product system, whereby the remaining net emissions are assigned to the main product (e.g. hydrogen). This requires understanding of the counterfactuals (i.e. the GHG emission of the products being replaced).

Energy allocation – Emissions are assigned to each co-product based on their energy content (generally on the basis of lower heating values). This can also include application of Carnot efficiencies or enthalpy changes to only account for the useful heat contained within any steam/heat co-products.

Physical causality – This allocation method is specifically mentioned in EU RED for processes where the ratio of the co-products produced can be changed. In these processes, the allocation should be determined based on physical changes in emissions, by incrementing the output of just one co-product whilst keeping the other outputs constant.

Economic allocation – Emissions are allocated in proportion to the (co-)product economic values based on total revenues obtained for each.

Mass allocation – Rarely used, but emissions would be allocated in proportion to the (co-)product mass flows.

Appendix B Detailed review of international hydrogen standards

UK Low Carbon Hydrogen Standard (LCHS)

The UK’s Low Carbon Hydrogen Standard (LCHS) was published in 2022 to support the implementation of the UK Hydrogen Strategy, setting requirements that UK hydrogen projects must meet to access revenue support under the Hydrogen Production Business Model and/or the Net Zero Hydrogen Fund (DESNZ, 2023).

Eligibility

The LCHS is feedstock neutral, but hydrogen must be produced via an eligible pathway as shown in the summary table in Table 3. New pathways can apply to be added to this list.

The LCHS sets a maximum GHG emission threshold of 20 gCO2e/MJLHV of hydrogen product (DESNZ, 2023). This threshold is applicable to a ‘cradle-to-production gate’ system boundary, which includes emissions from feedstock production up to and including hydrogen production.

Hydrogen derived from biogenic inputs is required to satisfy biomass feedstock Sustainability Criteria (Land, Soil Carbon and/or Forest Criteria, following those established in EU RED), and >50% of any biogenic hydrogen must be derived from waste or residue feedstocks. Indirect land use change emissions are also required to be reported separately.

GHG calculation methodology principles

Under the LCHS, hydrogen producers using electricity must demonstrate one of the following electricity supply configurations:

- Power Purchase Agreement (PPA) with a specific generator or private network. Here, physical delivery including losses and 30 minute temporal correlation (showing delivered volumes of electricity at least match the electricity consumption) is required for producers to use the GHG intensity of that generator or private network; or

- Grid electricity supply, where the GHG intensity is determined by the 30 minute average grid factor (GB or Northern Ireland, as applicable); or

- Grid electricity that would otherwise have been curtailed, which is permitted to use nil GHG intensity.

Proof of renewable electricity additionality is not a requirement of the UK LCHS (e.g. new windfarms do not have to be built to supply a hydrogen production facility). The LCHS requires that the contracted electricity generator must be located within the UK but does not impose further geographical correlation rules.

The LCHS uses energy allocation to assign GHG emissions based on (co-)products’ lower heating value energy contents. When heat or steam are produced as co-products, Carnot efficiencies[5] are applied for the energy allocation. However, the LCHS also requires that pathways using waste fossil feedstocks account for their displaced counterfactual emissions (i.e. the emissions that would have occurred if the feedstock had not been diverted to hydrogen production), which is a partial inclusion of a system expansion method.

A pressure of 3MPa and purity of 99.9% by volume is used as a reference flow under the LCHS. If the hydrogen produced is below these values, the theoretical emissions from compression and/or purification required to reach the reference flow need to be added. No adjustment is made if hydrogen is produced above the reference flow values.

Other requirements

Under the UK LCHS, mass balance chain of custody is generally used for upstream supply chains. However, the LCHS also currently states that biomethane cannot be mixed with fossil natural gas at any point, i.e. imposing an identity preserved chain of custody for biomethane feedstocks.

Uncertainties and future direction

Uncertainties in the LCHS include if/when downstream emissions from producer to user might be included within the system boundary, if/when hydrogen producers will be able to report producer-specific upstream natural gas GHG intensities (given the current lack of methodology and paucity of fossil industry data), plus when fugitive hydrogen emissions might be accounted for (and at what Global Warming Potential). It is also unclear how the UK LCHS will interact with ISO-19870 once published.

EU Renewable Energy Directive (RED)

Under EU law, regulations are directly applicable and binding in all Member States without the need for national implementation. Directives, on the other hand, set goals that Member States must achieve, and require Member States to first transpose them into national law, which allows for differences in policy mechanisms to arise in how these goals are met.

The Renewable Energy Directive (RED) is the legal framework for the development of clean energy across all sectors of the EU economy which Member States must transpose into national law (European Union, 2023a). Unlike the UK LCHS which currently only determines the eligibility for domestic UK hydrogen production to receive financial support, the RED mandates renewable energy consumption more broadly. Under EU RED, both domestically produced and imported hydrogen can contribute towards Member States’ compliance with renewable energy targets (European Union, 2023a).

Eligibility

EU RED does not prescribe a list of eligible technology pathways but evaluates eligibility based on fuel type, which is defined by the feedstock used to produce hydrogen.

- Biofuel – hydrogen produced from biomass that meets RED sustainability criteria;

- Recycled carbon fuels (RCF) – hydrogen produced from waste streams of non-renewable origin (European Union, 2023a);

- Renewable fuel of non-biological origin (RFNBO) – hydrogen derived from renewable energy sources other than biomass.

When used in transport, biofuels, RCFs and RFNBOs must achieve at least 70% GHG emissions savings (variable depending on year of commissioning) compared to the fossil fuel comparator of 94 gCO2eq/MJ. This means that lifecycle GHG emissions must be below 28.2 gCO2eq/MJLHV hydrogen. This threshold is measured on a ‘cradle-to-use’ system boundary, which goes beyond the UK LCHS’s ‘cradle-to-production gate’ system boundary.

GHG calculation methodology principles

In the EU, rules determining the GHG emission intensity of electricity inputs are set by the Delegated Act (DA) on renewable electricity under EU RED (European Union, 2023b). This states that renewable electricity from direct connections and PPAs need to meet additionality requirements to be considered to have nil GHG impact. Grid connected facilities with PPAs must also fulfil temporal and geographical correlation requirements, with some exceptions.

- Additionality: Requires that hydrogen production is connected to new (i.e. less than 36 months before the electrolyser starts operation), rather than existing, renewable energy generation assets. Additionality is not required before 2028, and for plants built before 2028, it is only required starting in 2038. This is different to the UK LCHS, which does not have additionality requirements.

- Temporal correlation: Until 2030, this rule requires that hydrogen must be produced within the same calendar month as the renewable electricity used to produce it, and hourly thereafter (European Union, 2023b). This is more relaxed than the 30-minute requirement in the UK LCHS.

- Geographical correlation: Requires that the hydrogen producer must be in the same bidding zone as the renewable energy installation or in an interconnected bidding zone with day ahead prices higher than that of the renewable generation asset.

- Exceptions: Additionality is not required for renewable PPAs with temporal and geographical correlation where the emission intensity of the bidding zone is <18gCO2/MJe. Bidding zones with >90% renewables do not have to meet any of these three criteria provided that the load hours of the hydrogen production plant are lower than the grid’s renewability share.

Similar to the UK LCHS, the default allocation method for hydrogen production pathways under EU RED is based on lower heating value (LHV) energy content for any co-product fuel, electricity or heat/steam (applying Carnot efficiencies). However, EU RED states that if the plant can change the ratio of the co-products produced, physical causality allocation is used (see definition in Appendix A). If co-products are produced that have no LHV energy content (e.g. oxygen, chlorine), GHG emissions are shared among co-products through economic allocation, based on the average factory-gate values of the (co-)products over the last three years. As with the UK LCHS, waste fossil feedstocks used for RCF production account for their displaced counterfactual emissions. EU RED sets no reference flow, with purity and pressure requirements only determined by the end user.

Uncertainties and future direction

According to the DA on renewable electricity (European Union, 2023b), the GHG emission intensity of grid electricity is determined at the level of countries or at the level of bidding zones. Different bidding zones do not currently exist in the GB power grid, but it is unclear how the DA defines a country. If Scotland is defined as a country under the DA, grid electrolysis projects could claim nil emissions for their input electricity without having to meet rules on additionality, temporal and geographical correlation, as Scotland’s grid has more than 90% renewables (Scottish Renewables, 2021). This would be a significant advantage and allow these projects to reduce their input electricity costs due to the lower regulatory burden. But if not defined as a country under the DA, these projects would have to take the GHG intensity of the GB grid, which only had an approximately 50% renewable share in 2023 (Ember, n.d.), requiring producers to instead procure renewable electricity PPAs that meet additionality, temporal and geographical correlation rules to claim nil emissions for the input electricity.

There are also uncertainties as to how individual Member States will implement the latest revised version of the RED, given that there is a May 2025 deadline for RED III to be transposed into national laws. Even within the confines of RED III, the policy mechanisms created and pathways deemed eligible by Member States can vary across the EU.

EU Gas Directive

The EU Gas Directive (formally called the Directive on common rules for the internal markets for renewable gas, natural gas and hydrogen) was published in July 2024 as part of the Hydrogen and Decarbonised Gas Market Package, it established a framework for the development of the future gas market in the EU, and its scope includes renewable and low-carbon hydrogen. Renewable hydrogen is defined as bio-hydrogen and RFNBO hydrogen, which must follow RED requirements (European Union, 2024a), whereby the EU Gas Directive sets requirements for low-carbon nuclear and fossil-fuel based pathways (outside of fossil waste derived RCFs) that are not currently covered by RED. This policy shares many similarities with the methodology set under RED, including a GHG emission threshold of 28.2 gCO2e/MJLHV and a ‘cradle-to-use’ system boundary.

The European Commission has until July 2025 to adopt a Delegated Act (DA) specifying the GHG methodology for low-carbon fuels (other than RCFs) (European Union, 2024b). On September 27, 2024, a draft version of this DA was released for public consultation (European Union, 2024c).

This draft version sticks to the same RED renewable power sourcing rules (and does not expand them to nuclear or fossil + CCS generator PPAs), but also appears to have several differences to the RED methodology for RFNBOs. For example, carbon capture and utilisation (CCU) in permanently chemically bound products is currently permitted in the draft DA, and there are also more detailed CCS requirements including allowing solid carbon sequestration, but ruling out enhanced oil & gas recovery (European Union, 2024c). Upstream natural gas emissions are to be based on reported producer values under EU methane regulations (European Union, 2024d), but before these are available, a conservative value from the DA is to be used. However, it is unclear how the existing use/fate of fossil fuel feedstocks is to be interpreted, and whether this counterfactual term is to be ignored or would generate a large emissions penalty or a large credit – both latter options would be a major departure from the attributional GHG methodology used in the RED and other EU legislation. Given the current consultation stage, other significant changes to the DA before final publication are possible, which also adds uncertainty.

CertifHy

CertifHy is an industry developed voluntary Guarantee of Origin (GO) certificate scheme within the EU, the European Economic Area and Switzerland. The CertifHy GO scheme verifies the origin (e.g. production location, production technology, feedstocks etc.) and GHG emissions of hydrogen products (CertifHy, n.d.). Rather than a set of legislative requirements, it is a scheme that producers can choose to participate in to demonstrate sustainability to their end-users.

Eligibility

CertifHy hydrogen can be labelled “green hydrogen” which covers renewable pathways, or “low-carbon hydrogen” which covers low-carbon fossil and nuclear pathways. For both, a GHG emissions threshold of 36.4gCO2e/MJ LHV hydrogen applies, which is measured on the same ‘cradle-to-production gate’ system boundary as the UK LCHS. This represents a reduction of 60% compared to the benchmark fossil process of 91gCO2e/MJLHV hydrogen product (via steam reforming of natural gas) (CertifHy, 2022).

GHG calculation methodology principles

When producing hydrogen from the electricity grid, the renewable origin can be established by cancelling of GOs[6]. Unlike the UK LCHS and EU RED, CertifHy does not specify further requirements such as additionality, temporal or geographical correlation.

Under CertifHy, co-products are dealt in different ways and are defined based on the production pathways. For pathways producing steam as a co-product, CertifHy requires its producers and consumers to use the same allocation method. Economic allocation is applied for hydrogen produced from chlor-alkali processes and its co-products. However, the method for allocating emissions to any co-produced oxygen from electrolysis is yet to be adopted (CertifHy, 2023).

Other requirements

The CertifHy GO scheme allows for the decoupling of physical hydrogen supply and its environmental attributes, via a book & claim system.

Uncertainties and future direction

The future use of this voluntary scheme and others such as TÜV SÜD and TÜV Rheinland could be impacted by the potential future alignment with ISO 19870.

France Energy Code L. 811-1

In July 2024, France transposed the definition of renewable hydrogen in alignment with EU RED under L. 811-1 of the Energy Code (République Francaise, 2024). It is a government developed standard and mandatory for accessing subsidy schemes.

Eligibility

As it is a transposition of EU RED, requirements for renewable hydrogen follow EU RED. The Energy Code also specifies the GHG methodology for low-carbon hydrogen, which is based on EU RED rules, but allows electricity from nuclear power generation.

Uncertainties

Recent Government changes in France resulted in a pause in publishing the new hydrogen strategy and subsequent Government funding in the form of a CfD for hydrogen developers producing renewable or low-carbon hydrogen. It is also currently unclear if France permits RCFs to count towards the REDIII renewable energy target (Martin, P., 2023).

United States Inflation Reduction Act 45V Tax Credit

The Inflation Reduction Act (IRA) introduced the Clean Hydrogen Production Tax Credit (PTC) (45V) to promote the production of low-carbon hydrogen in the US. This tax credit can be claimed by producers for every kilogram of eligible hydrogen they produce in the US. The value of the tax credit is determined by a tiered approach based on the GHG emissions intensity of the hydrogen with significant multipliers also available if the production facility meets the labour requirements set out under the tax credit.

Eligibility

Eligibility for 45V is determined by whether the produced hydrogen meets GHG emission thresholds, which is measured on a ‘cradle-to-production gate’ system boundary. The maximum GHG threshold is defined at 4 kgCO2e/kg H2. Hydrogen produced with lower GHG emissions is eligible for higher support, which is determined by a percentage of the maximum credit value[7] as seen in table below.

|

kgCO2e/kg hydrogen |

gCO2e/MJLHV |

% of Production Tax Credit value |

|

>4 |

>33.3 |

0% |

|

2.4 to 4 |

20 to 33.3 |

20% |

|

1.5 to 2.5 |

12.5 to 20 |

25% |

|

0.45 to 1.5 |

3.8 to 12.5 |

33.4% |

|

<0.45 |

<3.8 |

100% |

GHG calculation methodology principles

For electricity input for electrolytic hydrogen, rules to demonstrate renewability are similar to requirements set under EU RED’s DA. Producers must procure PPAs for renewable electricity that demonstrate incrementality (new generation capacity must begin operations within 3 years of hydrogen facility being placed into service, this is similar to the additionality concept in the EU), deliverability (clean power must be sourced from the same region), and temporal correlation (annual matching is until 2028, with hourly matching thereafter).

The reference flow is set at 2MPa at 100% purity, rather than 3MPa and purity of 99.9% under the UK LCHS. Producing hydrogen below/above this reference flow means the GHG intensity is adjusted higher/lower. By contrast, only upwards adjustments are required for the UK LCHS.

Further differences include the allocation approach. In the US, a system expansion (displacement) approach is generally used for co-product allocation, instead of energy allocation as in the UK LHCS. The US method can therefore give significantly negative GHG intensities for hydrogen produced from organic waste based biomethane[8]. Additionally, 45V places a cap on the amount of steam that can claimed as co-product from natural gas reforming to avoid incentivising over-production of steam to lower hydrogen GHG emissions (US DOE, 2024).

Uncertainties and future direction

45V is currently undergoing consultation to seek industry opinion on methods to enable a virtual tracking system for both direct connection and mass balancing for biomethane and fugitive methane. This includes counterfactual assumptions for biomethane feedstocks, treatment of fugitive emissions, and how to track and verify biomethane through virtual systems. It appears likely that 45V will impose “incrementality” (additionality), temporal matching and deliverability requirements for biomethane but details are unknown at present (Ding et al., 2024). More broadly, while the IRA has been signed into law, a change in US administration could create instability regarding the future of this tax credit.

International Partnership for Hydrogen and Fuel Cells in the Economy (IPHE)

IPHE is an international inter-governmental partnership, which aims to develop a set of mutually agreed methodologies and an analytical framework to determine the GHG emissions of hydrogen production. Use of this methodology is voluntary and differs from other standards reviewed as it serves as a framework for determining GHG emissions of hydrogen production only and does not set any eligibility criteria.

Version 3 of IPHE defines GHG methodologies for electrolysis, steam cracking, fossil gas reforming with CCS, fossil (coal) gasification with CCS, biomass biodigestion (anaerobic digestion to biomethane) with CCS, and biomass gasification with CCS. The methodologies for other pathways will be developed in the future. Unlike other standards, IPHE does not provide guidance on any categories (e.g., “renewable” or “low-carbon”), and it does not stipulate any GHG emission intensity threshold. (IPHE, 2023). This is expected to be done by individual countries participating in IPHE, if they wish to do so.

GHG calculation methodology principles

The current IPHE guidance covers a ‘cradle-to-point of use’ system boundary, which includes supply chain steps to transport hydrogen from the producer to the end user, but not the final use of the hydrogen. This goes beyond the UK LCHS system boundary, but not quite as far as EU RED.