Onshore and inshore storage of carbon dioxide

July 2024

DOI: http://dx.doi.org/10.7488/era/4622

Executive summary

Scotland’s net zero 2045 ambition and updated Climate Change Plan require the rapid development of carbon capture and storage (CCS) and carbon dioxide removal (CDR). Current pathways to meeting statutory targets are dependent on large industrial clusters, funded by the UK Government.

Alternative pathways for the rapid decarbonisation of smaller, distributed biogenic sources of carbon dioxide (CO2) may be available, noting that these would be of an order of magnitude less than the industrial clusters, with the advantage of high-value CDR credits. This requires permits for storage sites within Scottish inshore waters which extend to 12 nautical miles from the coast, and policy coordination across capture, transport and storage.

This study explored the potential total CO2 storage capacity in Scottish inshore areas and the availability of onshore emissions originating from biomass, known as bio-CO2. The study also investigated if the distribution of potential sources and storage availability would make it possible to expedite Scotland’s CCS and CDR potential.

The capture of bio-CO2 is already a commercial success in Scotland, with an ambition to scale without subsidy to 1 million tonnes per year by 2030, which requires storage. Norway, Denmark and Iceland are selling CO2 storage at a premium, reflecting a supply-and-demand imbalance in regional storage availability.

Aims

This study aimed to assess the potential for developing CCS within 12 nautical miles of the Scottish shoreline – an area within Scottish Ministers’ competence. We explored the feasibility to deploy high-value capture and low-cost CO2 storage in Scotland and what the commercially viable total capacity for nearshore storage is likely to be. The outcomes also address the availability of bio-CO2, domestic CCS value chains, fit-for-purpose storage site licensing and high-value CDR certificates.

We propose that Scotland can make rapid progress by refocusing on domestic bio-CO2. These emissions are already being captured in Scotland at low cost and with simple technology.

We identified prospects within the 12 nm territorial waters. Developing secure storage of high value bio-CO2 within the Scottish jurisdiction can produce several financial benefits, including premium lease payments to Crown Estate Scotland, development of local skills and growth of new businesses. This has the potential to increase Scottish GDP by tens to hundreds of millions of pounds per year, as well as paying staff and corporate taxes.

Developing Scottish storage sites for CO2 provides elements of control over licensing and the pace of approval for carbon capture and storage. Developing secure storage of high value bio-CO2 within the Scottish jurisdiction can produce CO2 removals, equivalent to direct air capture but at much lower financial cost.

We reviewed the potential for the rapid licensing of inshore storage using a streamlined version of UK licensing. Four geographic areas of interest are ranked by maturity of evaluation. We examine when injection could start if all regulations were in place across the different authorities.

Findings

We addressed five elements of CCS: licensing, storage, sources, timeframes and cost. We found that it is theoretically possible to adopt a streamlined licensing framework; inshore storage is available for rapid appraisal, albeit at a very limited capacity compared to offshore; bio-CO2 sources are abundant across nine sectors with explosive growth potential driven by the global CDR market; timeframes can be measured in years with the potential to deliver operational injection of bio-CO2 before 2030; costs are competitive with UK clusters and export markets.

Licensing

- CO2 storage involves multiple activities under different licensing regimes.

- New regulations for CO2 storage are not required.

- Minor amendments to existing statutory instruments may be required.

- The amendments may be fast if based on existing UK regulations and the CCS Directive.

- A Crown Estate Scotland (CES) lease is also required.

- Consents may also be required from the Scottish Environmental Protection Agency (SEPA) and the Scottish Government’s Marine Directorate.

Storage

- Four areas have well data and seismic coverage.

- Only the Lybster oil field is a candidate for immediate development.

- The total expected nearshore capacity is 2 Mt without further extensive surveying.

- The Forth Basin is a low Technology Readiness Level research opportunity.

Sources

- We mapped 98 of the largest bio-CO2 sources in Scotland.

- Source emissions range from 2 to 360 kilotonnes per annum.

- Separation of CO2 from distilleries and biogas upgrading are low cost.

- Combustion sources are higher cost and are the largest sources and sectors.

- The source distribution across five clusters favours road transport to local storage.

Timeframes

- North Sea Transition Authority appraisal licences average five years and three months.

- Appraisal are followed by storage permits and 2 years of further site development.

- The fastest storage permits are issued in as little as three years.

- The fastest development of a site to first injection is around a year.

- Lybster permitting could be fast but requires further exploration of legal frameworks.

- Rapid progression is dependent on pre-existing data to confirm site suitability.

Costs

- Capture costs for separation sources are low, at £60 per tonne.

- Capture costs for combustion sources are higher, at £120 per tonne.

- Truck transport costs £20 per tonne per 100 miles, or £0.12/tonne/km.

- Storage costs for Lybster are £70 per tonne.

- The full chain CCS cost is £150 per tonne for separation within 100 miles of Lybster.

- Storage costs for sites further offshore are at least two to three times higher.

Revenue

- CDR credits on the European voluntary market are worth £297 per tonne.

- Taxing storage would be subject to further work by the Scottish Government.

- As a simple example, a 10% tax could yield between £7 and £30 per tonne per annum.

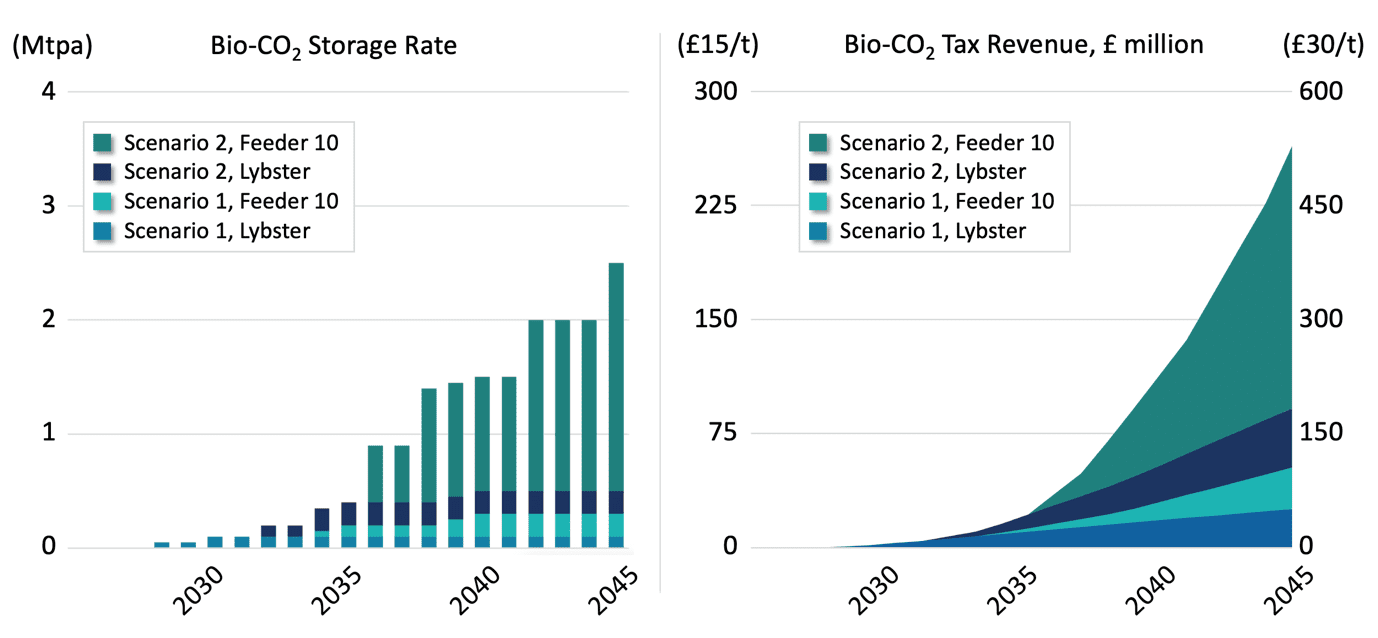

- Lybster tax revenue would be £30 million for a 2 Mt capacity and £15 per tonne tax.

- Further revenue is available if bio-CO2 is transported to Acorn via the Feeder 10 pipeline.

- Combined revenue for Lybster and Feeder 10 could total £250-500 million by 2045.

Next steps

In order to progress the potential benefits of CCS and CDR in Scotland, we recommend the following actions.

- The Scottish Government could conduct further work to fully understand the law around consenting and regulating storage and consider pursuing a streamlined regulatory framework for storage that builds on the structure established by the NSTA while emulating the accelerated approach taken by Denmark and Norway. This is relevant to Scottish policy, legislators, SEPA, and the Marine Directorate.

- The Scottish Government could consider supporting an appraisal of Lybster with the involvement of a compliant operator. This would require 3D seismic interpretation to build a static model and undertake reservoir simulation. This could be completed within one year with the intention of transitioning to a front-end engineering design study and development decision within three years. This requires a competent person’s report on the site, model outcomes, and risk analysis.

- The Forth Basin saturated water injection proposal could be considered as a potential research pilot to mature the concept and location from its current low TRL. This is relevant to the Scottish universities’ research community and British Geological Survey.

- Maturing the Fraserburgh and Solway Firth areas could proceed when market signals support the necessary investment in data acquisition and offshore development.

- The Scottish Government could seek mechanisms and policies to maximise the domestic benefits of full chain CCS, rather than exporting captured bio-CO2 to storage providers in other countries. The high concentration of bio-CO2 sources in the central belt raises the possibility of a gathering station for Feeder 10 access to Acorn.

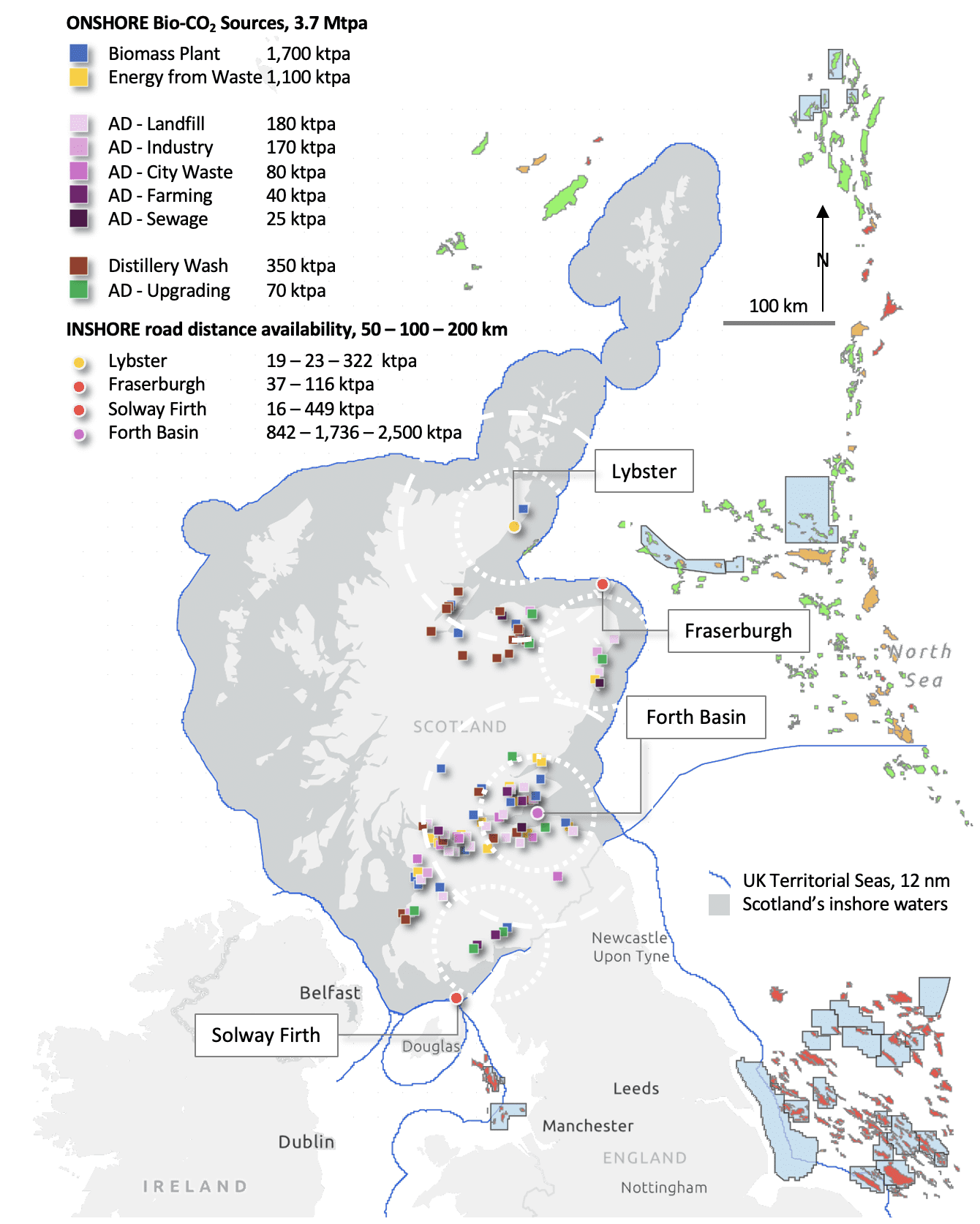

Onshore bio-CO2 sources located close to inshore CO2 storage prospects.

(Sources: SCCS, BGS, SNZR, NNFCC, NSTA)

List of abbreviations

|

AD |

Anaerobic Digester |

|

AOI |

Area of Interest |

|

BEIS |

Department for Business, Energy, and Industrial Strategy |

|

BSA |

Boston Square Analysis |

|

Bio-CO2 |

CO2 from decomposition, digestion, or combustion of biomass |

|

CCS |

Carbon Capture and Storage |

|

CDR |

Carbon Dioxide Removal |

|

CES |

Crown Estate Scotland |

|

DECC |

Department of Energy and Climate Change |

|

DESNZ |

Department for Energy Security and Net Zero |

|

DF |

Distillery Fermentation |

|

EfW |

Energy from Waste |

|

FEED |

Front End Engineering Design |

|

MD |

Marine Directorate |

|

Mtpa |

Million tonnes per annum, equal to 50 litres per second of CO2 |

|

NSTA |

North Sea Transition Authority |

|

OGA |

Oil & Gas Authority, the legal entity for the NSTA |

|

P90-P50-P10 |

Pessimistic-Expected-Optimistic range |

|

SEPA |

Scottish Environmental Protection Agency |

Glossary

|

Aquifer |

An aquifer is an underground layer of water-bearing rock, consisting of porous and permeable materials such as sandstone and chalk. |

|

Biomethane |

Biomethane is methane gas, CH4, that has been produced from the anaerobic digestion of organic matter such as manure, sewage, and organic waste. |

|

Biomethane Upgrader |

A biomethane upgrader is a piece of equipment that transforms biogas to biomethane by filtering out impurities such as other gases that are also generated during anaerobic digestion. |

|

Caprock |

A relatively impermeable rock, commonly shale, anhydrite, or salt, that forms a barrier or seal above and around reservoir rock so that fluids cannot migrate out of the reservoir. |

|

Inshore |

Inshore is a marine area adjacent to the coast of a state or jurisdiction. The inshore area for Scotland is synonymous with the territorial waters that extend 12 nm beyond the coastline. |

|

Regional Aquifer |

A regional aquifer is a water-bearing reservoir that extends laterally for 10s to 100s of km, reflecting a thick regional distribution of the reservoir rock such as a sandstone or chalk. |

|

Seismic |

Seismic in this context refers to the geophysical surveying technique of imaging the geologic structure of the subsurface by using vibrational waves and sonic reflections. |

|

Syncline |

A trough of stratified rock in which the beds dip toward each other from either side to form a u-shaped or v-shaped structure along a geometric axis. |

Introduction

The following report consists of five sections that cover CO2 storage licencing, inshore storage opportunities, available sources of bio-CO2, storage development timeframes, and a cost-revenue analysis of onshore capture, transport, and inshore storage. The report closes with six questions and answers that aim to synthesise the outcomes and propose ways forward.

Licensing

The Energy Act 2008 first enabled CO2 storage in the UK. The Carbon Dioxide Regulations 2010 adopted many requirements of the EU CCS Directive 2009 on the geological storage of carbon dioxide and came into force October 2010 – Appendix A. The regulations were extended in 2011 to address the termination of licences. The CCS Directive was transposed into UK law in 2012 by the adoption of secondary legislation under the authority of the Energy Act 2008.

CCS Directive

An EU regulatory framework for CCS was first proposed by the European Commission in 2007 (EC, 2007). The CCS Directive 2009 provides the framework for CO2 storage with only brief mentions of capture and transport. The CCS Directive is supported by a series of six guidance documents. The guidance covers: the storage complex, characterisation, risk management, stream composition, monitoring and corrective measures, criteria for the transfer of liability to the competent authority, and financial security and financial mechanisms. The Directorate-General for Climate Action (DG CLIMA) commissioned DNV in 2022 to revise the guidance documents to reflect the current understanding of CCS and remove ambiguities identified during the development of early CCS projects. The outcomes can be expected in Q3 2024.

Licensing in the UK

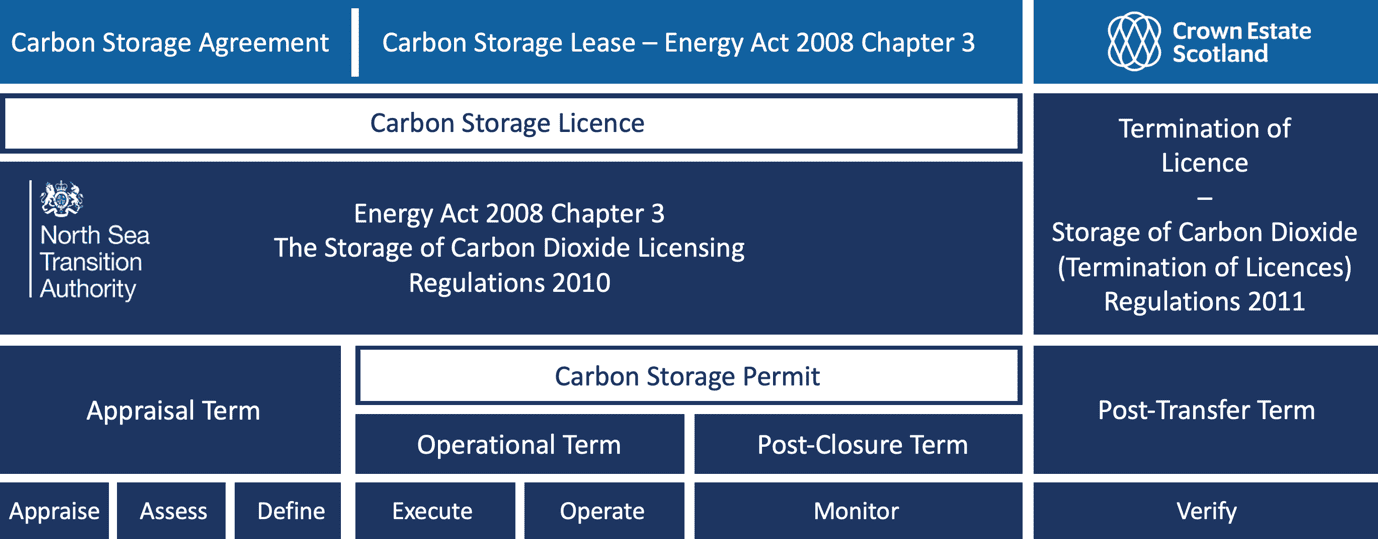

DESNZ currently leads UK government energy policy, preceded by BEIS (2016-2023) and DECC (2008-2016). UK energy policy is framed by HM Treasury budgeting and long-term planning. The Energy Act 2008 makes provision for gas storage, enabling the licensing of CO2 storage appraisals and CO2 storage permitting – Figure 1.

Figure 1. Current UK licensing framework for CO2 storage in Scotland for offshore areas such as Acorn.

UK licensing development

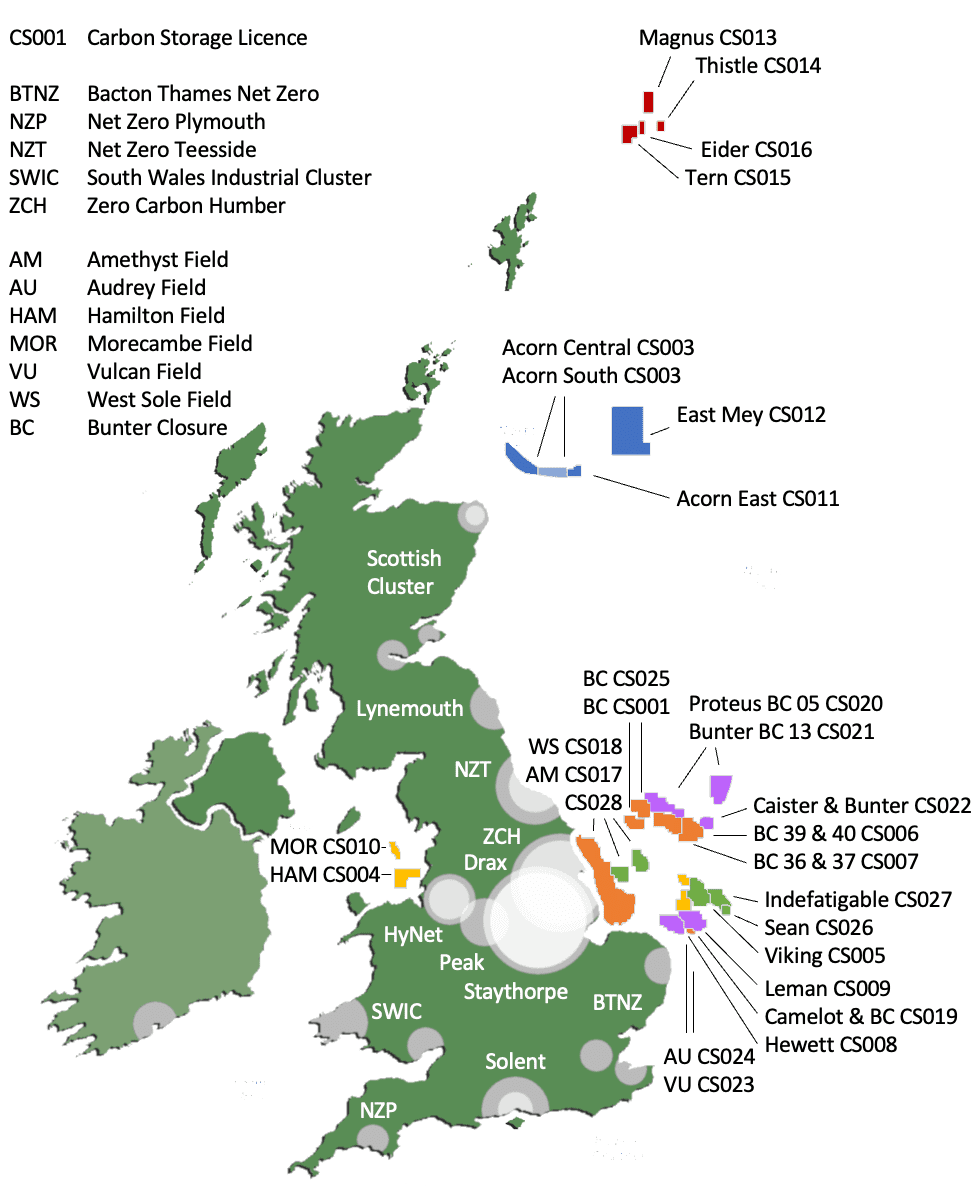

There are currently 27 UK appraisal licences open – see detail in Appendix B and Figure 2.

Figure 2. The location of offshore CO2 storage appraisal licences currently active in UK waters.

Licence CS001 and 1CS003-CS027). CS002 was reissued as CS003 in 2023.

Over a decade of policy engagement and early licensing experience has led to the current structure of appraisal licensing, storage permitting, and licence termination. The appraisal licence and storage permit terms both consist of three phases each:

- Appraisal licence phases: 1. Appraise 2. Assess 3. Define

- Storage permit phases: 4. Execute 5. Operate 6. Monitor

The seventh and final phase is a further monitoring period that occurs after the transfer of the site liability from the operator to the regulator with the termination of the storage permit. The seven phases are described in more detail below:

1. Appraise: This initial phase consists of an early risk assessment to establish storage feasibility and identify gaps which are then addressed by site characterisation. The characterisation of the trap structure may require 3D seismic acquisition over the site or reprocessing of an existing survey, and appraisal drilling.

2. Assess: This phase is a thorough evaluation of the site characterisation outcomes, and the operator’s proposed storage plan or need for further appraisal.

3. Define: This phase is a detailed proposal for site development commonly referred to as front end engineering and design (FEED). The design specification and required engineering informs a final investment decision and, if positive, an application for a storage permit.

4. Execute: On issuance of a storage permit, the operator executes the design plan. This entails the construction and commissioning of the engineering works necessary for CO2 injection into the target reservoir and for site conformance monitoring during the operational phase.

5. Operate: This phase commences with the first injection of CO2 and conformance to the operational plan. Any deviation from the planned operational conditions such as pressure excursions, flow impedance, or indications of out-of-zone migration are investigated and addressed to the satisfaction of the regulator, or otherwise promoted to a change in the operational plan up to and including a suspension of operations and early closure of the site.

6. Monitor: This phase commences with the end of injection and closure of the site and is a continuation of any preceding operational monitoring adapted to the specific requirements of conformance monitoring for the post-operational phase.

7. Verify: This phase commences with the end of the storage permit and transfer of site liability to the regulator. It consists of a sustained monitoring plan that verifies the long-term conformance of the site to expected outcomes.

The seven phases outline the structure of the current UK licensing regime – Table 1. In practice, each phase entails many elements that need to be negotiated between the operator and regulator. The negotiations are based on the specific requirements of a storage site and the evidence base of increasingly detailed assessments, characterisation, development proposals, and adaptation to conditions during the execution and operational phases.

Illustrating this, 17 of the 28 appraisal licences include between two and five additional requirements that apply during the initial appraisal phase to support characterisation – Table 2. These range from acquiring 3D seismic and drilling an appraisal well, to undertaking CO2 transport and topside installation studies, core sampling, and fault geomechanical analysis.

Table 1. Main stages of license progression

|

Main stages |

TLA |

Maturity |

|

Early Risk Assessment |

ERA |

Feasibility |

|

Characterise |

CH |

Appraisal |

|

Assess |

AS |

Pre-front-end engineering |

|

Define |

DF |

Front-end engineering design |

|

Permit Application |

PA |

FIP, firm intention to proceed |

|

Construct & Commission |

CX |

FID, final investment decision |

|

Operational |

OP |

OI, on injection |

|

Post-Closure |

PC |

Post-Closure monitoring |

|

Post-Transfer |

PT |

Post-Transfer monitoring |

Table 2. Additional licensing requirements.UK licensing structure

|

Additional Requirement |

Description of Requirement |

|

Seismic RP |

3D Survey reprocessing |

|

Seismic AQ |

3D Survey acquisition |

|

Well |

Appraisal drilling |

|

Injectivity |

Appraisal flow |

|

Wells VSP |

Vertical seismic profile |

|

Firm TR |

Transport study |

|

Firm TS |

Topside installation study |

|

Firm Geomech |

Geomechanical study |

|

Firm Cap |

Caprock seal study |

|

Firm Seal |

Fault seal study |

|

Firm Core |

Core analysis study |

Licensing in Scotland

Inshore developers in Scotland must first secure the appropriate rights to appraise and develop storage from the Crown Estate Scotland (CES). A CES agreement is required for a site appraisal. A CES lease is required for storage in accordance with the Energy Act 2008. The CES approach to managing storage assets is set out in the CCS Asset Profile (CES, 2022).

Onshore consent is covered by Scots law and is a matter for the local planning authority. Offshore consent for CO2 storage in territorial waters is also covered by Scots law, and requires coordination between the Scottish Environmental Protection Agency (SEPA), the Marine Directorate (MD) and the NSTA. The shared jurisdiction is discussed below.

Scots law

The territorial sea adjacent to Scotland is subject to both UK and Scots law. In terms of international law, the UK as the coastal state, enjoys sovereignty in the territorial sea which includes the seabed and subsurface. How the UK decides to exercise that sovereignty is a matter for the UK and this becomes complex in the context of devolution – Appendix C.

Licensing and regulation

Oil and gas fields under the territorial sea adjacent to Scotland are vested in the Crown. Although Scottish Ministers did receive licensing powers for oil and gas in the post-referendum settlement in the context of the Scotland Act 2016, this was explicitly only in relation to the onshore area, defined as lying within the baselines of the territorial sea – section 47. Licensing in relation to all offshore oil and gas, within the territorial sea and under the continental shelf, is a matter for the NSTA. This would be relevant to the closure of the oil production licence for Lybster in preparation for CO2 storage.

Scottish Ministers are established as the licensing for CO2 storage in the territorial sea by section 18 of the Energy Act 2008. The Storage of Carbon Dioxide Regulations 2010 went on to define a licence as granted by the authority, namely the NSTA – Regulation 1.3. However, the Storage of Carbon Dioxide Regulations 2011, a Scottish Statutory Instrument (SSI), transferred the powers to grant storage licences to Scottish Ministers, along with the associated powers to oversee the development, operation, monitoring, and closure of storage sites in Scottish territorial waters. This greatly simplifies the regulatory framework and requirements for licensing storage in Scottish waters.

Two points are worth noting. Firstly, the SSI precedes the 2012 transposition of the CCS Directive, and withdrawal of the UK from the EU in 2020. Very minor amendments to SSI 2011/24 may be required to reflect this. For example, the reporting authority named in the SSI is the European Commission.

Secondly, while the necessary powers sit with Scottish Ministers to oversee storage licensing, the competent authorities, and associated resources and procedures are not developed. Purchasing the services of the NSTA as regulator is an option that requires exploring. The long experience of the NSTA is an important supporting consideration. One option may be an agreement between an existing Scottish authority such as the Marine Directorate and the NSTA to deal with carbon licensing in territorial waters.

There is a precedent, the Memorandum of Understanding between the HSE and OPRED to form the Offshore Safety Directive Regulator, now OMAR, when that directive required a competent authority to deal with health, safety, and environmental risks under one roof (HSE, 2024). While that involved two regulators at UK level, there ought to be no objection to a similar arrangement between a UK and a Scottish regulator given the commonality of purpose and the desirability of a seamless approach.

Liability and ownership

Hydrocarbons in strata, even if residual and uneconomic, are vested in the Crown unless the Crown specifically transferred ownership, which it would be unlikely to do. Regarding liability for operational oil fields, the principal party is the licensee. In most cases, however, liability is joint and several with co-venturers under a joint operating agreement.

For decommissioning, it is a matter of anyone who holds a section 29 notice under the Petroleum Act 1998. Again, this will usually be co-venturers, but the list is lengthened to minimise the risk to the state if duty holders become insolvent. Things get more complicated in relation to any remaining infrastructure under an agreed derogation. Firstly, there is no specific legislation or regulation on this matter; rather it is dealt with in the context of guidance notes issued from time to time by OPRED. Leaving aside the apparent confusion in the guidance over ownership and section 29 notice holders – see Appendix C7. More fundamentally, there is an argument that the use of a Crown lease in relation to CCS constitutes an exercise of property rights. This raises the possibility that pre-existing infrastructure is a fixture in both jurisdictions. It follows that this belongs to the owner of the land or seabed to which it is attached. This has never been tested but is certainly arguable.

By contrast, this is a much easier proposition to establish within the territorial sea where the Crown Estate has habitually claimed property rights and the courts have readily confirmed them. Whatever is stated in the guidance notes and essentially accepted by duty holders in relation to decommissioning, property law may say something different.

Pore space

For Lybster, whereas the hydrocarbons in the field are vested in the Crown and those rights are exercised by the NSTA, the pore space is the property of the Crown. Property rights would be exercisable by the CES. For the Forth Basin, the pore space would also be owned by the Crown and the property rights would be exercisable by CES. Note that this property law analysis also implies that CO2 injected into depleted reservoirs beneath the territorial sea would be owned by the Crown on the basis of the principle of annexation. This has been more fully explored in the context of enhanced oil recovery (Patterson & Paisley, 2016).

Shared jurisdiction

The exploration and production licensing for Lybster at the time would have been a matter for the Secretary of State. Even now, as the reservoir lies within the territorial sea, the oil licensing would be a matter for NSTA. However, the CO2 storage licensing is a matter for Scottish Ministers. The siting and operation of the drilling rig onshore would then and now be a matter for the local planning authority. Thus, both UK law and Scots law are engaged as appropriate.

The Beatrice field presents a most interesting problem. The residual hydrocarbons in the field remain vested in the Crown. The pore space within 12 nm is owned by the Crown. The ownership of pore space beyond 12 nm is not clear, but from a practical perspective only the Crown has sovereign rights to act. The licensing authority within 12 nm is Scottish Ministers, and, beyond the 12 nm, NSTA. This may be resolved by some form of arrangement modelled on those for hydrocarbon reservoirs that cross boundaries.

Summary

CO2 storage involves multiple activities under different licensing regimes. These need to be explored further by the Scottish Government to fully understand what will be necessary to put in to law for CO2 storage within Scottish waters. New regulations will be required; it may well be, however, that insofar as existing regulations could be relied upon, the process of modifying SSI 2011/24 and drafting consents could be fast. This would really be a question for those with a better insight into the technical detail and political due process.

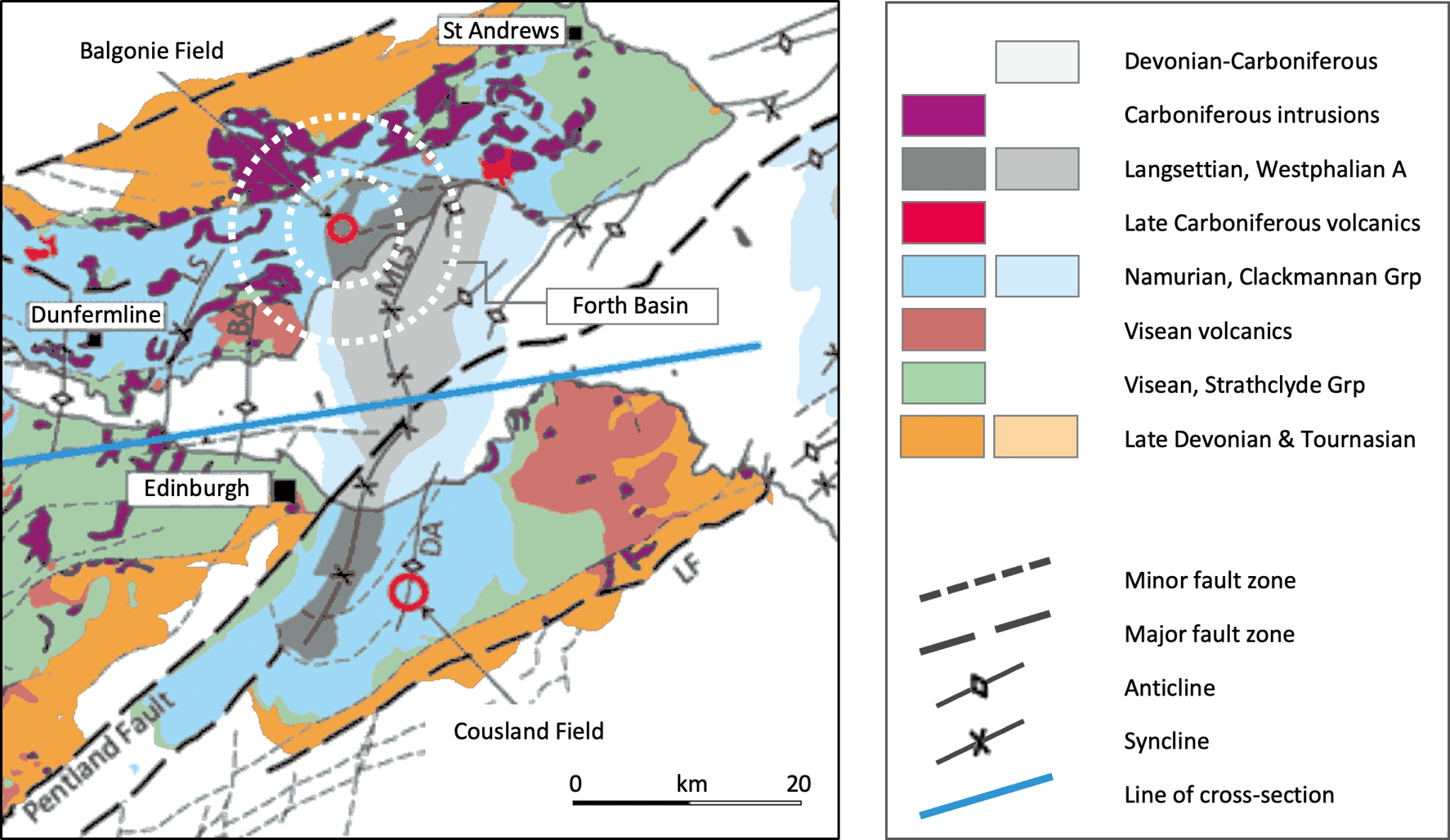

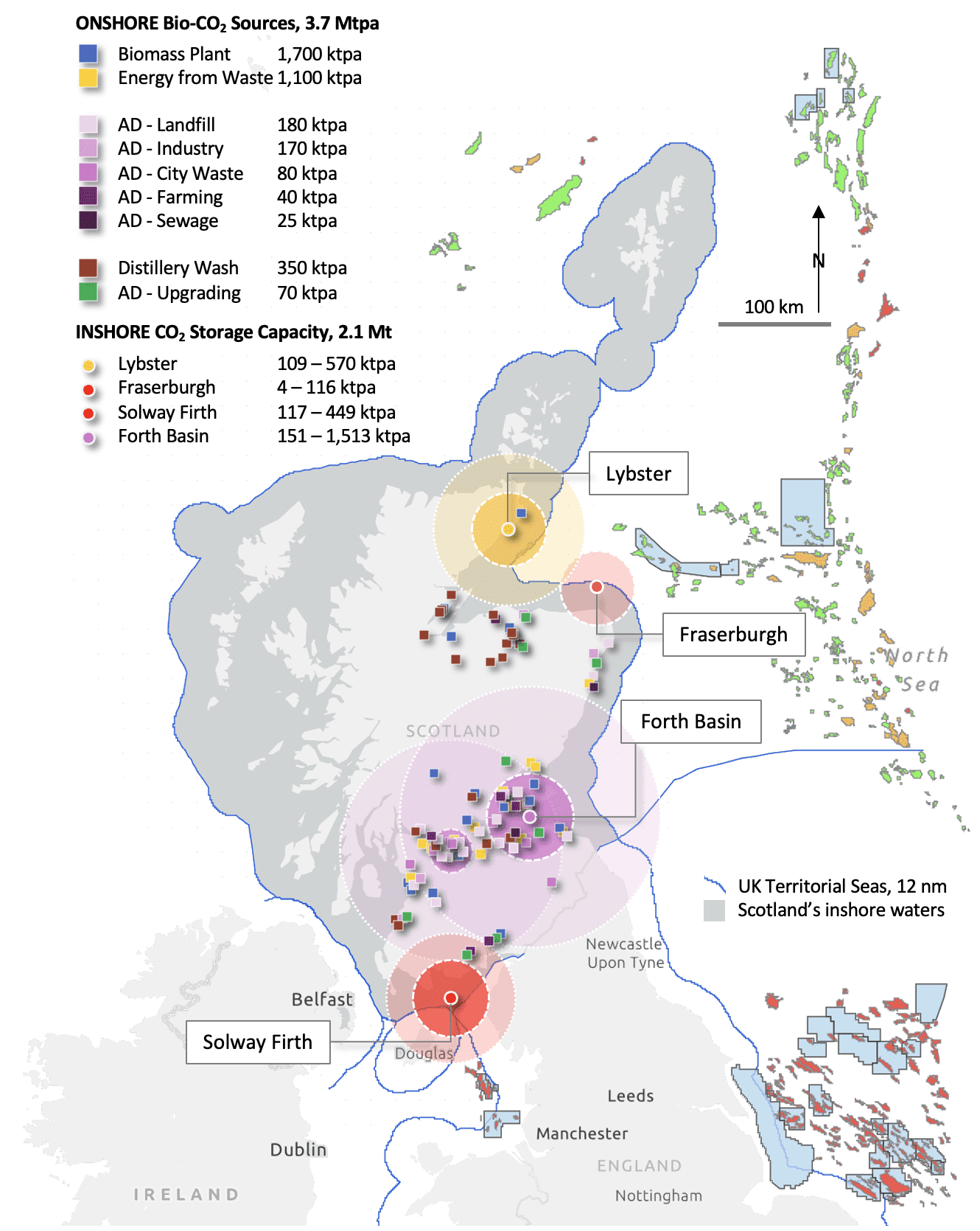

Inshore storage

Scotland’s territorial waters cover an area of 55,480 km2 with the potential for inshore storage. This includes a great deal of seismic data – Figure 3. While the 2D seismic coverage is extensive, only three areas have 3D seismic: Lybster, Fraserburgh, and the Solway Firth. 3D seismic is the most effective data for accurately characterising subsurface structures (Dee, et al., 2005). In its absence, 2D data may identify structures of interest in cross-section. The Forth Basin area is covered by a 2D survey – Appendix C. The availability of data allows the prospective areas to be ranked by maturity – Table 3. The exploration ranking of Fraserburgh and the Solway Firth is explained in the description of the areas of interest that follows below.

Areas of Interest

Figure 3 presents areas of interest for inshore CO2 storage.

Figure 3. Areas of interest for inshore CO2 storage. Four areas are identified with seismic coverage and exploration well data – see Annex E for an inventory. Lybster has the best data coverage (contingent), followed by Fraserburgh and the Solway Firth (prospective), and the Forth Basin (exploration).

Table 3. Inshore areas of interest ranked by maturity and potential to progress rapidly.

|

Areas of Interest |

Area Name |

Seismic & Wells |

Maturity |

|---|---|---|---|

|

AOI 1 |

Lybster |

RE07 3D seismic + 5 wells + model |

Contingent |

|

AOI 2 |

Fraserburgh |

PGS18 3D seismic + 3 wells |

Prospective |

|

AOI 3 |

Solway Firth |

ES94 3D seismic + 2 wells |

Prospective |

|

AOI 4 |

Forth Basin |

CN87 2D seismic + 1 well |

Exploration |

Lybster Area

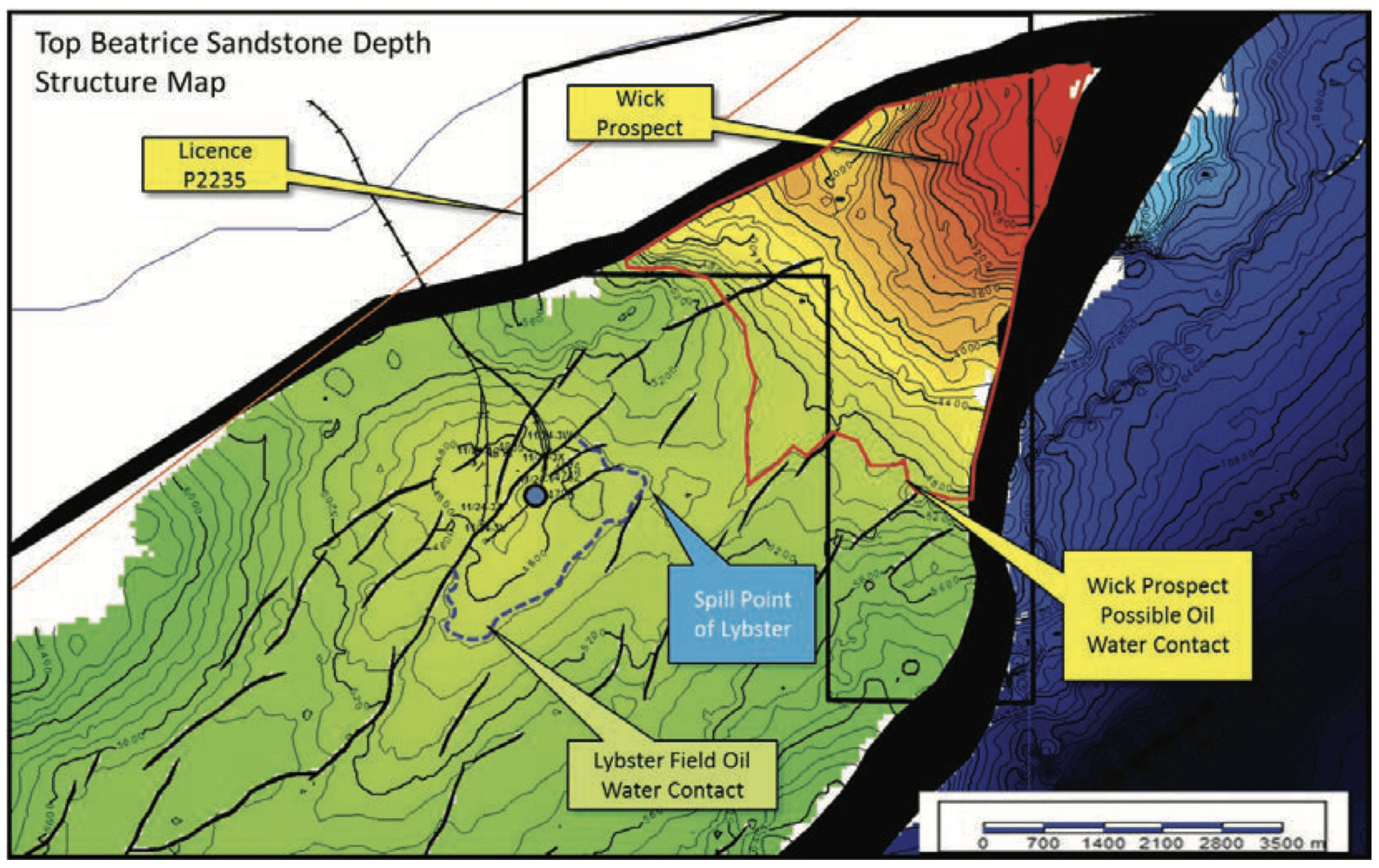

The Lybster oil field is ranked as contingent on the maturity pyramid where the maturity progresses from an exploration resource (large base) to a commercial reserve of sites (small top) via contingent prospects – Figure 3. The area of interest encompasses 306 km2 that include the field and exploration structures, Knockinnon and Braemore.

Two more oil fields, Beatrice and Jacky, are located at the 12 nm limit. Lybster is notable for three reasons: its proximity to the coast; a substantial amount of data and analysis; and an existing production well. These significantly reduce the potential cost and timeline to developing a storage site. The field needs to be screened for capacity and suitability to qualify the field for appraisal licensing. The initial capacity estimate and assessment of suitability are documented in Section 4.2, supported by Appendix D.

Knockinnon and Braemore are relatively immature with respect to storage analysis but noteworthy for potentially providing step-out capacity to Lybster. Beatrice has not been assessed for this report as the field is beyond a presumed technical limit for onshore development via extended reach wells. 12 nautical miles is equivalent to 22 km; the 2022 record for an extended reach well is 15 km. A reasonable economic limit of 10 km has been set for assuming offshore development. Beatrice, the largest field in the area, straddles the 12 nm boundary. Jacky is a small satellite field in territorial waters to the north of Beatrice.

Fraserburgh & Solway Firth

Both areas have 3D seismic survey coverage and exploration wells. The location of the 3 wells and seismic for Fraserburgh, approximately 16-20 km from shore, would require an offshore installation (pipeline, injection well, and monitoring equipment). Any prospects within the area would need to be identified from the existing seismic and well data and screened for suitable reservoir injectivity and caprock seal properties prior to appraisal licensing.

The Solway Firth area has two exploration wells and a 3D seismic survey in the southern half of the 12 nm territorial waters. One of the wells is within the seismic survey area. The location of the seismic and well 13 km from shore would require an offshore installation (pipeline, injection well, and monitoring equipment). As with Fraserburgh, prospects within the area would need to be identified from the existing seismic and well data and screened for suitable reservoir injectivity and caprock seal properties prior to appraisal licensing. As such, both areas are ranked as prospective on the maturity pyramid.

Forth Basin

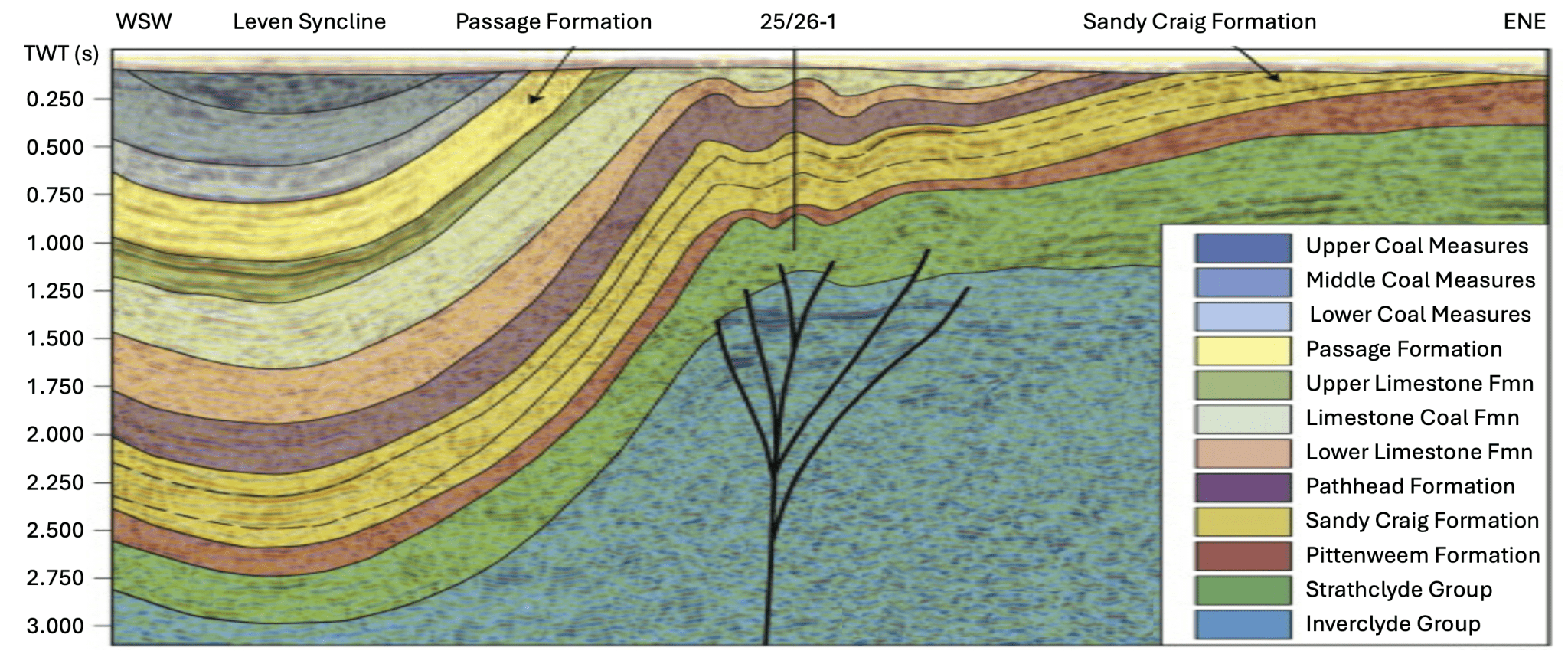

The Forth Basin is close to a diverse cluster of bio-CO2 sources located in the Central Belt. The Forth was screened for prospective storage sites as part of the CASSEM project (SCCS, 2012). Trap structures were identified but rejected due to a lack of well data and poor control on the 2D seismic interpretation for caprock thickness and reservoir volume (Monaghan et al., 2012). The Forth also contains a large basin, the Leven syncline. The syncline may be suitable for an alternative strategy of CO2-brine surface mixing and injection of the CO2-rich mixture which is denser than the syncline’s porewaters (Eke et al., 2011). This approach to storage is examined in section 2.3. The low TRL of dissolved CO2 injection and need to mature the concept for the Forth Basin rank this area as exploration.

Lybster prospect

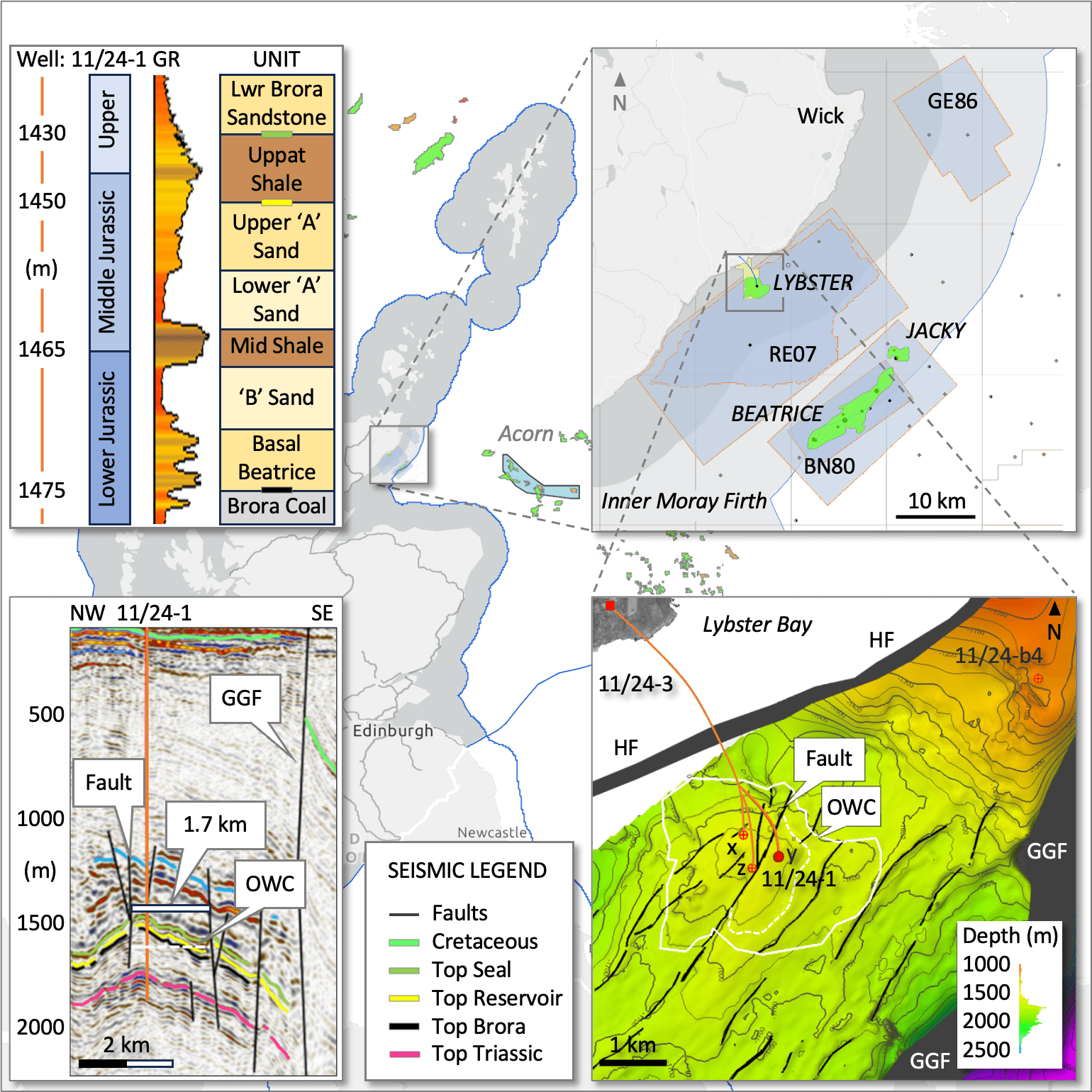

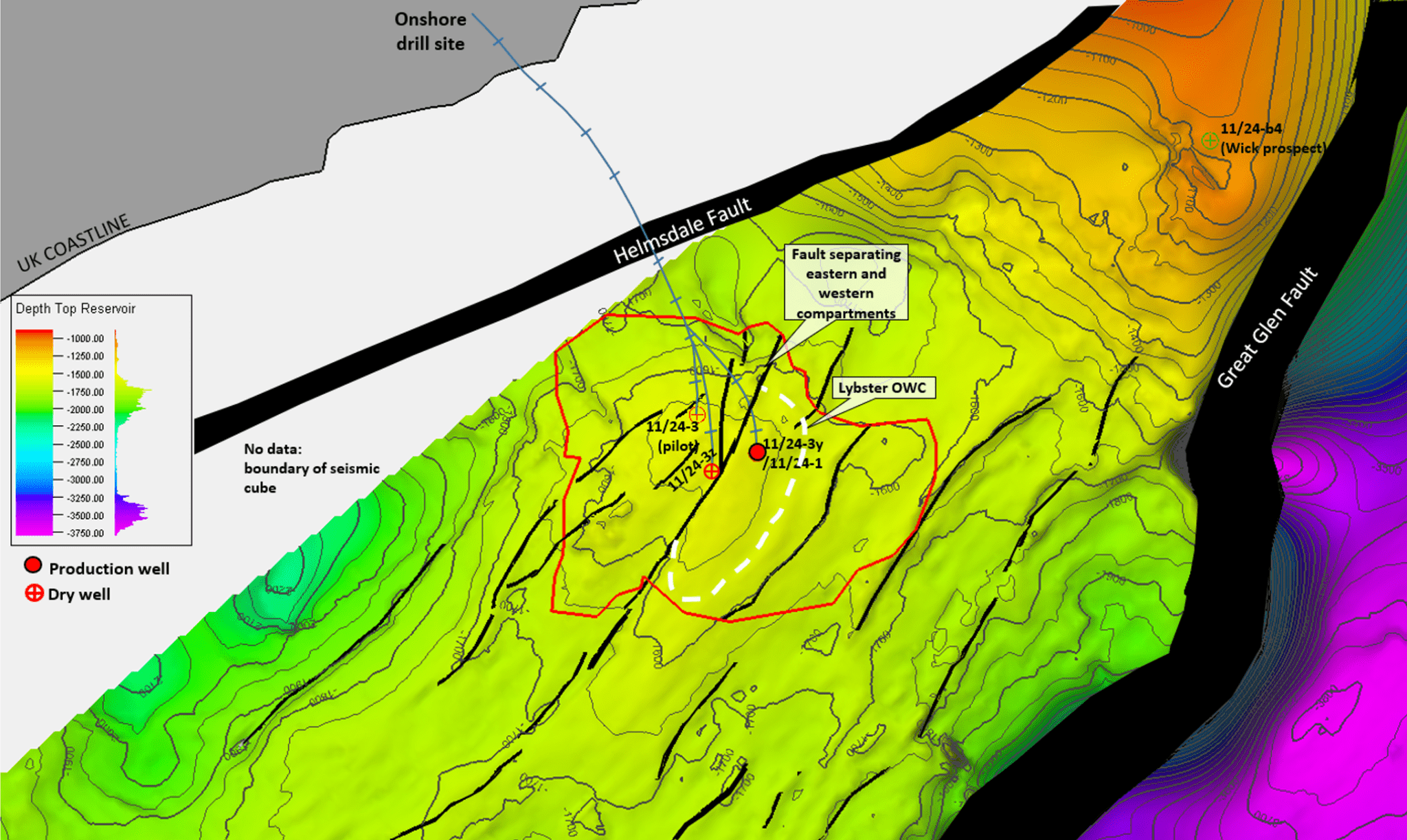

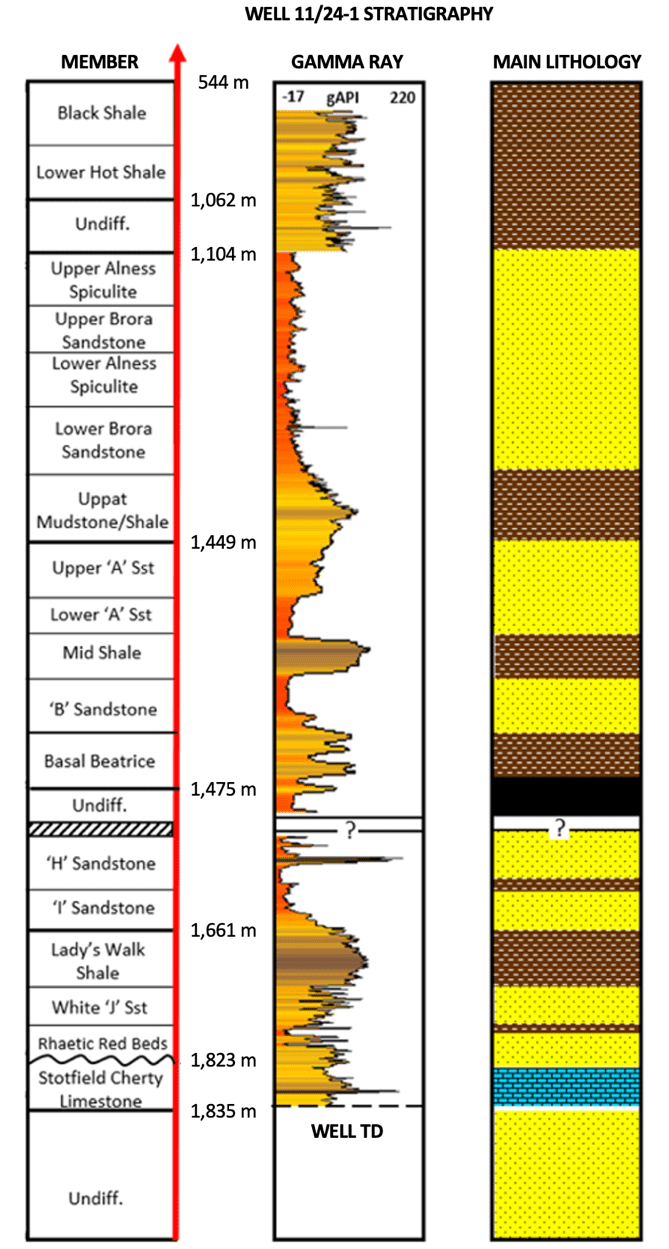

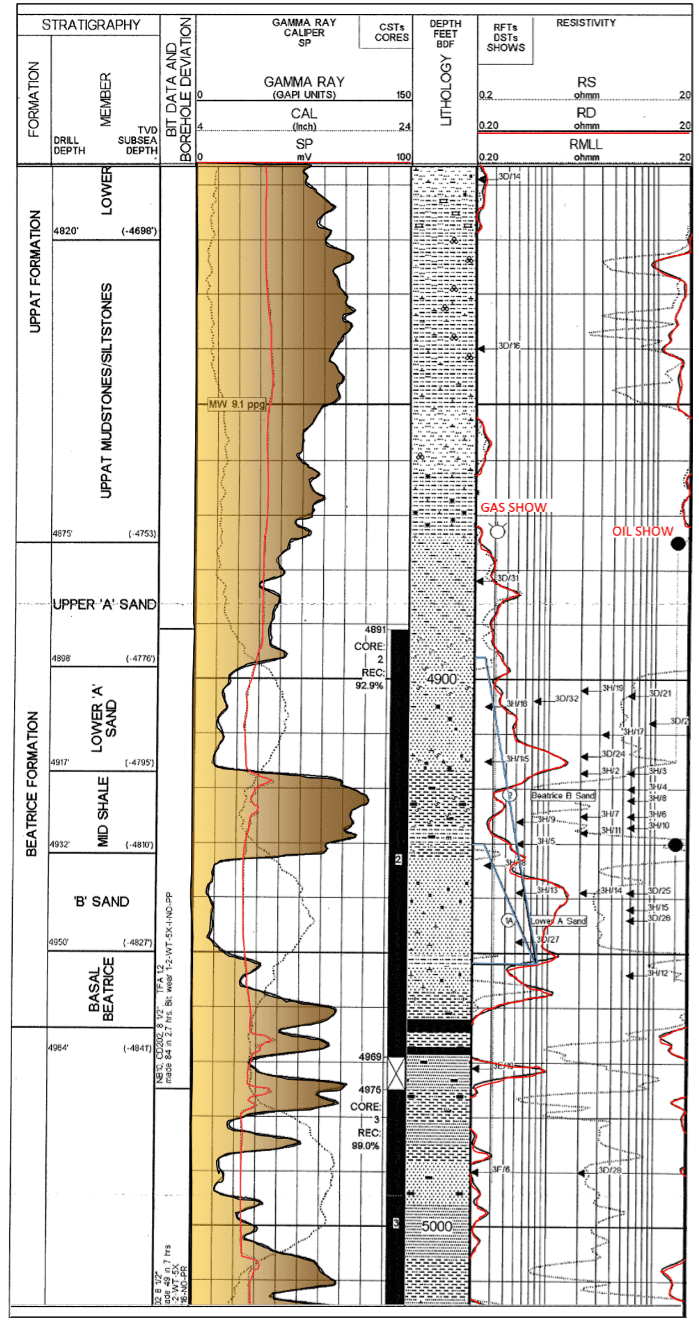

Lybster was drilled in 1996 just 3 km off the Caithness coast – Figure 4. Lybster is 3 km from the coast, with a vertical offshore discovery well, 11/24-1 (1996), onshore extended reach appraisal well, 11/24-3 (2008), 3D seismic coverage, and a reservoir model.

Figure 4. The Lybster prospect location, associated reservoir model, seismic section and well data.

The model (Figure 4, bottom right) is constructed from 3D seismic data (Figure 4, bottom left) and well data (Figure 4, top left). The field has two high quality reservoir units, the lower ‘A’ and ‘B’ sands, separated by a baffle, the mid-shale, and capped by the Uppat Shale seal. The field is divided into two halves by a fault that strikes NE-SW. Several small faults occur between the regional Great Glen Fault (GGF) and Helmsdale Fault (HF).

The discovery well for Lybster was plugged and abandoned. The field was then drilled from the shore in 2008 via a 3 km extended reach well; the only offshore UK field to be produced this way. Most North Sea fields are much further offshore. This makes Lybster an accessible and low-cost storage prospect that requires no expensive infrastructure. If suitable, the suspended production well could be repurposed for CO2 injection.

Lybster is a four-way closure, or small 6 km2 dome, that has trapped oil and gas beneath a mudstone caprock for tens of millions of years. This is a good indication of suitability for storing CO2. The structural volume or space available for storage is calculated from known properties of the field such as reservoir area, thickness, porosity, and fluid properties such as CO2 density at reservoir conditions. The expected capacity is 2 Mt, (low-high range: 0.3-9 Mt).

An appraisal licence requires an early risk assessment (ERA) to formally establish the expected capacity and technical suitability of a suite of attributes ranging from seal and reservoir quality to fault geomechanics, lateral migration risk, legacy wells, and more. The ERA is a gap analysis that identifies further data requirements and potential issues to address in the ‘Assess and Define’ phases of an appraisal term for a storage licence. A first-look analysis follows below.

Storage analysis

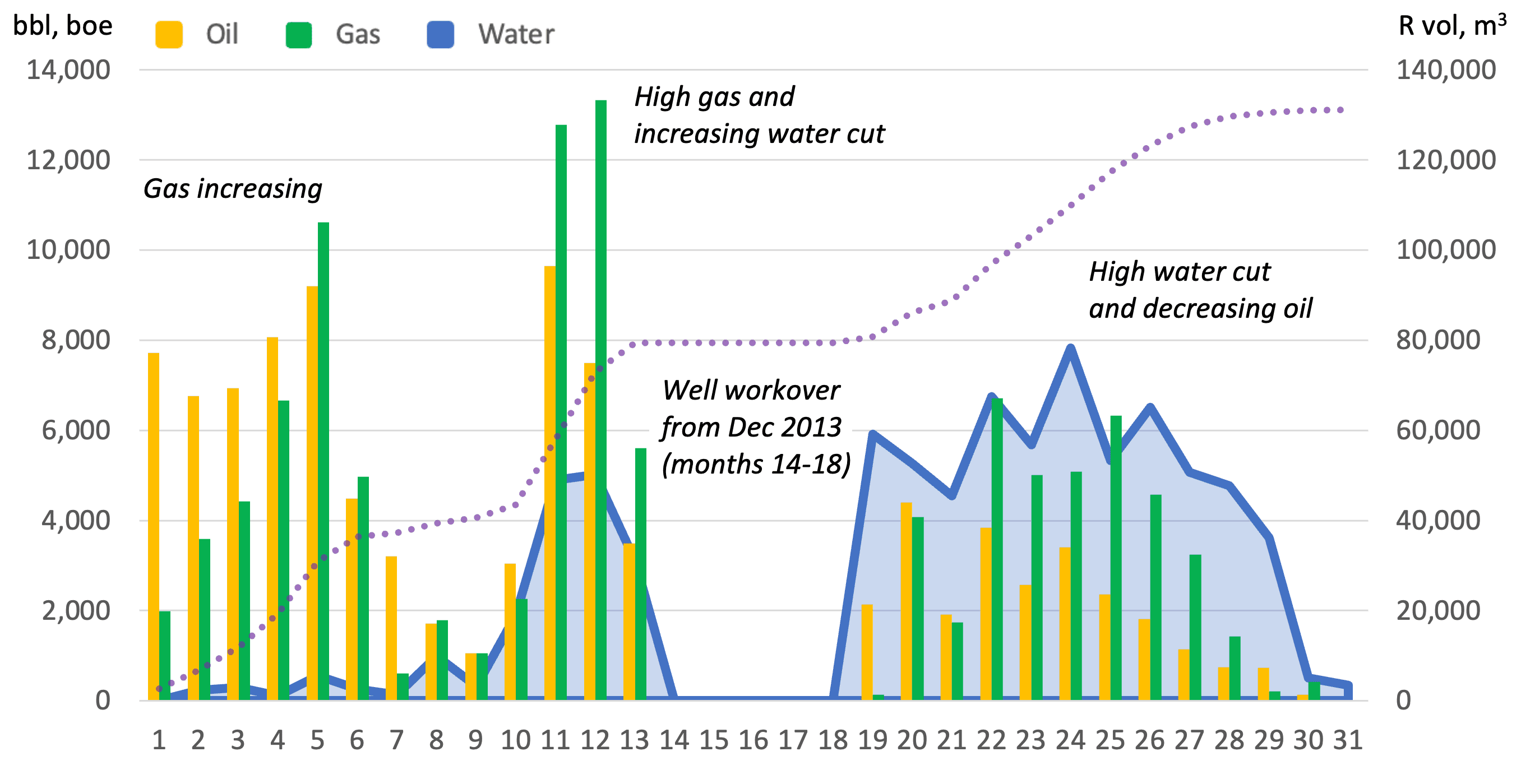

At least two attributes of the Lybster field require further analysis as part of an early risk assessment. Firstly, the production history deviated from expectations – Figure 5. Increasing gas and water cuts within a matter of months and declining oil production resulted in a well workover and then suspension. A dynamic reservoir model is needed to explain these outcomes and fully understand the flow and containment of fluids within the structure.

Figure 5. Production history in barrels of oil, water, equivalent gas, and produced reservoir volume.

Secondly, the field is located between two large faults, the Helmsdale Fault and Great Glen Fault, and has several smaller faults within the field boundary that segment the reservoir. These require a detailed geomechanical study to de-risk the prospect – Appendix F.

Capacity: The expected capacity of Lybster, based on the structural volume, is 2.1 Mt of CO2. – Table 4. This reasonable mid-range value assumes just half the field area, 3 km2, and an average reservoir thickness of 15 meters. A storage area of 3 km2 assumes the main fault for the field is sealing and CO2 storage is restricted to half the mapped field area. The full field area, 6.11 km2 (NSTA estimate), effectively doubles the capacity for mid-range values.

Combining the full-field area with high-range values for the other five variables quadruples the capacity. The full field area and high-range values for all variables furnishes an optimistic maximum capacity of 9.4 Mt. The low estimate, a pessimistic 0.35 Mt, uses low range values and halves the expected area again. The highly conservative minimum estimate of 100 kt is based on the produced volumes of oil, gas, and water.

Qualifying adjectives for capacity are as follows: ‘minimum’ is the lowest value calculated, a highly conservative production volume estimate. The structural volume estimates are defined as ‘low, ‘mid’, and ‘high’, based on reasonable range estimates for six variables; the dominant variable is the storage area. Note that while the outcomes resemble the common P90-P50-P10 approach, the data is too sparse to support a statistical analysis. This simply reflects the field’s short production history. The two methods are summarised in Appendix H.

Table 4. Structural volume variable range and applied values for capacity estimates

|

Variable |

Range |

Low, 0.35 Mt |

Mid, 2.1 Mt |

High, 9.4 Mt |

|---|---|---|---|---|

|

Storage area |

1.5 – 6 km2 |

1.5 |

3 |

6 |

|

Net thickness |

5 – 25 m |

9 |

15 |

21 |

|

Porosity |

8 – 22% |

0.11 |

0.15 |

0.19 |

|

Net to Gross |

56-80% |

0.6 |

0.68 |

0.76 |

|

CO2 Density |

700-750 kg/m3 |

710 |

725 |

740 |

|

Saturation |

50 – 75% |

0.55 |

0.625 |

0.70 |

Discussion

The Lybster field area has been intensively studied – Appendix H. While this report relies on Keenan’s detailed analysis of reservoir attributes such as porosity (Keenan, 2023), it corrects for the field area which was underestimated by an order of magnitude. The 2 Mt outcome is reasonable when compared to traps with a similar area such as Sleipner, Norway.

The alternative analysis, presented by Watt (Watt et al., in preparation), assumes a replacement volume for produced fluids. While this is a common approach to the capacity assessment of mature depleted fields such as Viking and Hamilton (Track-1 and Track-2 storage sites), the outcome is highly conservative for Lybster, a field with an unusually short production history. We favour the structural volume as a more reasonable indication.

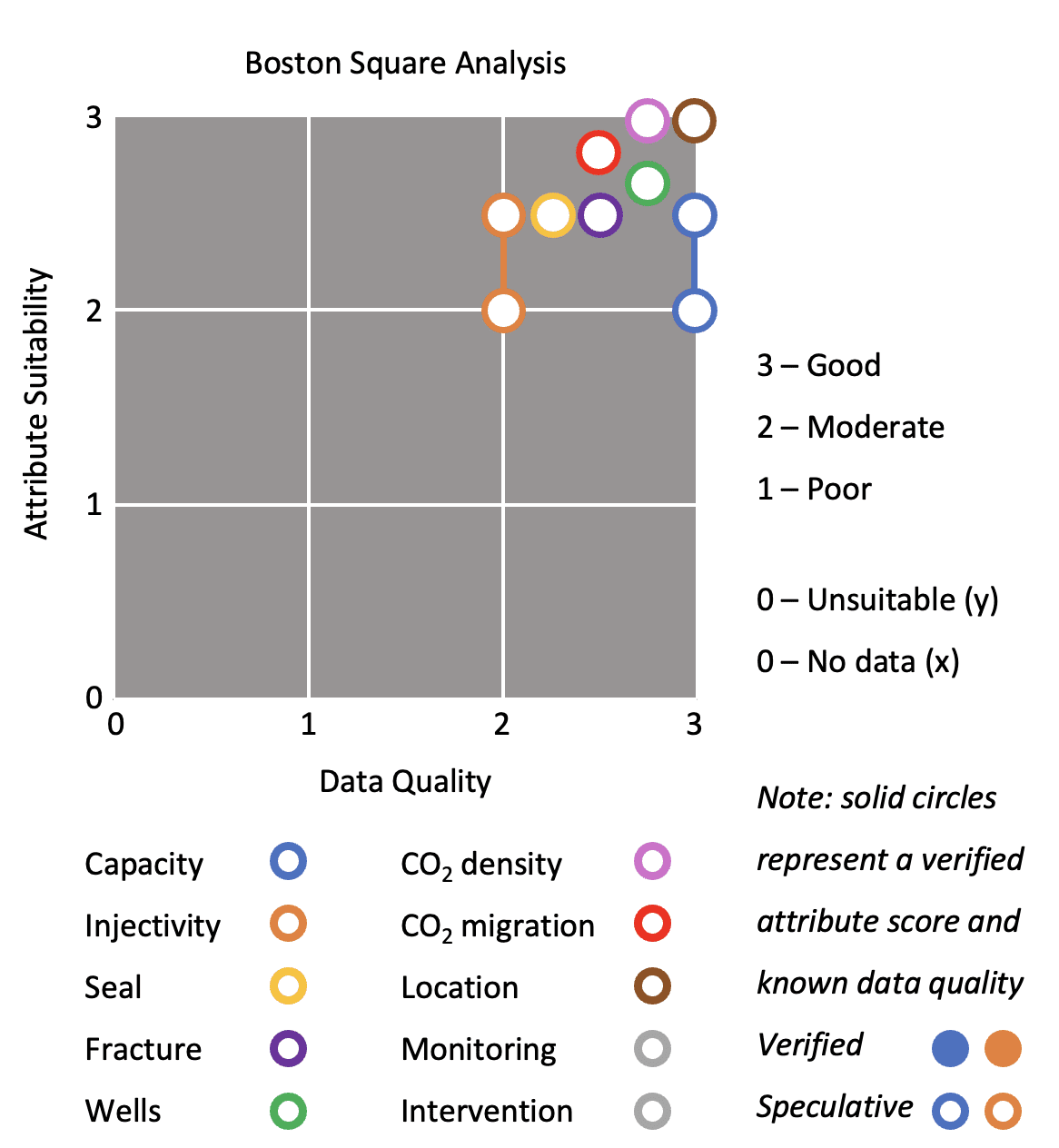

The suite of suitability attributes also supports Lybster as a strong candidate for a licenced storage appraisal – Figure 6. This will apply the rigour necessary to mature the attribute scores from speculative to verified or identify gaps for further analysis. Our recommendation is that an appraisal licence include studies on fault integrity, geomechanics, and reservoir simulation.

Figure 6. Boston Square analysis of attribute suitability for Lybster. A Boston Square is a simple scheme for scoring expert judgement from 1 to 3 devised by the Boston Consulting Group.

Forth Basin

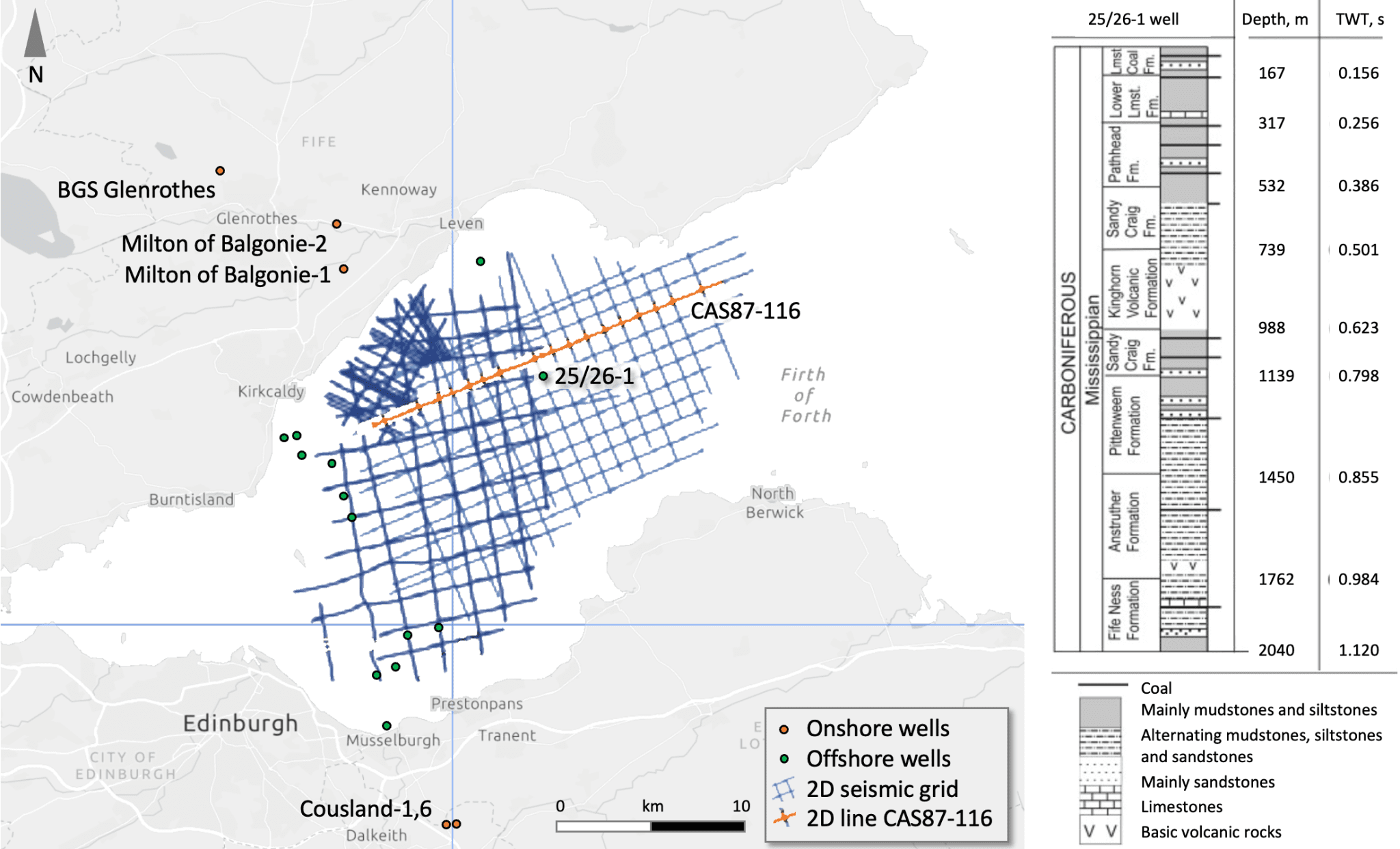

The Forth Basin contains the Leven syncline, a geological structure in the Forth Estuary mapped on 2D seismic – Figures 7 and 8. Most proposals for CO2 storage assume injection of liquid CO2. This requires a geological seal above the reservoir to trap its buoyant rise. However, it is also possible to inject dissolved CO2 with large volumes of water, where the CO2-saturated water is denser than the porewater and sinks rather than rises. Research at the BGS and the University of Edinburgh shows that suitable geology to retain sinking dense CO2 may exist beneath the inshore waters of the Forth Estuary (Smith et al, 2011).

CO2-brine surface mixing

The CO2-brine dissolution approach was extensively modelled by Eke et al. (2011) and became a commercial reality in 2014 with the industrial-scale injection of 7 ktpa of CO2 from the Hellisheiði power plant, Iceland. While the physical limit for CO2 dissolution is 50 kg/m3, optimal chemical and physical parameters are controlled in the surface process facility. For Iceland, the outcome is 20 kg of dissolved CO2 per cubic meter of injected brine. This increases the volume of injected fluid by about 35x compared to a pure CO2 injection project like Sleipner. Reservoir pressure increases are minimised by extracting brine from the reservoir for mixing and return. This has worked for Iceland, with injection recently increasing from 7 ktpa to 12 ktpa. Future plans will scale to 40 ktpa before 2030. However, the geological setting, densely fractured young volcanic rocks, is quite different from the Leven Syncline.

Figure 7. Forth Basin, location of 2D seismic data grid, interpreted line and exploration well 25/26-1.

Figure 8. 2D seismic line CAS87-116, revealing the stratigraphy and structure of the Leven Syncline.

Suitability

The high volumes of brine injection associated with dissolved CO2 storage require a simple combination of a large regional aquifer with good reservoir quality and low structural complexity. The aquifer needs to provide a sufficient volume to help minimise pressure increases. Reservoir quality also minimises pressure increases. This implies above average porosity and permeability and thick continuous beds of high net-to-gross sandstones. Low structural complexity implies a simple geometry with a small number of faults that are transmissive, i.e. open to the lateral flow of brine, allowing the dissipation of injected fluids. These attributes are not clearly established for the Leven syncline – Figure 9.

A detailed analysis of the area (Monaghan et al. 2012) noted the poor data quality, lack of reservoir data, and structural complexity. These attributes are reflected in the low TRL status of the Forth Basin prospect.

Figure 9. Forth Basin area regional geology, indicating the stratigraphic and structural complexity.

Sources of bio-CO2

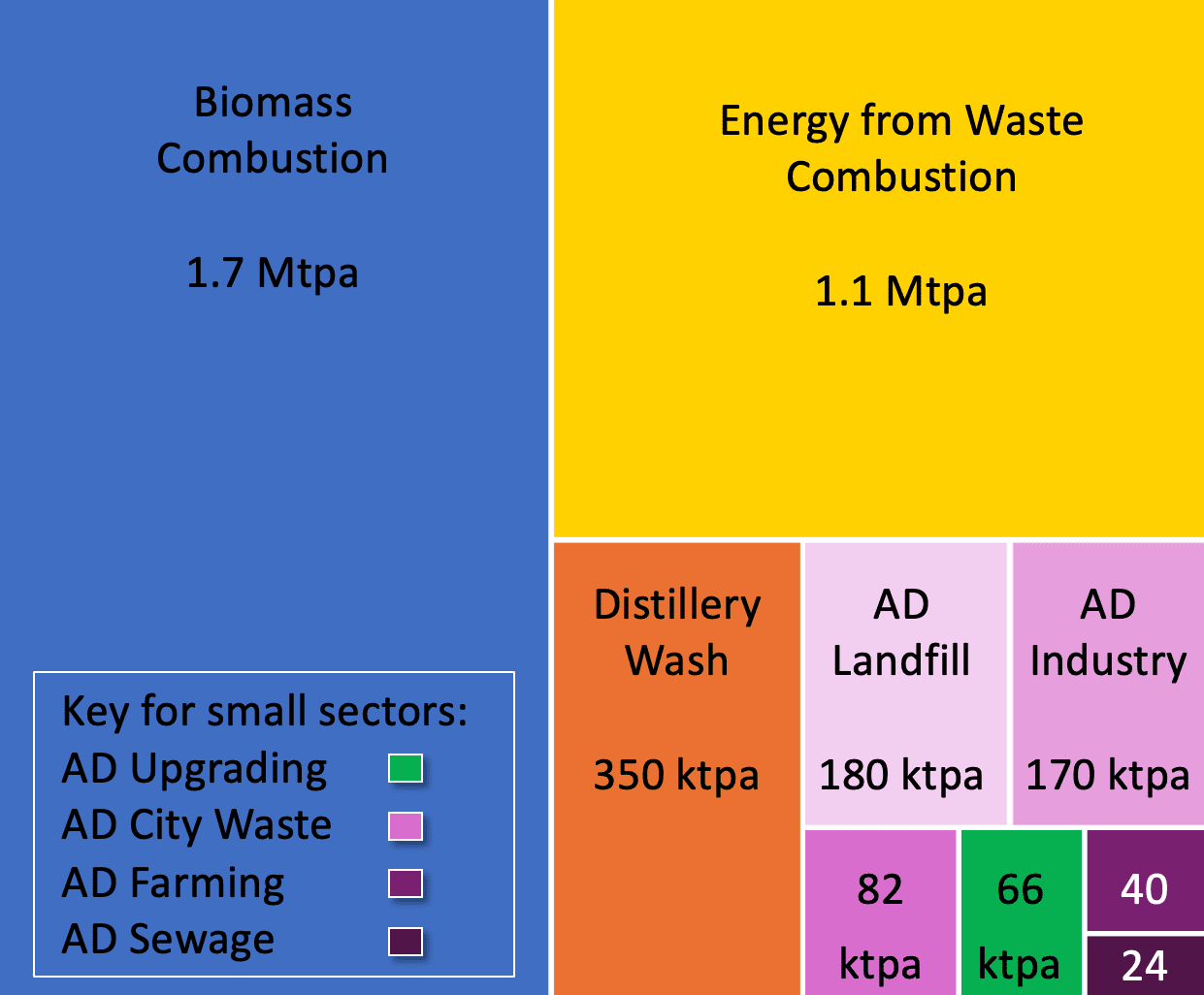

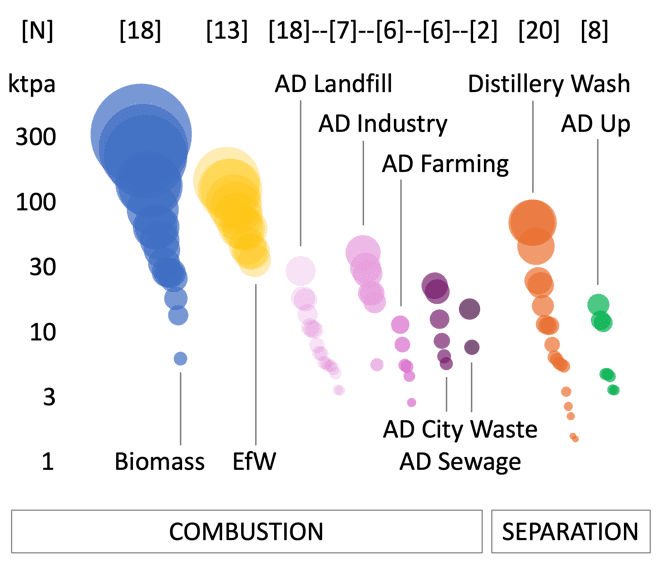

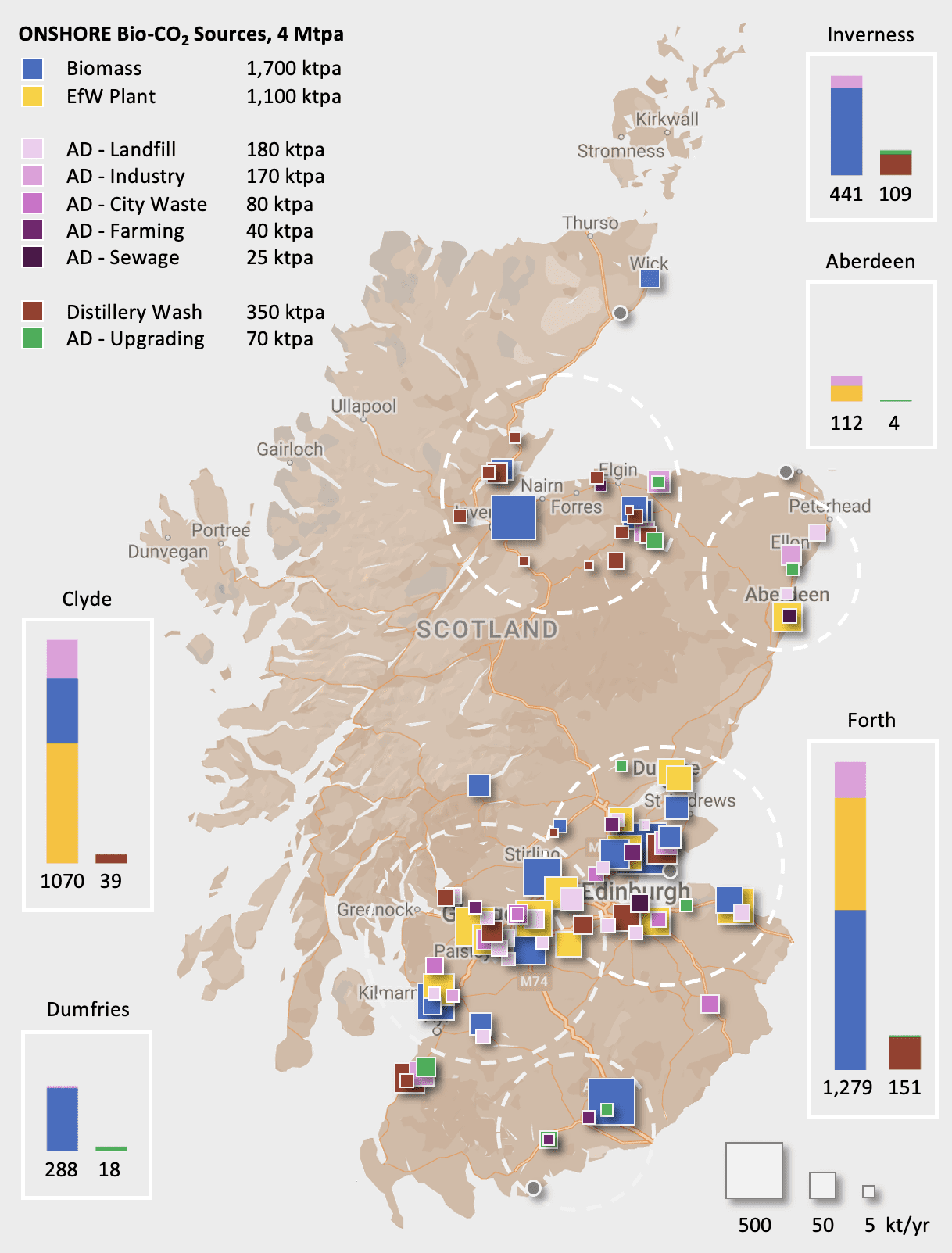

Our analysis of over a hundred sources of bio-CO2 in Scotland produced a database of 98 sites with emissions that range from 3 to 360 ktpa – Figure 10. Four small distilleries, 1.6-2.8 ktpa, are included as these have already been selected for bio-CO2 capture. The total resource is 3.7 Mtpa. Almost all the sources, 91 sites, are grouped into five regional clusters – Figure 11.

Categories and Sectors

We have categorised the sources based on capture method: combustion, 89%, and separation, 11%. Separation at distilleries and anaerobic digesters is low-cost and high purity relative to post-combustion flue gas capture. The two categories are then split by process into nine sectors.

Biomass

Biomass, the largest sector at 46%, produces CO2 from the combustion of plant and animal waste. Biomass is often configured as combined heat and power (CHP). The 18 facilities in the database produce an average of 95 ktpa and total 1.7 Mtpa. The six largest sites, 150-360 ktpa, include Markinch, Steven’s Croft, and Morayhill. This accounts for 900 ktpa of bio-CO2 emissions. The smallest site, Gleneagles, emits 7 ktpa. Locations tend to be semi-rural.

Energy from Waste

Energy from Waste (EfW), the second largest sector, 29%, produces electricity and heat from the incineration of municipal waste, often in a CHP configuration. Roughly half of the emissions are bio-CO2 (Tolvik, 2024). The 13 sites emit a total of 1.1 Mtpa, average 84 ktpa. The five largest are amongst the top ten sources, total 0.6 Mtpa, average 126 ktpa. The largest, South Clyde Energy Centre, 158 ktpa, is planned for 2025. The smallest site, Binn, 38 ktpa, opens in 2026.

Anaerobic Digestion

Anaerobic digestion (AD) covers a range of dry and wet waste applications that produce raw biogas. AD tends to be small, with 39 sites in the database accounting for 0.5 Mtpa of bio-CO2, average 13 ktpa. The largest site, 44 ktpa, is the Girvan distillery. The smallest site, Crofthead farm, 3 ktpa. We identify five sectors where biogas is combusted on site:

- AD Landfill is the fourth largest sector overall after biomass, EfW, and distillery fermentation, with 18 facilities producing a total of 0.18 Mtpa, average 10 ktpa.

- AD Industrial is the second largest AD sector with 7 facilities producing 0.17 Mtpa, average 25 ktpa. Sites include distilleries, breweries, and pharma manufacturing.

- AD City Waste is the third largest AD sector with 6 facilities producing 0.08 Mtpa in total, average 14 ktpa. Sites process municipal wet streams such as food waste.

- AD Farming is the fifth largest AD sector with 6 facilities producing 0.04 Mtpa in total, average 7 ktpa. Sites process wet streams such as crop waste and silage.

- AD Sewage is the smallest bio-CO2 sector, with just 2 facilities in the database producing 0.02 Mtpa in total: Seafield, 16 ktpa, and Nigg, 8 ktpa.

Distillery Fermentation

Whisky distilleries produce CO2 during the mash fermentation stage. The CO2 can be easily separated using a simple wash process where pressurised water acts as a solvent. This generates a pure CO2 stream. Distillery fermentation (DF), 10%, is the third largest sector after biomass and EfW, with 20 sites producing 0.35 Mtpa in total, average 18 ktpa.

The three largest distilleries account for 0.2 Mtpa, average 66 ktpa; the remaining 17 sites account for 0.16 Mtpa, average 9 ktpa. The database includes four small distilleries: Tomatin, Speyburn, Tullibardine, and Balmenach, 1.6-2.8 ktpa. These are shortlisted along with Invergordon and North British for commercial bio-CO2 capture and storage (CCSL, 2024). Many of the 20 sites are located around Speyside as part of the Inverness cluster.

AD upgrading

AD biogas can be upgraded to biomethane by separating out the CO2 using a membrane filter. The biomethane is frequently sold directly into the natural gas grid. As with distilleries, this also generates a low-cost and high-purity stream of bio-CO2. AD upgrading is the seventh largest sector overall, 2%, with eight sites producing 0.07 Mtpa in total, average 8 ktpa. Sites include farms and industrial facilities located in semi-rural areas across the country.

Table 5. Bio-CO2 sources by sector. Note: the lowest cost sectors are highlighted in grey.

|

Sector, Bio-CO2 |

Category |

Sites |

Average |

Range, ktpa |

Total |

3.7 Mtpa |

|---|---|---|---|---|---|---|

|

Biomass |

Combustion |

18 |

95 ktpa |

7-360 |

1.70 Mtpa |

45.8% |

|

Energy from Waste |

Combustion |

13 |

84 ktpa |

38-158 |

1.10 Mtpa |

29.4% |

|

Distillery Wash |

Separation |

20 |

18 ktpa |

2-75 |

0.35 Mtpa |

9.52% |

|

AD Landfill |

Combustion |

18 |

10 ktpa |

4-32 |

0.18 Mtpa |

4.93% |

|

AD Industrial |

Combustion |

7 |

25 ktpa |

6-44 |

0.17 Mtpa |

4.67% |

|

AD City Waste |

Combustion |

6 |

14 ktpa |

6-24 |

0.08 Mtpa |

2.20% |

|

AD Upgrading |

Separation |

8 |

8 ktpa |

4-17 |

0.07 Mtpa |

1.76% |

|

AD Farming |

Combustion |

6 |

7 ktpa |

3-12 |

0.04 Mtpa |

1.08% |

|

AD Sewage |

Combustion |

2 |

12 ktpa |

8-16 |

0.02 Mtpa |

0.65% |

Figure 10. Bio-CO2 sectors. Distillery (orange) and AD Upgrading (green) are categorised as separation, yielding a low-cost CO2 source relative to post-combustion capture. Values in square brackets [18] represent the number of sources; area of circles represent the size of the source (ktpa).

Figure 11. Onshore sources of bio-CO2 across Scotland. 91 of the 98 sites are located in five clusters.

Many low-cost distillery sources are located in the Inverness cluster, relatively close to the Lybster site. The five clusters are analysed by road distance from the nearest storage prospect in section 3.2. Also, note the overlap of the Forth and Clyde clusters at the terminus of the Feeder 10 pipeline. This highlights an interesting possible alternative to inshore storage, i.e. access to the Acorn offshore storage hub. This is discussed further in the summary.

Regional Clusters

We have grouped the sources into five clusters. The boundaries are marked by either a 100 km or 50 km diameter circle. Note, the sources east of Elgin are closer to Fraserburgh but included as part of the Inverness cluster given the primacy of Lybster as a storage candidate.

Inverness

The Inverness cluster, the third largest overall, falls within the Lybster catchment area. The cluster has 21 sites, producing 0.55 Mt of bio-CO2, and boasts a concentration of low-cost separation sources: 12 distilleries, 92 ktpa, and two AD upgraders, 18 ktpa. The average road distance to storage is high at 186 km. However, just over half of the cluster, 0.31 Mtpa, is within 150 km of Lybster: 5 distilleries, 43 ktpa, including the region’s largest distillery, Invergordon, 24 ktpa, which has been shortlisted for commercial CO2 capture; and 2 biomass plants: Morayhill, 323 ktpa, and Balcas, 28 ktpa, which is close to the Invergordon distillery. The remaining low-cost sources, 67 ktpa, are 200 to 240 km from Lybster by road.

Aberdeen

The Aberdeen cluster sits within the Fraserburgh catchment area, with six facilities producing 116 ktpa. The majority comes from five combustion facilities; the remainder from a small AD upgrading facility: Savock Farm, 4 ktpa. The largest source is the NESS EfW plant at 67 ktpa. The cluster has the third shortest average road distance to storage at 56 km.

Dumfries

The Dumfries cluster has five facilities producing 300 ktpa, mostly from the Steven’s Croft biomass plant, 0.28 Mtpa. The area includes two low-cost AD upgrading facilities producing a combined 18 ktpa. One of these, Crofthead, is already commercially capturing 13 ktpa, and has a separate CHP source, 3 ktpa, currently not captured. All the sites are within 70 km by road of the Solway Firth storage prospect. The cluster average at 48 km is the shortest overall.

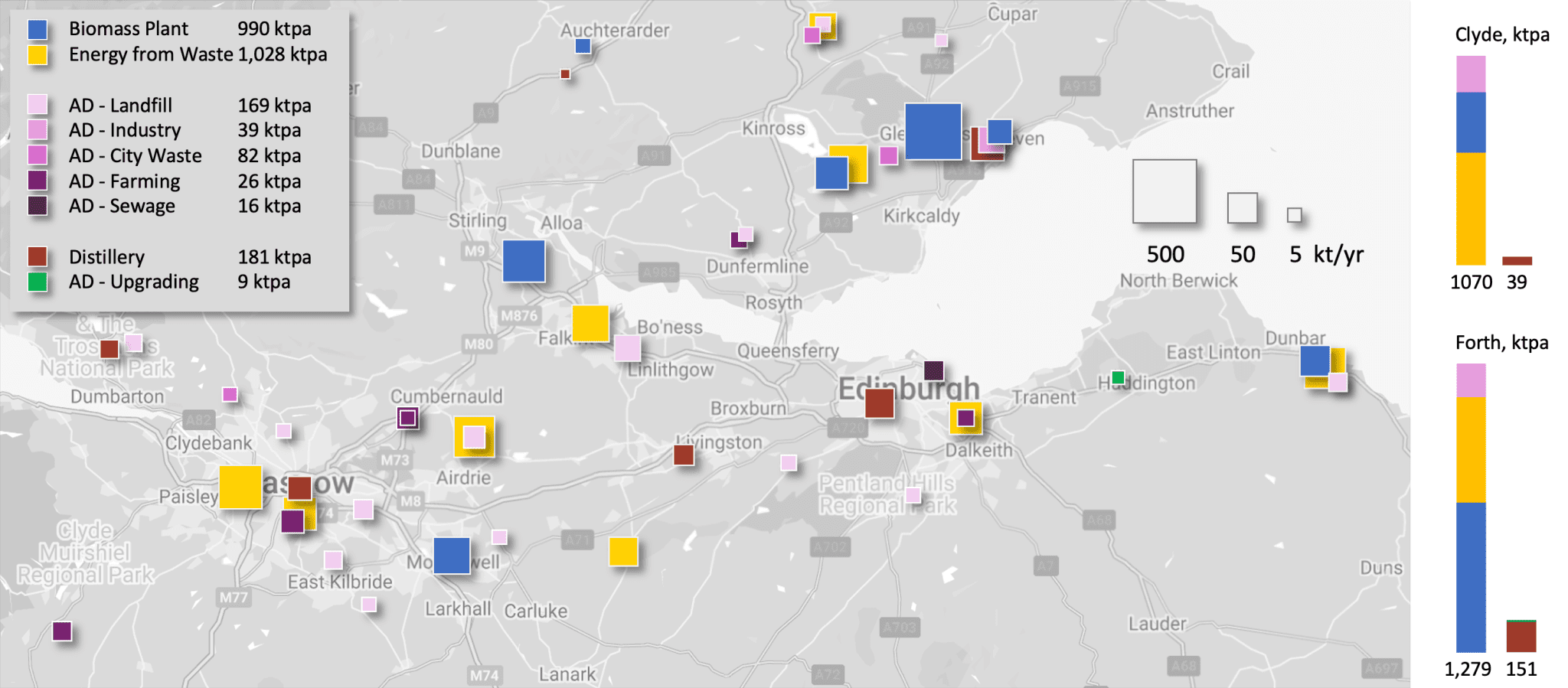

Forth & Clyde

The Forth and Clyde clusters are closest to the Forth Basin storage prospect. These are the two largest clusters in our database, with a combined 59 sites producing 2.5 Mtpa. The area accounts for 69% of all combustion and 45% of all separation sources in the database; and includes some of the largest facilities including the Markinch and Caledonian biomass plants, 360 and 144 ktpa, and Cameronbridge distillery, 75 ktpa. Just over 0.84 Mtpa is within 50 km of the Forth Basin storage location, including Cameronbridge, 9 km, and Markinch, 10 km.

The North British distillery, 49 ktpa and 49 km by road from the storage location, is already commercially capturing CO2 for export to storage in Denmark. Low-cost separation sources account for 190 ktpa of bio-CO2 at an average road distance of 80 km from the storage location. It is worth noting the Feeder 10 terminus is located in the overlap of the two cluster boundary circles. Also of interest, are the significant local combustion clusters at Irvine, 290 ktpa, and Dunbar, 208 ktpa, which are 107 km and 109 km by road from the storage location.

Outliers

Seven outliers account for just 3% of all combustion, and 24% of all separation sources. The latter value reflects a concentration of low-costs sources in Ayrshire. This includes two facilities at the Girvan distillery: fermentation, 75 ktpa, and AD upgrading, 17 ktpa; and the neighbouring Ailsa Bay distillery, 7 ktpa. Combustion sources include Charlesfield AD, Borders, 18 ktpa, the Acharn biomass plant, Perthshire, 31 ktpa, and the Pulteney distillery, Wick, a small biomass plant, 19 ktpa. The latter is the closest source to Lybster.

Table 6. Bio-CO2 sources by cluster. Note: the sources outside clusters are highlighted in grey

|

Combustion |

Bio-CO2 |

Storage |

N |

Average |

Road |

Range, ktpa |

3.3 Mtpa |

|---|---|---|---|---|---|---|---|

|

Inverness |

441 ktpa |

Lybster |

7 |

63 ktpa |

197 km |

5-242 |

13% |

|

Aberdeen |

112 ktpa |

Fraserburgh |

5 |

22 ktpa |

57 km |

4-67 |

3% |

|

Forth |

1,362 ktpa |

Forth Basin |

25 |

51 ktpa |

46 km |

4-360 |

41% |

|

Clyde |

987 ktpa |

Forth Basin |

26 |

41 ktpa |

99 km |

5-158 |

32% |

|

Dumfries |

288 ktpa |

Solway Firth |

3 |

96 ktpa |

50 km |

3-279 |

9% |

|

Outliers |

112 ktpa |

Various |

4 |

28 ktpa |

86 km |

18-44 |

3% |

|

Separation |

Bio-CO2 |

Storage |

N |

Average |

Road |

Range, ktpa |

0.4 Mtpa |

|

Inverness |

109 ktpa |

Lybster |

14 |

8 ktpa |

181 km |

2-24 |

26 % |

|

Aberdeen |

4 ktpa |

Fraserburgh |

1 |

4 ktpa |

49 km |

4 |

1% |

|

Forth |

151 ktpa |

Forth Basin |

6 |

25 ktpa |

68 km |

2-75 |

36% |

|

Clyde |

39 ktpa |

Forth Basin |

2 |

19 ktpa |

114 km |

12-27 |

9% |

|

Dumfries |

18 ktpa |

Solway Firth |

2 |

9 ktpa |

46 km |

5-13 |

4% |

|

Outliers |

99 ktpa |

Various |

3 |

33 ktpa |

84 km |

7-75 |

24% |

Development timeframes

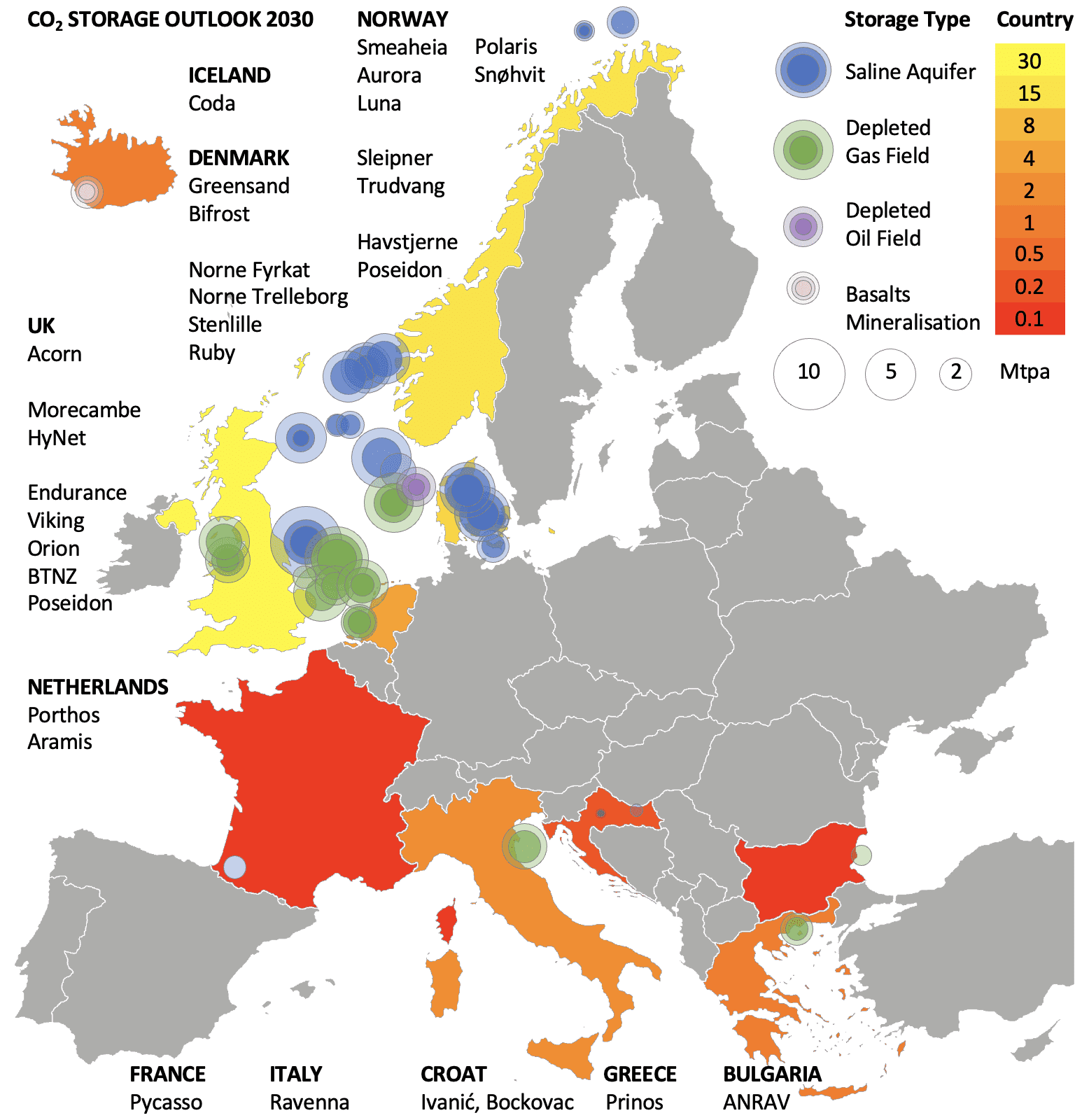

CCS is being rapidly deployed to meet demanding net zero targets. By our analysis, there are 32 projects across Europe with realistic timelines to storage by 2030 – Figure 12. Development timeframes have become crucial to delivering these targets, as policy makers seek to balance haste with due diligence. The exponential growth in demand for CDR credits is also exacerbating a supply imbalance for CO2 storage that early movers, notably Denmark (Stenlille), Iceland (Coda), and Norway (Northern Lights) are seeking to capitalise on. We observe that timeframes in these countries are the fastest in Europe at around five years.

Figure 12. The outlook for European Storage, 2030. Seven countries have megatonne projects planned, with 64% of capacity in the North Sea. Countries in grey have no storage planned for 2030.

UK timelines

The NSTA, as the UK’s competent authority and carbon storage regulator, is instrumental in setting UK licensing timelines. The first UK carbon storage licensing round was held in 2022. The NSTA announced 21 accepted appraisal licences in September 2023, building on the experience of the previous seven licences. Each licence is tailored to the prospective storage site with a deadline for a storage permit application and specific requirements relating to the necessary maturation of the project for a permit application – Appendix D.

The first storage permits are expected no later than Q4 2024 for Endurance CS001 (East Coast Cluster) and Hamilton CS004 (HyNet North West). Assuming a two-year construction and commissioning period, first injection is expected no later than 2028 with minor delays possibly increasing that to 2030. It is worth noting that 21 of the appraisals are required to submit storage permit applications between 2026 and 2028, which may cause a significant bottleneck similar to Class VI well permitting delays at the Federal level in the USA – Appendix I.

Analysis of the 27 active licences indicates that the average appraisal time from early risk assessment to storage permit application is five years and three months. Examples of exceptionally short and long appraisals are the Scottish Cluster’s Acorn East licence (Storegga, two years) and the East Coast Cluster’s Bunter 42 expansion (BP, eight years). The former is supported by a decade of prior site characterisation. The latter is an exploration target that requires 3D seismic acquisition and an appraisal well. Allowing for construction and commissioning, storage projects expect to be operational, i.e. ‘on injection’, within eight years on average of an appraisal licence application.

EEA timeframes

Analysis for EEA projects is largely dependent on public statements of ambition. The outcomes are faster than the UK. The nine Norwegian projects average six years from initial application to expected operation. Denmark is relatively fast by comparison, averaging four years for its six projects. The two large Dutch projects, Porthos (2019) and Aramis (2021), expect to be operational within seven years. Pycasso, the French project launched in 2021, has the longest development period at ten years. The remaining projects for Bulgaria, Greece, Iceland, and Italy expect to be operational within five years of their start dates which range from 2021 to 2023. If the UK timings are indicative, ambitious EEA deadlines of less than six years for a third of the projects are likely optimistic and at risk of delays of one to five years. This may result a storage capacity substantially less than the EU target of 50 Mtpa.

Implications for inshore storage

Many storage projects are on timelines of around a decade characterised by three phases: a pre-licensing identification and application phase of approximately three years; an appraisal licensing phase that averages five years; a storage permit construction and commissioning phase of around two years. This is likely to hold true for Fraserburgh and the Solway Firth, the two less mature areas of interest identified in Chapter 2. Lybster is an exception, with several factors indicating a fast-track approach that could support a storage permit application within three years. This option is examined in the final chapter of this report.

Cost-revenue analysis

The following cost-revenue analysis for the capture, transport, and storage of bio-CO2 establishes to a good first approximation the potential value of developing onshore and inshore CCS in Scotland. The full chain cost is compared to available revenue from the recent emergence of a high-demand and low-supply voluntary CDR market.

Note that indicative costs for capture, transport, and storage are based on publicly available sources where possible. In the absence of published data, companies operating in Scotland, the UK, and Europe have been approached to provide a commercial estimate.

Capture

Capture is divided into two categories: combustion and separation. Combustion accounts for seven of the studied nine sectors and 89% of the bio-CO2, 3.3 Mtpa. This category costs more than separation as the capture is a post-combustion process on a low-purity and dilute flue gas stream, whereas separation from distilleries and biomethane upgraders is on a high-purity and concentrated CO2 stream that simply requires dehydration and compression.

The combustion sources in this study range from eight large biomass and EfW facilities, 130-360 ktpa, to twenty-five small AD sites, 3-12 ktpa. Post-combustion capture is sensitive to economies of scale, with many studies noting a wide range of capture costs that reflect the stream purity and size of the facility. For example, there is an average 43% increase in cost for an order of magnitude decrease in capture rate from megatonne to sub-megatonne projects (GCCSI, 2021).

The available literature focuses on large CCS applications, broadly defined as facilities emitting at least 100 ktpa (IEAGHG, 2024). A degree of generalisation is therefore necessary given that 89 of the 98 sources in this study emit less than 100 ktpa, with half the sources emitting less than 15 ktpa.

Where possible, we estimate a range for costs and assume the high cost given the predominance of small sources in our data.

Biomass is the largest sector in this study with sources averaging 95 ktpa. We estimate a low cost of £87 per tonne based on the levelised cost analysis of Lehtveer & Emanuelsson (2021) – Appendix J. We estimate a high cost of £128 per tonne based on analysis of emitters smaller than 100 ktpa by Beiron et al. (2022). We favour the high cost as representative – Table 5.

Energy from Waste is the second largest sector with average emissions of 84 ktpa. Two estimates were found with broadly similar costs: £81 and £109 per tonne (MVV, 2024; IEAGHG, 2024). We favour a high cost as the average plant capacity is small at under 200 ktpa of waste.

Anaerobic Digestion covers five sectors in the combustion category with low average emissions of 13 ktpa. We found no data on capture costs for AD combustion. We assume a low-cost of £128 per tonne from the biomass analysis, given the much smaller size of AD sources. In the absence of data, we conservatively assume a high cost of £136 per tonne based on a mean EfW cost, £95, multiplied by the order-of-magnitude scalar for combustion, 143%.

Separation produces highly concentrated streams of pure bio-CO2 (EBA, 2022). Distillery fermentation, average 18 ktpa, and AD upgrading, 8 ktpa, are the two sectors that use cryogenic distillation and membrane separation to capture the CO2. Global analyses provide a low-cost estimate of £30 (IEA 2021; NETL, 2023). In our opinion this reflects economies of scale for large bioethanol plants in the USA. A high-cost price of £60 per tonne is based on a commercial sales estimate for small emitters (E Nimmons, pers. comm., May 2024)[1].

Table 7. Estimated capture costs by sector, including % concentration of CO2 in emissions stream.

|

Sector, Bio-CO2 |

Category |

N |

Average |

Cost Range |

High Cost |

Stream |

|---|---|---|---|---|---|---|

|

Biomass Plant |

Combustion |

18 |

95 ktpa |

£87 – £128 |

£128 |

8-20% |

|

Energy from Waste |

Combustion |

13 |

84 ktpa |

£81 – £109 |

£109 |

6-12% |

|

AD Combustion |

Combustion |

39 |

13 ktpa |

£128 – £136 |

£136 |

10-20% |

|

Distillery |

Separation |

20 |

18 ktpa |

£30 – £60 |

£60 |

98% |

|

AD Upgrading |

Separation |

8 |

8 ktpa |

£30 – £60 |

£60 |

98% |

Transport

Truck transport is the simplest option, as rail transport of geographically dispersed sources would require onloading and offloading at rail heads with truck transport at both ends. A rail route north from Inverness, and clusters further south and east, terminates at Wick. No cost analysis of rail has been undertaken for this study.

Truck transport of CO2 is by a cryogenic T75 ISO tank as a liquid at -35°C and 22 bar. Each truck carries 20 tonnes. Assuming an injection rate of 100 ktpa and batch delivery over 6 days a week throughout the year, 16 truck loads per day are required. There is scarce literature on truck costs for Europe. However, a commercial estimate of £20 per tonne for a 100-mile round trip seems reasonable (E. Nimmons, pers. comm. May 2024) and is applied here – Appendix J. This is equivalent to £0.124 per tonne per km, which is similar to a recent cost estimate of £0.126 by Ricardo (2023) and $0.111 for the USA (Stolaroff et al., 2021). We presume that the slightly lower dollar estimate reflects lower fuel costs in America.

The average road distance to Lybster for the Inverness cluster is 191 km, with 87 ktpa available within 150 km. This includes 40 ktpa of low-cost CO2 from four distilleries; the remaining 47 ktpa are from two biomass sources, Balcas and Pulteney. The Inverness cluster has enough low-cost CO2 to supply 109 ktpa at an average road distance of 188 km, equivalent to £24/tonne.

With the exception of Savock Farm at Ellon, 4 ktpa and 300 km, the remaining low-cost sources are more than 360 km away. It follows that road transport costs for 100 ktpa over 10 years are £20-50 million with an opportunity to source all of the bio-CO2 from the Inverness cluster and low-cost sources at £24 million. It is worth mentioning that a hydrogen fleet would reduce life cycle emissions and road wear, being lighter than an electric vehicle equivalent (Low, 2024).

Storage

Three storage cost scenarios are considered. The most detailed is Lybster, outlined below. The second scenario is a first approximation for Fraserburgh and the Solway Firth. This is similar to Lybster but less mature and more challenging with respect to appraisal wells, seismic data, and location. The third scenario is a consideration of potential costs for the Forth Basin proposal, the least mature of the storage options.

Lybster

The cost analysis for Lybster assumes 100 ktpa of CO2 over a decade which would account for half of the expected capacity estimate of 2 million tonnes – section 2.2.1. This would potentially mature the understanding of the site towards a further decade of injection.

Buffer: The site will require tanks for the temporary storage of CO2 prior to injection. We assume four tanks with sufficient capacity for an injection rate of 100 ktpa, equivalent to an injection rate of 12 tonnes/hr. This allows for 10 days of well maintenance per year. While the production and injection of CO2 is continuous, transport occurs in discrete runs and is a batch process. Redundant capacity is required on-site to provide operational flexibility. Assuming 16 trucks a day and 125% capacity based on LNG shipping experience, 4 x 100 m3 onsite tanks would buffer flow to the wellhead. For comparison, the twelve Northern Lights tanks at Øygarden are 6 times the size to accommodate one shipload, 7,500 m3. The capital investment for the Lybster storage tanks and site works is assumed to be around £1 million.

Compression: The site will require a compressor to take the liquid CO2 to the required pipeline pressure of 150 bar for the well system and injection at reservoir conditions. We estimate this to require 120 kWh per tonne after Psarras et al. (2020) at an operational cost of £30 per tonne with no capital investment, assuming rental of the equipment from a service company. The operational cost over 10 years at 100 ktpa is estimated at £30 million.

Injection: The site also requires an injection well. The discovery well, 11/24-1, is unsuitable. The well is designated AB3 (NSTA, 2023), i.e. permanently abandoned and seabed cleared, with no infrastructure in place. Additionally, three cement barriers isolate the well. The re-purposing of 11/24-1 would be technically challenging and very expensive.

The production well, 11/24-3y, is currently suspended with the onshore surface infrastructure in place. The current drilling pad can be re-used and the well re-purposed. 11/24-3y is an extended reach well that has been designed to encounter a 173 m succession of the target reservoir sandstones compared to the 25 m of the vertical exploration well, 11/24-1. This favours good injectivity. It is estimated that the conversion cost of an onshore well to CO2 injection is approximately £1-2 million (IEAGHG, 2022). This is an order of magnitude cheaper than an offshore injection well at £10-15 million based on NSTA estimates of recent North Sea drilling costs at £5-10 thousand per meter (NSTA, 2023). We conservatively assume a combined conversion and maintenance cost for the well of £3 million.

Appraisal: The storage site requires an expert reinterpretation of the existing 3D seismic cube, including depth conversion and static model construction (three months) and dynamic simulation of the reservoir (nine months). This would match the known fluid production history and forward model the reservoir response to CO2 injection and storage (9 months). We estimate the cost of this appraisal study to be about £0.5 million. A related geomechanical study of similar duration and rigour is also estimated to cost £0.5 million. The budget for a two-year appraisal that includes both the modelling and geomechanical studies, a well repurposing study, and standard elements of the NSTA appraise-assess-define framework for appraisal licensing is estimated to cost approximately £3 million.

The cost estimates sum to a sub-total is £37 million. Assuming operational costs for the site of £250,000 per annum, the capital investment and operational costs sum to £40 million. Not addressed here are monitoring and verification, as these are highly dependent on the technologies chosen. The design of the monitoring programme is an important element of the appraisal licence. However, if we conservatively assume a monitoring cost of £20 million over the lifetime of storage and add £10 million for conformance and decommissioning, this indicates a storage cost of £70/tonne based on 100 ktpa over 10 years.

Fraserburgh and Solway Firth

These two prospective sites require an offshore installation and operation. Assuming suitable targets are discovered at 1,000-2,000 m depth, the well drilling cost would be £10-15 million. A compressor would need to be either located offshore on a small operational platform, or at the landfall end of a 16 km pipeline. While there is scant literature on short pipeline costs, we conservatively assume a cost of £50 per tonne based on the analysis of Johnsson et al. (2017). The 10 year 100 ktpa cost is £50 million. The cost of an offshore operational platform is tentatively estimated at £10 million. Note that no cost estimate was found for this element.

Appraisal costs reflect the need to reinterpret the existing seismic over the area at £2 million, plus the possibility of needing 100 km2 of new 3D seismic for exploration and appraisal at £5 million. Further appraisal requirements will likely increase the appraisal budget to at least £10 million. From the Lybster cost breakdown, we can add on the cost of temporary storage, £1 million, compression, £30 million, maintenance for the well, £3 million, and monitoring of the site, £20 million. It follows that the total cost for Fraserburgh and Solway Firth would be, to a very rough approximation, around £140/tonne, i.e. double the estimate for Lybster.

Forth Basin

No cost analysis is undertaken for the Forth Basin, as our recommendation is for this prospect to proceed as an experimental pilot study with a nominal injection rate of 10 ktpa. The site would require an injection well with the wellhead located onshore to reduce costs. However, the research budget would need to cover the cost of the well, and handling of the onshore dissolution of CO2 into brine extracted from the well. Any research proposal is likely to be costed at more than £10 million for the well alone. The brine extraction, mixing facility, and re-injection are likely to more than double the well cost. However, no data was found on the latter elements. As such, an accurate costing is beyond the scope of this study.

CDR market

The European Union and UK have yet to regulate a CO2 removal requirement. However, the voluntary market for carbon dioxide removal (CDR) is rapidly emerging, with rumours of Microsoft, Shopify, and Stripe buying credits valued at USD1,000 per tonne from Iceland’s Carbfix and Climeworks projects in 2021. Climeworks is offering public CDR subscriptions at USD1,500 per tonne (WP, 2024). These are based on direct air capture (DAC) and CO2 mineralisation in the young and reactive basalts of Hellisheiði, 20 km to the east of Reykjavik.

A different price signal for permanent storage has recently emerged in Europe. In 2023, the European Commission approved the Danish NECCS fund (DKK 2.6 billion, €350 million) for the permanent geological storage of CO2 from direct air capture and biogenic sources; the projects must be operational by 2026. In April 2024, Denmark awarded NECCS funding to three bio-CO2 companies to remove 1.1 Mt of CO2 between 2026 and 2032 – Table 8[2].

Table 8. Awarded NECCS funding for CDR and CCS in Denmark, April 2024.

|

Company, Country |

NECCS |

Storage |

Contract |

DKK / tonne |

GBP/tonne |

|---|---|---|---|---|---|

|

BioCirc biogas, DK |

2026-2032 |

Stenlille |

130.7 ktpa |

968.5 |

£110 |

|

Bioman biogas, DK |

2026-2032 |

Stenlille |

25 ktpa |

1,117.5 |

£127 |

|

Carbon Capture Scotland, UK |

2026-2032 |

Stenlille |

4.65 ktpa |

2,600 |

£297 |

These credits have been negotiated on the voluntary carbon market, and tentatively establish a low CDR value of £110. Ørsted, the Danish power company, are also contracted by Microsoft to capture 3.67 Mt of bio-CO2 over 10 years which will be exported to Northern Lights for a combined transport and storage cost of around €100 per tonne. The Ørsted credit value is unknown. However, given the much higher value of credits for geological storage in Iceland, we favour the high value of £297 as indicative of European CDR pricing in the near future.

Value proposition

Applying the high-cost prices for capture, transport, and storage, and assuming storage at Lybster, we can estimate a full chain cost. Low-cost bio-CO2 is sourced from the Inverness cluster. A combined capture and storage rate of 100 ktpa is assumed for a period of 10 years.

£60 per tonne for bio-CO2 from separation sources, primarily distilleries

£24 per tonne for transport for an average road distance of 188 km

£70 per tonne for storage from buffering tanks to decommissioning

- Full chain CCS cost estimate: £154 per tonne

- Voluntary market CDR credit revenue: £297 per tonne

- Net return on investment over 10 years: £143 million

Conclusions

The following section poses six questions that draw out the major themes and outcomes of our research. The answers are intended to highlight actionable policy directions that may support the rapid development of domestic CCS on small but lucrative bio-CO2 sources.

Can Scotland develop inshore bio-CO2 storage by 2030?

The short answer is yes. The key metrics are 3.7 Mtpa of available bio-CO2, including 109 ktpa of the lowest cost sources, mainly distilleries, within 188 km of the inshore Lybster prospect. This is a good source-sink match for a site that has an expected 2.1 Mt capacity. First injection by 2030 will require a rapid formal appraisal and regulated consents to permit storage.

The remaining prospects identified in this study are much less mature and characterised by locations that require a substantial investment to appraise. A realistic timeline for these prospects is 2035-2040 with no clear indication at this stage that the prospects are suitable.

How can this be funded?

There are several ways to fund the appraisal of Lybster, which we estimate will cost about £3 million and take three years. Commercial interest may be sufficient to raise capital. This may be through a capture company that is seeking storage, or as a joint venture between the capture company, whisky distilleries and their parent companies. A successful appraisal will lead to construction and commissioning, including site works such as tank installation and well engineering, which we estimate to cost £3-5 million. An approximate budget of £10 million is needed.

We note the strong narrative structure of decarbonising international brands within a cultural tradition. This may attract global corporations who wish to associate themselves with carbon dioxide removals that have a story to tell. As a strategic project for Scotland, the appraisal costs may be partly underwritten by government funding.

On commissioning, verified carbon storage certificates can be issued on the voluntary market at an estimated price of £300 per tonne. On injection, assuming a sustained injection rate of 100 ktpa and a 20% mark-down of storage to removal, the site would generate an annual revenue of £24 million. No subsidy would be needed once storage has commenced. This would contribute to both Scotland’s economic growth and a just transition to net zero.

How quickly can this be done?

The fastest appraisal-to-permit timelines in Europe are about three years. These fast-track appraisals rely on an aggressive pursuit of a commercial opportunity and a background of available data and mature understanding of the technical risk. Lybster has both the interest and the technical maturity. The missing piece is the necessary legislation to support a legal consent for the appraisal license and storage permit if successful. The legal advice is that the necessary consents may only require a transfer of existing UK regulations to Scottish law.

How much bio-CO2 capture is available?

In total, we have identified 3.7 Mtpa of available bio-CO2. This is far in excess of the initial requirement for inshore storage, which we estimate at 0.1 Mtpa. The 3.6 Mt surplus and its geographic concentration in the central belt suggests that offtake to Acorn via the Feeder 10 pipeline ought to be considered as a parallel strategy to inshore storage, noting that this could be a considerable time in the future – Figures 13 and 14.

Combustion source capture is relatively high cost at around £120 per tonne. Separation is much more valuable at £60 per tonne. Distilleries and AD upgraders are common at the low end of the range, making up nearly half of the smallest 27 sites that average 5 ktpa, and one-third of 22 sites that average 10 ktpa. Significantly, there are 14 separation sources near Inverness that may support 21 modular capture units assuming 3-5 ktpa per unit, i.e. sufficient to batch load 16 trucks at 20 tonnes per day for a 100 ktpa supply to Lybster.

Figure 13. Central Belt sources: 2.3 Mt of combustion bio-CO2 is available, of which 0.3 Mt is from 28 small AD sites; another 190 ktpa of separation bio-CO2 from 6 distilleries and 2 AD biogas upgraders.

How much storage capacity is available?

Based on current data, our analysis found that only the Lybster prospect has potential commercially viable storage capacity – expected to be 2.1 Mt. This would be sufficient for 20 years of storage at an injection rate of 100 ktpa. This is not significant in terms of overall storage capacity in the North Sea or in terms of Scotland’s overall statutory climate targets but would provide an opportunity to showcase Scotland as a global frontrunner for CCUS technologies.

2.1 Mt of storage would generate £500 million in CDR revenue at 100 ktpa – an injection rate that is much lower than the technical limit for CO2 storage, which is generally thought to be around 700 ktpa. The low estimate is 0.35 Mt, which would result in only three to four years storage and a revenue of £72 million. The high estimate of 9.4 Mt would be more than sufficient to provide storage out to 2090 at a revenue in excess of £1.5 billion.

What policy actions need to be taken?

The legal opinion is that minor amendments to existing regulations are required to license storage appraisals and storage permits in the territorial waters of Scotland. To repeat the summary from Chapter 1: CO2 storage involves multiple activities under different licensing regimes. It may well be, however, that insofar as existing regulations could be relied upon, the process of modifying existing statutory instruments could be fast. This would really be a question for those with a better insight into the technical detail and political due process.